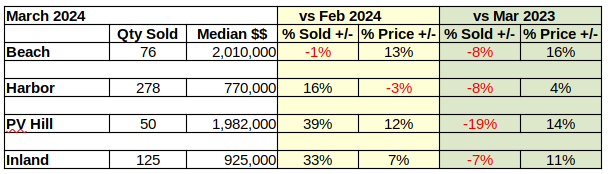

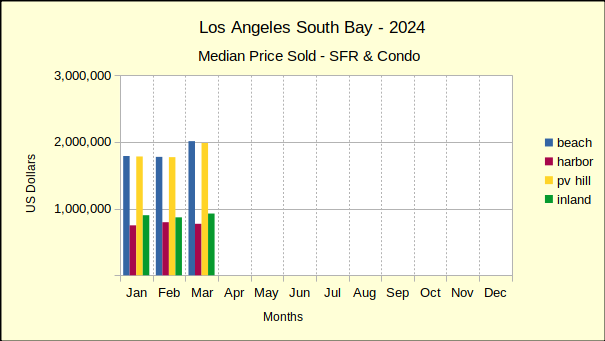

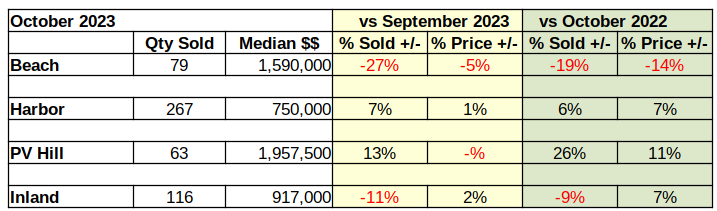

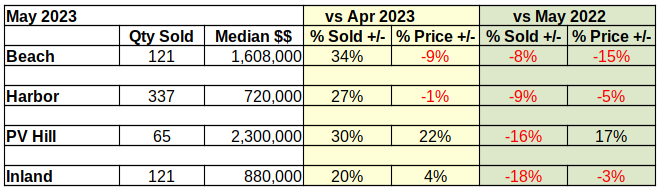

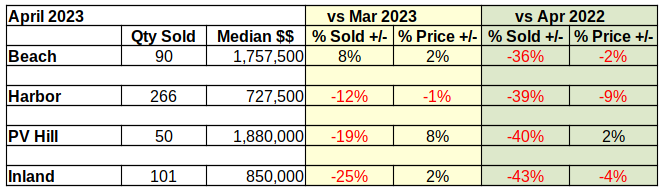

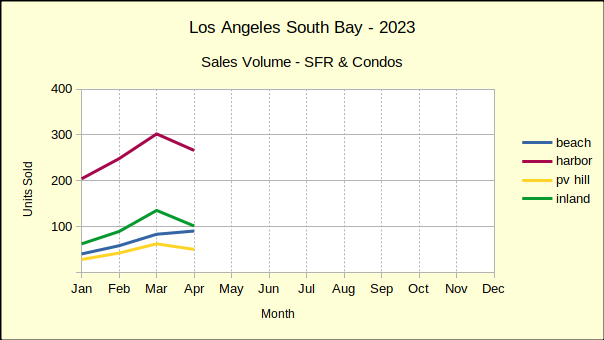

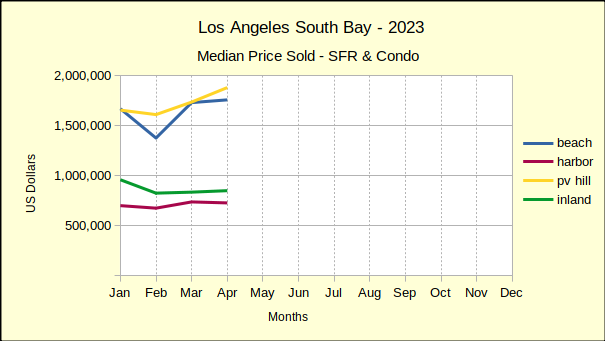

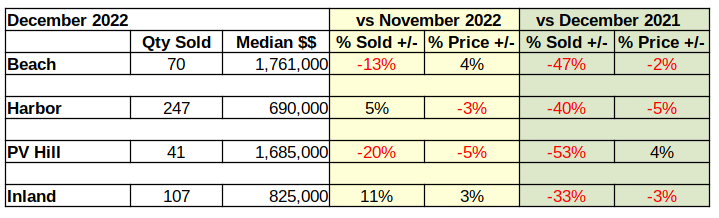

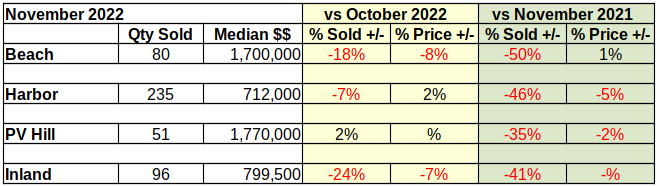

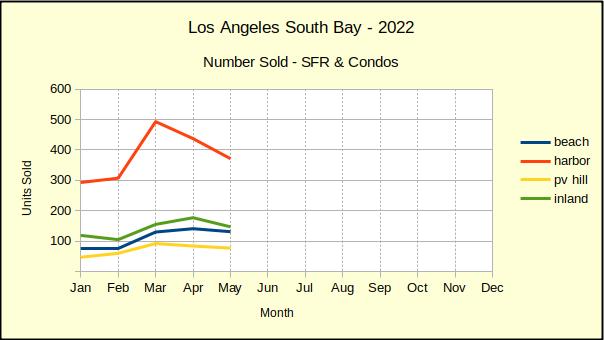

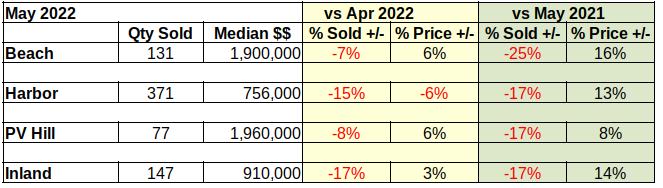

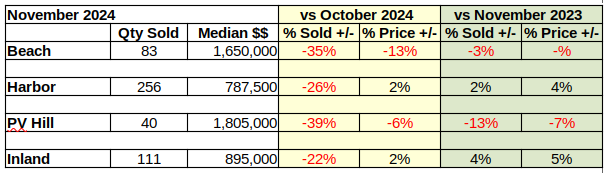

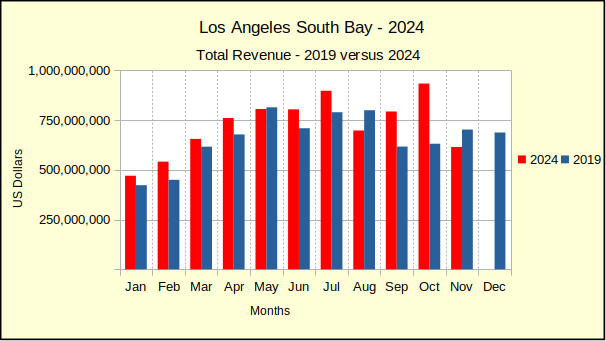

On the heels of an encouraging October real estate market, November saw the South Bay market plummet into the red. Compared to last month the number of homes sold fell by nearly 30%, while the median price collapsed at the Beach and on the Hill. At the same time, the Inland and Harbor areas showed modest growth in median price, posting a 2% gain in both areas.

This was a surprising downturn following across the board sales growth in the October market, accompanied by generally positive price appreciation.

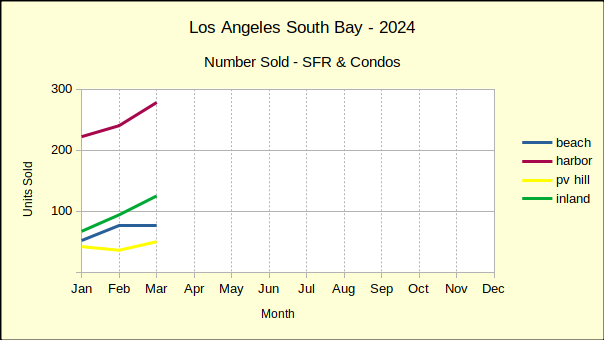

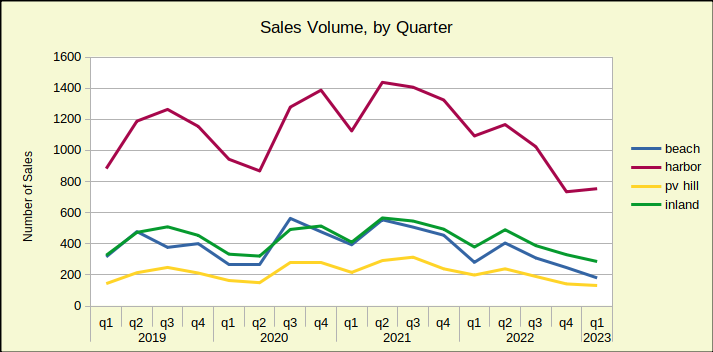

Looking at year over year, same month sales provides a slightly more positive result. Both the Beach and the Hill show the number of homes sold down by 3% and 13% respectively. The Harbor area maintained sales growth of 2% while the Inland area increased by 4%. Both areas were off substantially from the 20-30% increases of October.

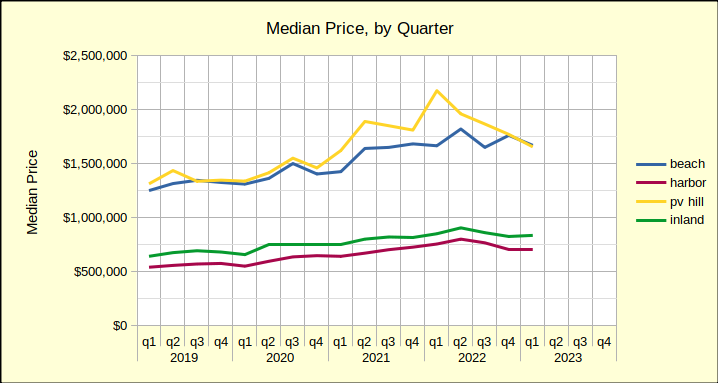

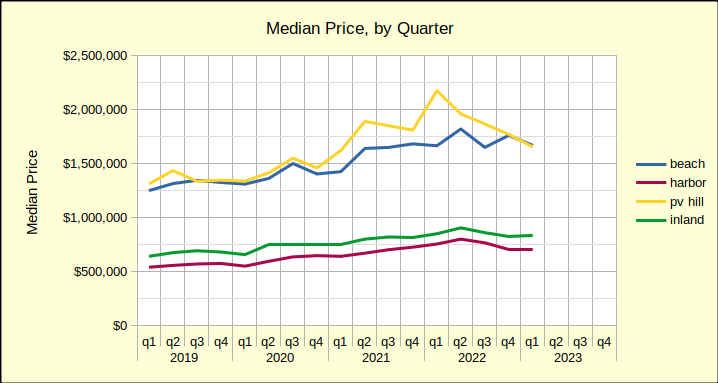

Year over year median prices were equally depressed. The Beach and the Hill, the high end of the South Bay market, both lost ground in the single digits. The Harbor and Inland areas, which make up the bulk of sales in the South Bay, grew at 4% and 5% respectively.

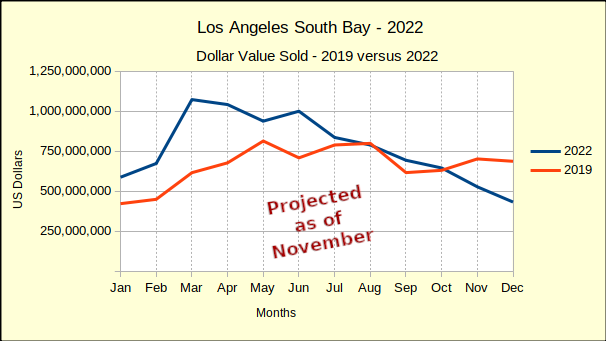

It’s too early to attribute this shift to the election results because most of the transactions closing escrow in November would have been negotiated in October. If anything, the decline reflects nervous anticipation leading up to the election. December sales will provide a much more definitive indication of how the public has reacted to the election results.

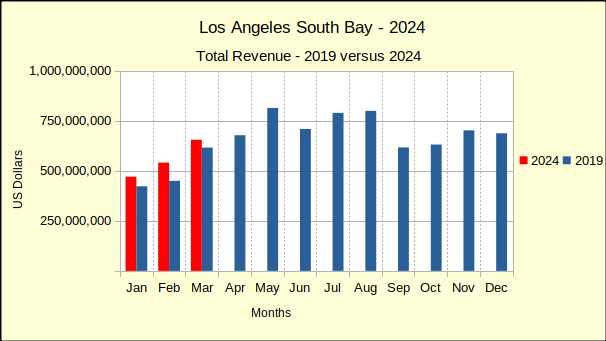

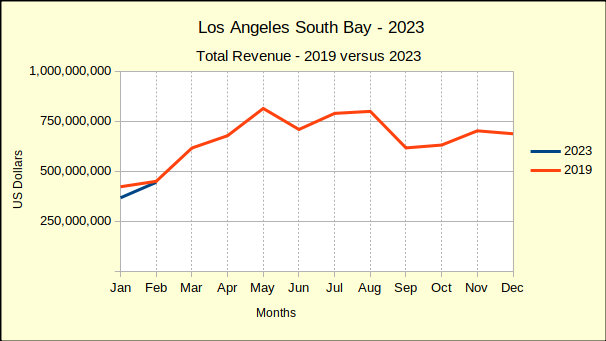

For right now we know that current sales volumes are running about 10% below December of 2023. And, we know that December last year was lower than December 2019 by 30%. Back at the end of October conditions seemed to be improving, but today it would seem we are still trying to climb out of the Covid trough.

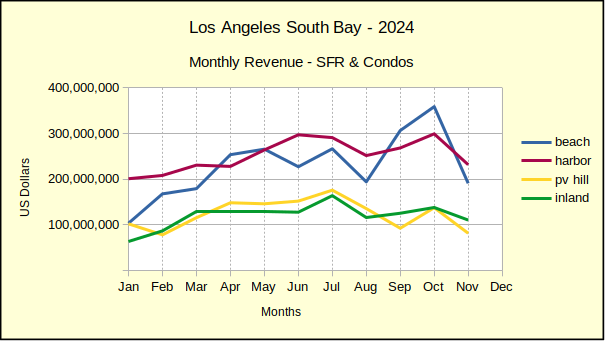

Beach: Sales Off 35% for November

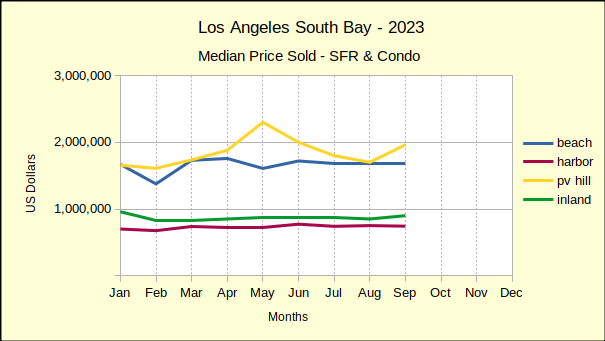

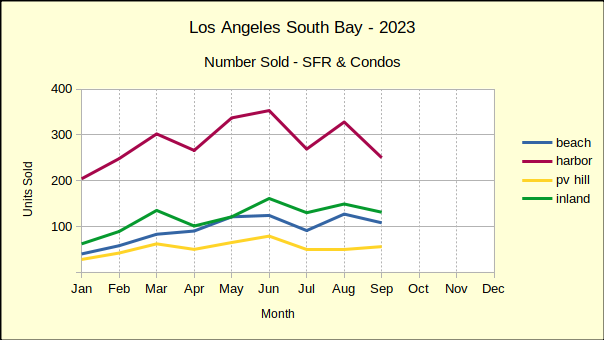

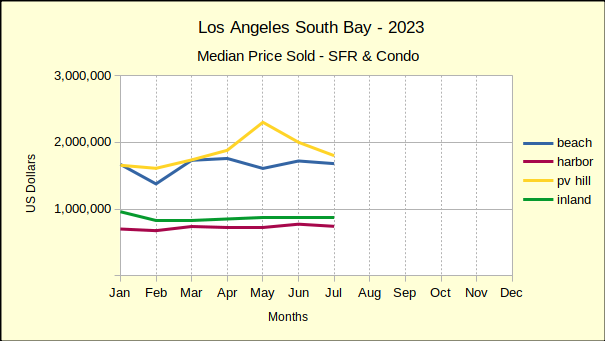

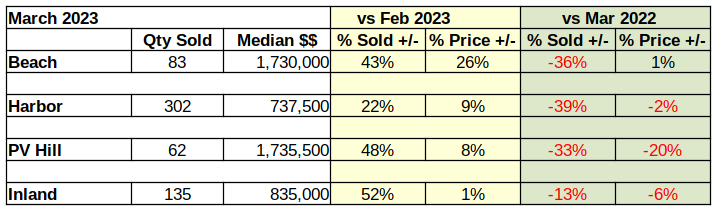

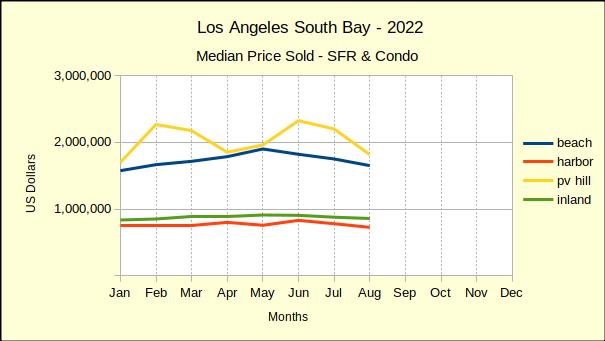

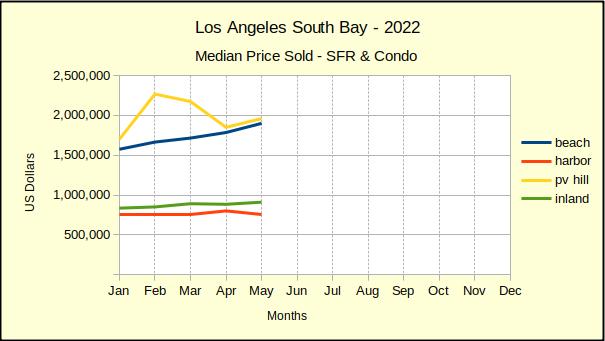

The number of homes sold in the Beach Cities dropped from 127 in October to 83 in November showing a 35% decline for the month. At the same time the median sales price dropped from $1.9M in October to $1.65M in November for a loss of 13%.

On an annual basis sales volume was off by 3% compared to last November, while the median price was flat.

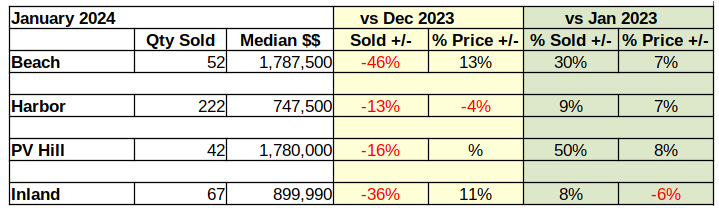

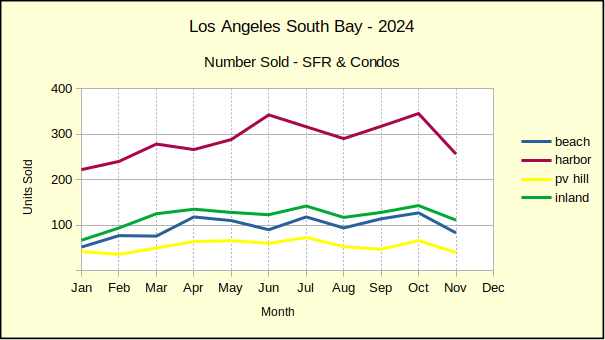

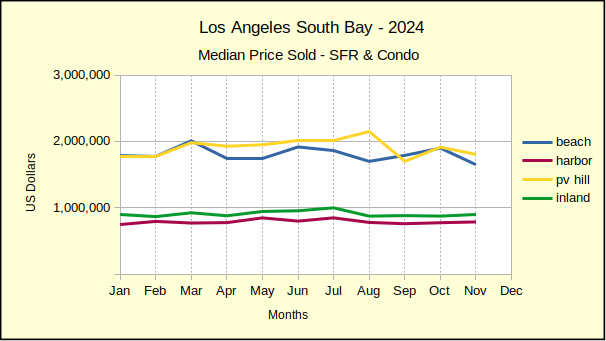

Year to date, 1,059 Beach homes have been sold compared to 1007 during the first 11 months of 2023. This is a 5% increase in the number of homes sold. The median price rose 7% from $1,675,000 last year to $1,787,500 year to date.

Harbor: Sales Fall 26% in November

Harbor area home sales plunged 26% from October, dropping to 256 units from 345 sold last month. At the same time the median price climbed 2%, to $787,500 from $775,000.

On the flip side, same month, last year sales moved the opposite direction, rising 2% this year compared to 252 homes sold in November of 2023. The median price this November was up 4% over the $760,500 recorded in November of last year.

With only one month remaining in the year, the Harbor area displays modest increases in both the number of homes sold so far this year and the median price of those homes. Annual sales have reached 3,160 to date, 3% higher than last year’s 3,076. Median prices for the year have climbed from $740,000 last year to $780,000 this year.

Hill: Market Drops 39% for the Month

Home sales on the Palos Verde Peninsula dove down 39% from October to November, wiping out all but 1% of last month’s gain. As mentioned in the October issue, during the last quarter of 2023 mortgage interest rates were hitting around 8%, which drove the South Bay market to a standstill. The fact 2024 sales volume is falling below 2023 is a concerning matter. Interest rates are once again pushing up against 8%, which has been an impenetrable barrier in recent years. While the number of homes sold dropped precipitously, the median price came in with only a 6% decline, falling from $1,914,500,in October to $1,805,000 in November.

Comparing November of 2023 to November this year turned up a steep fall again. This year brought a sales volume decrease of 13% accompanied by another 7% drop in the median price.

As 2024 heads for closure, the dramatic swings of earlier in the year are mellowing out. Through November, the 597 sales on the Hill have settled in at just 1% above last year. Similarly, the median price, which has ranged from an increase of 26% to a decrease of 15% throughout the year, is coming in at 3%, or $1,927,500.

Inland: Home Sales Collapse by 22%

November sales of 111 homes in the Inland area totaled a 22% drop from the 143 sold in October, rounding out a total decline of 28% for South Bay real estate this month versus last month. Despite the fall in month to month sales volume, the Inland area enjoyed a 2% increase in median price over October.

Same month last year sales increased by 4%, moving up from 107 units in 2023. At $895,000, the median price for November Inland area homes was up by 5% over the $851,000 of last year.

Looking at year to date sales volume of 1,313 shows a mere 1% increase over January-November of 2023 when 1,302 homes sold. Median price fared higher, with a 3% jump from $867,500 to $895,000 this year.

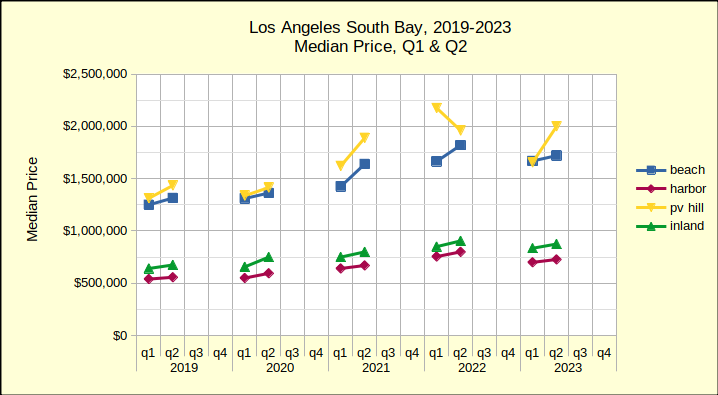

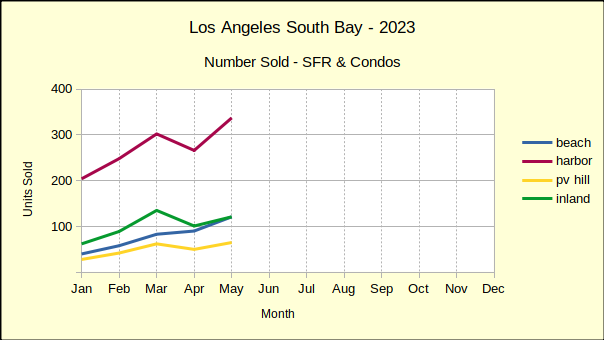

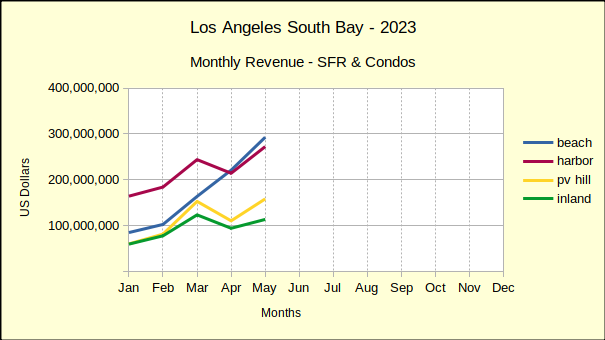

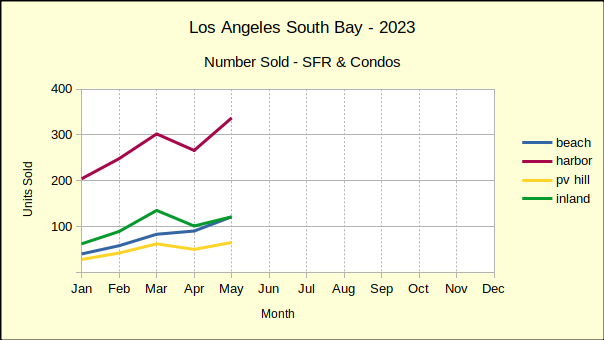

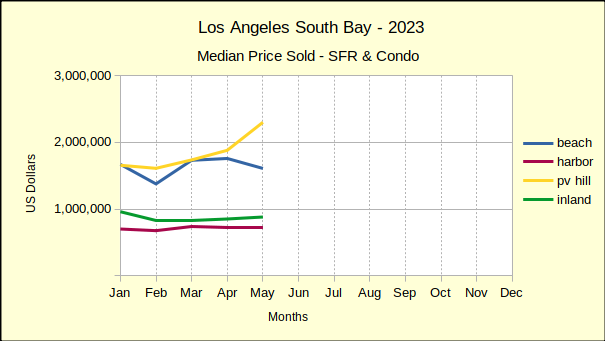

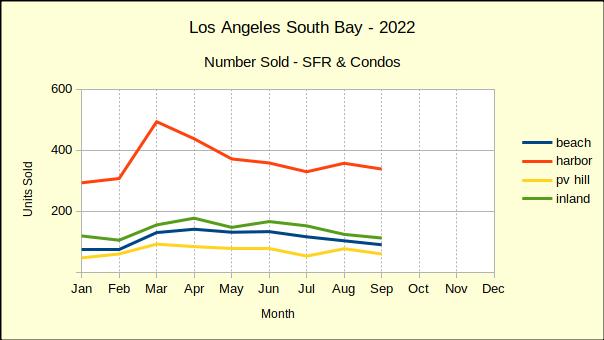

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

Inland=Torrance, Lomita, Gardena

Photo by CURTIS HYSTAD on Unsplash