When prices are changing rapidly — whether they’re going up or down — there’s always a risk of appraisers not being able to catch up. Most of the data available to appraisers is at least a week old, usually a few weeks. Most of the time, this is good enough, but not when price fluctuations are happening quicker than that. It’s expected that prices will be dropping rapidly throughout 2023 and 2024, which increases the risk of overappraisal. This is especially harmful to buyers who may end up paying more than the home’s actual value, immediately falling into negative equity. Lenders also want to avoid this, since they can incur losses when lending to a buyer who is suddenly in debt.

It’s not an issue that can be eliminated entirely, but luckily, there’s a way to at least mitigate it. In 2007, Fannie Mae encouraged appraisers to start including an assessment of the current market direction. Since 2009, oversight for appraisals is not handled by Fannie Mae but rather by appraisal management companies, but its still good advice. It means that even if the appraisal is off by a bit, involved parties will know in what direction the error is likely to be and can plan accordingly. Fannie Mae suggests that the assessment be limited to the neighborhood of the property in question and include data on recent price changes, average days-on-market, and inventory.

Home sales volume tends to follow a similar seasonal pattern each year. It most often peaks in the middle of the year, falls off rapidly once winter arrives, and is at its lowest point the following January before restarting the cycle. The pandemic didn’t completely upset the pattern, but there were some noticeable shifts.

2020 could actually be described as having two cycles — one in the first quarter and one during the rest of the year. The first cycle peaked just before lockdowns in March, while the seasonal variance was on its upswing, before crashing down to the lowest point of the year in May. The peak of the second cycle was towards the end of the year. Home sales predictably shot up as the year entered June, but then continued their slight upward progression. The second cycle did reach bottom in January, as expected, but the low was significantly higher than prior years, as pent-up demand was still high.

The first half of 2021 seemed fairly normal. Home sales volume increased fairly steadily until the summer months. The peak was higher than normal, likely for the same reason the year started at a higher point. But the decline in the latter half of the year was quite a bit sharper than usual. The trough in January was lower than that in the beginning of the year, despite coming down from a higher point.

The shape of 2022 was rather odd. Like 2020, the peak was actually in March. But this time, it wasn’t because of a pandemic. It was the realization that we’re at the start of a downward cycle in the housing market overall. There was no steep increase just before June; it just continued to decline, though there was a minor upward bump later in the summer. The data is not yet available for December or January, but considering November’s home sales volume was already lower than the trough in January 2019 — the most recent trough of a normal cycle as well as the lowest value during a normal cycle in the past decade — and sales are continuing to decline, one can expect the numbers will be quite low.

A build-to-rent community is a community in which single-family homes are build solely for the purpose of renting them out. It isn’t a new concept, but it’s been under the radar for quite some time, comprising only 3% of the single-family residence (SFR) market. As just one of many changes in the type of demand brought in the wake of the pandemic, that number is now up to 12%.

Many people who transitioned to work-from-home needed more space for a home office. That meant looking for a larger home. For renters, that often wasn’t possible, since they were priced out of the homebuying market. But what if they could rent the type of home people normally would buy? In a build-to-rent community, they can. The SFRs in such communities have significantly more space than apartment units, and while they are certainly more expensive to rent than apartment units, rising home prices meant renters definitely couldn’t buy if they weren’t able to before. It’s definitely possible to find SFRs that are not in a build-to-rent community, but looking for such a community guarantees it, and also comes with community amenities.

Home prices have begun their decline after a period of incredibly high prices. More regions of California are following suit. In October, 22 of the 51 tracked counties (California has 58 counties) recorded a decline in median sale price from the prior year. In November, this increased to 33 counties. Only two broad regions of California experienced price growth from the prior year, the Central Coast, with an increase of a mere 0.1%, and the Inland Empire, with a 2.1% increase. In all regions, prices are down from October to November. Prices are declining for both single-family residences and condos.

The largest changes from November 2021 to November 2022 occurred in Napa County, an increase of 29.4%, and Mariposa county, a decrease of 27.2%. The biggest positive and negative changes between October and November 2022 occurred in Tehama County, an increase of 10.8%, and Santa Barbara County, a decrease of 28.3%. Home prices are not the only thing declining. Home sales volume has also dropped precipitously since November 2021, decreasing in every single county except Mendocino County, which saw an increase of 4.5%. Mendocino is also one of the counties in which prices are still increasing. In most counties, the decrease in sales volume hovered around 40-50%, though some were higher or lower. The decrease reached as much as 68.9% in San Benito County, but was only 12.5% in Glenn County.

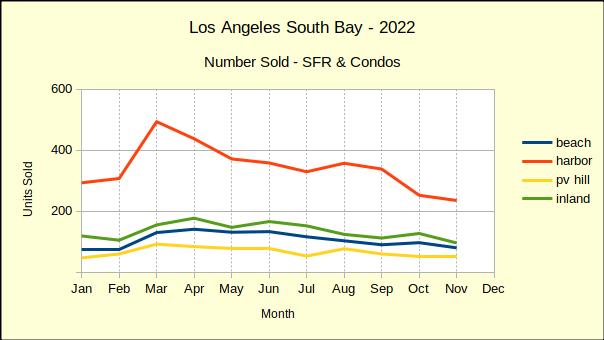

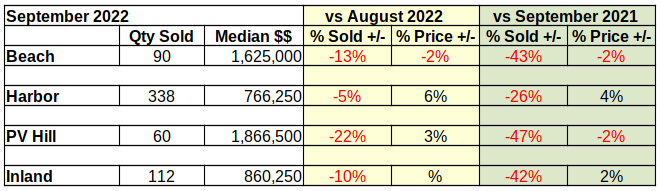

November saw the number of homes sold in the South Bay fall 12% from October totals. Sales volume has declined in seven of the eleven months on a month to month basis since the beginning of the year. Sales tipped up a modest 2% on Palos Verdes peninsula, while volume dropped 7% at the Harbor, 18% at the Beach and 24% in the Inland area.

Year over year sales look even more depressed with a 45% drop from 2021 sales across the South Bay. The Beach Cities led the plunge with a 50% fall, followed by the Harbor area at 46%. Palos Verdes and the Inland area brought up the rear with 35% and 41% respectively. The falloff in sales began with a 17% drop in January and has been increasingly negative since.

Because 2020 and 2021 were both significantly impacted by the coronavirus pandemic and the governmental response to it, 2019 is the most recent year with a normal business pattern. Comparing 2022 sales volume with 2019 provides the truest measure of the current recession. Overall, for the first 11 months of the year, the South Bay has experienced a 9% decline in sales compared to 2019.

Through the month of November, sales on the PV Hill have fared the best, showing a modest drop of 3% compared to the same time period in 2019. The Harbor and Inland areas which generally are entry level for the South Bay both fell back 8% for the same period. So far this year the Beach Area has suffered the largest declines with an 18% drop in number of sales versus 2019.

Annual Sales Dollars Off By $3.2 Billion

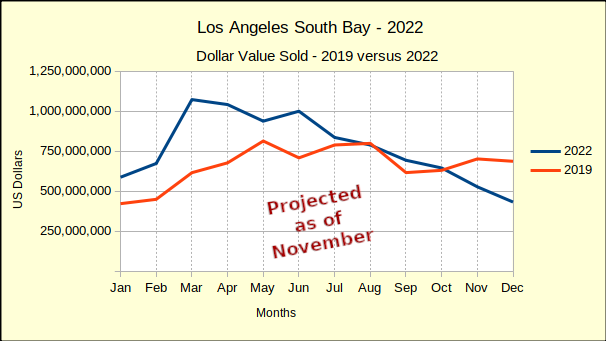

Comparing year-to-date sales of homes in the Los Angeles South Bay shows a drop in dollar value from 2021 to 2022 of over $3.2 billion. That represents an over-all decline of 22% in total dollars sold from the same 11-month period last year.

The Beach area has been the hardest hit so far with a drop of 34%. The PV Hill has dropped 29%, while the Harbor area has fallen 22%. The Inland area fared the best, only down 19% for the same 11 months.

On a month to month basis, the decline in sales accelerated from 7% in October to 18% in November. The Inland area which had flipped to a positive gain in October plummeted by 30% in November. Similarly the Beach which had been up 7% in October fell 25% in November. The Harbor and Hill areas were off by 8% and 11% respectively.

At this point year to date South Bay sales dollars for 2022 still exceed the total for 2019 by 22%. We expect the end of year numbers to be positive. However, with monthly sales figures shrinking by 30%-40%, we project 2023 to fall below 2019.

Median Price Shows Mixed Results

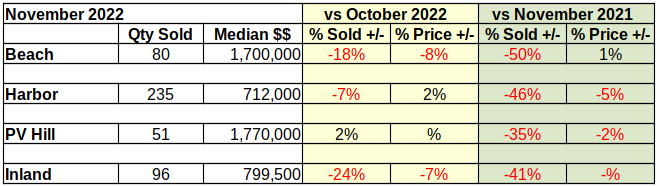

Statistically speaking, the Beach cities median price fell 8% from October to November. The reality is that the median in October was unusually high. Multiple sales of Strand property drove the median up 14% that month. The blue line on the chart below shows the one month blip and median prices dropping back to a steeper downward pace in November.

Palos Verdes was flat compared to the previous month. This is a rare event as one can see by the erratic yellow line on the chart. Because the physical area is smaller than the other geographical areas, the number of sales is smaller, and mathematically the sample size is smaller. Thus one or two outlier sales can create wide swings in the chart.

Similar to the Beach area, the median price dropped 7% in the Inland area. This decline follows two months of no change, preceded by three months of month over month negative median prices.

At the same time the Harbor area experienced a month to month increase of 2% in the median price. Researching this anomaly we discovered 11 new construction sales in Carson had been accumulated and posted simultaneously by the developer. It’s worth noting that Harbor area median prices have also been elevated to some extent by the new construction on Western Avenue in San Pedro.

From a year over year perspective, November median prices continued to fall in comparison to those of November 2021. The Harbor and PV Hill areas were down 5% and 2%, respectively. Median price in the Inland area dropped from positive 6% in October to negative .05% in November. The Beach cities remained positive with growth of 1% in November. That being in contrast to an unexpected growth of 20% last month caused by the sale of multiple Strand properties in Manhattan Beach.

Despite increasingly deep reductions in sales volume and in median price throughout this year, the median is still higher than it was in 2019. Palos Verdes home owners have fared the best with the current median price 40% above the November 2019 median. The Harbor area is still 34% higher and the Beach cities still maintain a 31% advantage. The Inland area has proven to be relatively stable throughout the pandemic and currently the median price is 27% above that of 2019 for the same 11 month period.

Year End Projection Updated

We’ve been comparing 2022 to 2019 all year because real estate sales during the height of the pandemic were so out of the ordinary, regular year over year comparisons yielded untenable results. The chart below depicts the current year total sales for the South Bay compared to sales from 2019.

Tracking the blue line, one can see where sales dropped below 2019 values in August, recovered in September, then slipped below again in October and November. Assuming the decline continues at the same rate, we are forecasting the December sales to drop another $75 million, or so.

The end of the year would then reflect accumulated sales of approximately $9.4 billion. That would mean 2022 total dollar sales come in at $1.4 billion above the $8 billion total dollar value sold in 2019. Across the South Bay that would be approximately an 18% increase.

Broken out by community, we forecast total dollars sold in the Beach cities to be 6% above 2019, followed by the Inland area with a 20% increase. Harbor comes in next with a 21% increase and the PV Hill with a 35% increase.

At a Glance

As 2022 draws to a close we find the final numbers for both sales volume and median price show the year to be rapidly declining from the final figures for 2021. However, the totals all remain positive. We expect December to continue the trend downward, though the year should end on a positive note.

With the number of units sold decreasing every month by 35% to 50%, and the median price now falling, 2023 should be firmly in the grip of the recession by mid-year.

Disclosures:

The areas are: Beach: comprises the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: comprises the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: comprises the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: comprises the cities of Torrance, Gardena and Lomita.

Although it was undeclared, we’ve been in a recession, which is usually indicated by two consecutive quarters of gross domestic product (GDP) loss. GDP has been going down, but now suddenly GDP is going back up. So does that mean we are out of the recession? Well, if it had ever been declared, it would be declared over — but that doesn’t mean it actually is, especially since it was never declared to begin with.

GDP is ultimately based on consumer spending. When consumers spend more, GDP goes up. This is indeed what happened. However, that isn’t necessarily a good thing. You may have read one of my posts from a few days ago about plummeting savings rates. As stated in that post, savings rates have recently dropped dramatically, which is normally an indicator of consumer confidence, but in this situation is actually a result of necessity due to increasing costs of living. In other words, inflation occurs, consumers must spend more to buy the products they need, therefore GDP goes up. We tend to think of GDP increases as good, but the reality is that it’s simply a mathematical value that can shift as a result of a variety of different factors, both positive and negative.

Some of the most significant closing costs are related to loans. During a cash sale, loans aren’t a factor, so you may be thinking closing costs are no longer relevant. However, there are certainly closing costs unrelated to loans. And the rules for who pays don’t change; it’s still negotiated between the buyer and seller.

The costs related to loans include origination fees, processing fees, and credit checks. These are all generally paid by the buyer, but you don’t have to worry about these at all for a cash sale. That doesn’t mean everything else is automatically paid by the seller. Closing costs also include earnest money, property inspections, appraisals, title insurance, and a title search. It may also include attorney’s fees, notary expenses, and some escrow fees, if applicable. Earnest money is always paid by the buyer, and in most cases, all or nearly all closing costs are. However, there’s always room to negotiate. Particularly in the case of a cash buyer, the buyer may have more negotiating power because the seller is less likely to want to lose a cash buyer.

Before you get a mortgage loan, ask yourself whether you want a qualified mortgage (QM) or non-qualified mortgage (Non-QM). You may be wondering under what circumstances you’d want your mortgage to not be qualified. Well, there are advantages and disadvantages to both. Non-QMs don’t conform to the regulations set forth by the Consumer Financial Protection Bureau (CFPB), but they’re actually entirely legal — the government simply can’t guarantee consumer protections.

So what are these protections, and why might you want to risk going without them? A QM loan cannot last longer than 30 years, cannot have prepayment penalties, cannot be a balloon loan, and should not have negative amortization. It requires a process for verifying several sources of information, including but not limited to bank statements and income. Because of this, it’s often more difficult to qualify for a QM loan. Therefore, someone who can’t qualify for a QM, such as many gig workers, may risk a non-QM loan. Investors, especially foreign investors, also frequently opt for non-QM loans that only require payments on interest. It’s also possible that you want to go for a longer-term loan, which would come with smaller payments, albeit a higher total amount paid once the loan is fully paid off. In any case, you probably want to ask a professional to explain the terms and risks of any loan you are considering taking, whether qualified or not.

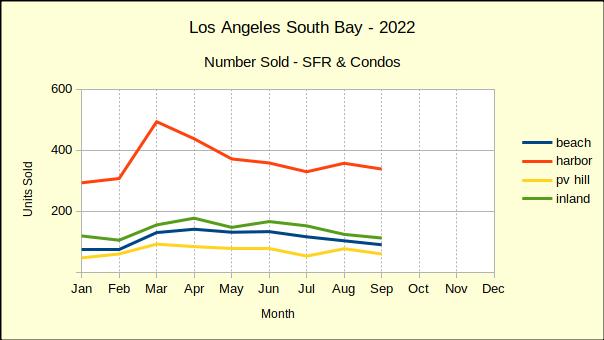

Last year saw home sales in the South Bay escalate dramatically as buyers sought to become homeowners while interest rates were still abnormally low. With interest rates rapidly rising it’s no surprise that sales are plummetting in 2022. The Harbor area, traditionally an entry level market, handily out-sold the balance of the South Bay with a drop of only 26%. The remaining areas suffered sales drops ranging from 42% to 47%, with the South Bay as a whole dropping 35%.

Compared to last year, cumulative South Bay home sales were down 21% as of September. The first three quarters of 2021 saw 7767 townhomes and single family residences sold, versus 6163 during the same period this year.

Recognizing that 2020 and 2021 were exceptionally aberrant, we also compared the 2022 year-to-date sales volume to 2019, the last normal year of business prior to the pandemic. As of the end of September 2022 cumulative sales volume was 4% lower than it was for the first nine months of 2019.

The decline from 2019 sales is uneven in that the biggest drop, 15%, is seen in the Beach area, which is typically at the high end of the market. Sales in the Harbor area only dropped back by 2%, while sales in the Inland area fell by 4%. The Palos Verdes peninsula fared best, actually increasing in quantity sold over 2019 by 4%. As always we offer a cautionary note when looking at statistics for property on the PV Hill. Because there are considerably fewer homes in that area, percentile statistics can take large swings.

Median Prices Mixed in September

The number of homes sold in 2022 has declined, indirectly affecting the median price of those homes, as well as the total dollar value of all the homes sold in the same period. A closer look at the median price of homes sold through September yields some surprising changes.

Since prices increased dramatically during the coronavirus pandemic we anticipated finding the median price from 2022 to be considerably higher than that of 2019. Indeed, that is the case with the median in the Beach area up 31% over that of 2019, the Harbor up 36%, PV Hill homes up a staggering 47% and the Inland area up 30%. But, that is gradually reversing.

July and August of this year showed depreciation in the median price across the South Bay. Prices consistently dropped in a range from 2% down (Inland) to 18% down on PV Hill. September sales broke the pattern with only the Beach cities losing value per the median. The Inland area was flat, showing no change from August. In an unexpected twist, both the Harbor area and the Hill came in with an increase in the median price. The growth was modest, up 6% for the Harbor area and up 3% for the Hill. Despite the slight improvement in September prices we anticipate continued downward pressure as inventory grows and time on market stretches.

Looking at the median price on a year-over-year basis, we find September with minor declines from August. The Palos Verdes cities showed prices dropping by 2% last month and this month. At the same time the Beach cities dropped 2%, while the Harbor and Inland areas increased by 4% and 2% respectively.

Median prices started 2022 with increases regularly coming in well above 10% growth. In April we saw the first negative where the median for the Hill fell 2% from 2021. Since then we have watched the rate of price appreciation decline from double digits until now in September with both the Beach and PV areas losing value.

We fully expect all areas of the South Bay to reflect declining median prices before the end of the year. While prices will be down on both a month-to-month and year-to-year basis, we don’t anticipate the median to fall below 2019 price points this year.

Total South Bay Sales Dollars

When the number of sales is decreasing and the median price of those sales is also decreasing, one has to assume the gross revenue will also decrease. Governor Newsome has been warning for several weeks that the 2022-23 fiscal year will not see the State level revenue surpluses California has been enjoying.

During the first quarter of 2022 gross revenue from real estate sales remained predominately positive, with year-over-year growth rates of about 6% per month. Since March the South Bay has only seen two instances of sales growth, 7% in the Harbor area for April and 3% in the Inland area for June. Every other entry on the chart is negative, with September declines averaging about 40%.

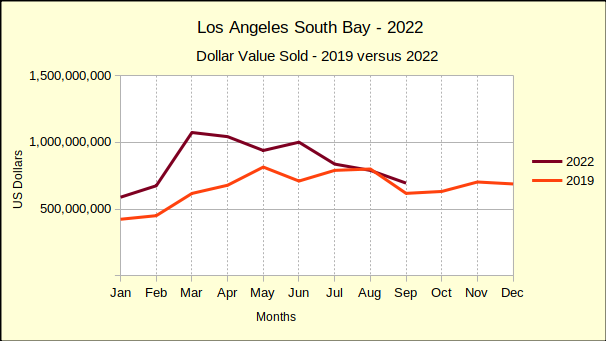

Cumulative sales for the first three quarters of 2022 were off by 29% compared to 2021. Our monthly sales dollars chart shows a zig-zag downward trend since spring of this year. Of course, 2019 is a more realistic point of comparison as a result of market gyrations created by the pandemic and our government’s fiscal response.

Comparing 2022 sales totals to 2019 yields a clearer picture of the current direction of the market. Instead of a sea of red ink, we can clearly see that 2022 sales have remained above those of 2019 with the exception of August. Sales started normally, then in March the Federal Reserve Bank announced a .25% interest rate hike, and promised more to come.

Buyers threatened with increasing monthly payments jumped into the fray and pumped sales up for a couple months. Then a new .5% increase, accompanied with the promise of multiple .75% increases throughout the year began a downward slide in home sales that is continuing.

Following the trajectory of the maroon line, and assuming the interest rates continue to increase, we predict 2022 sales will drop below 2019 again in October. The Federal Reserve Bank has already announced plans for another .75% increase in November, followed by a .5% increase in December. Adding another 1.25% will bring the full increase for the year to 4%. We envision the fall in sales growing steeper, bringing total sales below that of 2019 for the final quarter of the year.

Statistical Summary

This would be the heart of the discussion if we were dealing with a normal fiscal environment. Here we could talk about month-to-month changes and changes from the same month last year to this year. Instead we’re faced with an unanticipated side effect of the pandemic—out-of-control inflation followed by a steep recession.

The areas are: Beach: comprises the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: comprises the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: comprises the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: comprises the cities of Torrance, Gardena and Lomita.

Goodbye Marymount, Hello UCLA!

Marymount California University, is no more. But, shed no tears! The prestigious University of California at Los Angeles plans to open the site for classes in the fall of 2023-24. Escrow had not yet closed as of this writing, but all appears to be moving forward at good speed.

We are told the finalists included four developers and three educational institutions. We’re pleased that UCLA was the successful bidder. We’ve heard some of their ideas and look forward to having them as neighbors.

However, we’re also interested in what kind of potential the developers saw in this deal. There’s a total of 11 acres already developed as residential and 24.5 acres developed as a campus. What would that have looked like if a residential developer purchased the site?

The 24.5 acres, some of it with gorgeous ocean views, is the jewel in the transaction. A little “back of the envelope” calculation says that using an average of 15,000 square feet per lot, Which is about the average in that neighborhood, one could build about 70 high end homes at the location. New construction on similar sites is selling for about $7.5M today, giving a value for the finished project of approximately $525M. Not bad for a land purchase of $80M, especially considering we haven’t started looking at the 11 acres.

There exist some legal complications in the 86 unit, 11 acre property. Deed restrictions purported to require the land to be used to house students. That can readily be accommodated by an educational institution, like UCLA. Developers on the other hand might have to pay some serious legal costs to do anything else with the land.

And it might have been worth the legal expense. A quick look at the apartment building market in the South Bay shows roughly comparable buildings selling for about $420K per unit. That would make 86 units worth about $36M, almost half the stated purchase price.

We’ll never know what might have been. The entire South Bay can look forward though, to an educational revival. A refreshed campus with UCLA’s academic resources and access to the university program at AltaSea and other port projects is a great starting ground.

Much of the danger to tenants is being unable to pay rent, as both rental prices and cost of living continue to increase while the job market is still in recovery. However, that isn’t the only way tenants can get evicted. There are even a few ways landlords can legally evict tenants that haven’t done anything wrong. That isn’t enough for some landlords though, who are actually resorting to illegal methods of eviction instead of notifying the tenant and potentially going through the court process.

Though both are legal, the court process distinguishes at-fault and no-fault evictions. At-fault evictions are the category where failure to pay rent lies, and this category also includes various contract violations and criminal activity while on the premises. The no-fault category includes landlord’s intent to occupy the property, withdrawal from the rental market, property being deemed unfit for habitation, or landlord’s intent to demolish or substantially renovate the property. Some of these can be used misleadingly as the landlord can simply change their mind later, but the real problem is unlawful evictions. The Office of the Attorney General (OAG) is particularly concerned with the type known as self-help evictions. This includes the landlord shutting off utilities, changing locks, or removing the tenant’s personal belongings in order to force them out of the property. Landlords initiating a self-help eviction can get charged with a misdemeanor, and the sentence is either a fine or a jail term of a maximum of one year.

Home prices fluctuate constantly, but have certainly been on an upward trend the past few years. In fact, it may not be quite as noticeable, but they’ve been trending upwards for about a decade. The difference is that the upward trend has occurred at an anomalous rate since 2019. But now, we’re starting to see hints that this isn’t going to continue. Currently, home prices are still high; however, sales volume has been dropping for the past four months, which will naturally lead to price drops.

On its own, rising home prices isn’t the problem; the issue is that they have been rising far quicker than wages. Even a period of flat home prices at their current high level would provide some slight respite to homebuyers, though of course they would benefit more from declining prices. Sellers aren’t going to be as happy in the next few years, especially if they bought recently. If they bought before 2019, they may still be able to sell at a profit, but not as much of one as if they had already sold by now. Without knowing how much prices are going to drop, there’s a risk of negative equity for homes purchased within the past three years, with the risk increasing the more recently it was purchased. If the downward cycle is particularly long or the decrease particularly steep, this could even extend to homes purchased much earlier.

Renting out your home, especially for a short period, can seem like a simple way to turn a profit without much effort. However, there’s a fair bit that goes into getting the home ready to be rented out. Just like if you were selling your house, you need to make sure there’s interest, which means making a good impression on potential renters.

The easiest way to do this is by repainting your home, which is something you’d probably do if you were selling as well. It may even be more important when renting, though, especially if you aren’t going to allow your tenants to repaint. Buyers may think they’re just going to repaint anyway, so they don’t care what color the walls are. But with tenants, you want to be sure to choose neutral colors that won’t offend anyone’s aesthetic.

You should also be sure that all the legal details are worked out. You may feel the desire to skip the middleman, but that’s not a good plan. A real estate agent will help draft a lease that protects both you and the tenant. Property management companies remove much of the headache of being away from the property. Regular maintenance can often be left to property management companies. That said, if the house is not in good condition from the outset, tenants won’t be interested enough to sign a lease. Make sure to take care of repairs before you start.

The aftershocks of the Great Recession are already here. We’re currently in the midst of a second, undeclared recession, albeit a less severe one. The lower severity doesn’t necessarily mean lower impact, though. Government assistance is what pushed us through the Great Recession, and that’s unlikely to occur again.

A recession doesn’t have to mean a market crash, but it’s a very real possibility. Some areas are at higher risk of a crash than others. The highest risk metros are those with high loan-to-value ratios, home flipping, new residents, and rapid home price growth. In California, these metros are Riverside, Sacramento, Bakersfield, San Diego, Stockton, and Fresno. Those aren’t the only areas that may be affected, though. Market problems in any one area will also cascade to other regions.

In heated markets, it’s difficult for buyers to negotiate prices down, since their competition will likely be offering more. Now that the market has begun to cool, buyers are looking for ways to pay less. The answer is greater scrutiny of home defects — not to avoid purchasing defective homes, but to reduce the home’s value so they can offer less for it.

Sellers are always required to disclose any significant defects or malfunctions they are aware of in a large range of categories. These categories are walls, windows, ceilings, doors, floor, foundation, insulation, driveways, roof, sidewalks, fences, electrical systems, plumbing, and sewer or septic systems. While it can be difficult to prove that a seller was aware of a defect and the notion that it’s significant is subjective, it’s good advice for the seller to disclose anything they know. Since there’s a high chance something will have to be disclosed, buyers are jumping on the chance to leverage this to negotiate a lower sale price.

When a homeowner sells the home they live in, their most common move is to use the proceeds to buy a replacement property, if they haven’t already done so. While it seems like homeowners would always remain homeowners, it does happen that people transition from homeownership to renting. But in most cases, the seller has decided to sell high and then rent for a short time while waiting for prices to bottom out. This is called timing the market.

This is not what’s happening now. Home prices and mortgage rates are both high, which is pricing homeowners out of their current home — and pricing 80% of them out of the market entirely. They aren’t waiting for a better time to buy; they’re simply no longer able to afford ownership. They become renters by necessity. Fortunately for people in such a predicament, it may not last too horribly long, though certainly longer than they would have wanted. It’s expected that prices will reach bottom around 2025.

Conventional wisdom is that it’s more financially sound to buy a house than rent, if you can afford to do so. However, this may not be entirely true anymore. While house prices and rent prices are both increasing, house prices are increasing at a much higher rate. The gap between mortgage payments and rental payments increased from $25 in April 2021 to over $800 a year later. This difference is the highest in over 20 years. Unless you’re planning to live there for over thirty years, you’re probably better off renting. Importantly, this is based on a down payment of 5%, which is significantly lower than the commonly recommended 20%, but many buyers may not be able to afford a 20% down payment.

This won’t be permanent, but it could last several years. Home price growth has already started to lessen, but interest rates are high right now. Prices aren’t expected to be at a low until around 2025. Increased construction could aid in further reducing home prices. Given that we’re seeing the the beginnings of another recession, though, that probably won’t happen until a couple years after prices bottom out. Even after a return to normality, California is still going to have a lot of renters. With many lower-income workers permanently priced out of buying, the state has consistently had the first or second lowest homeownership rate of any state, frequently swapping places with New York.

With high interest rates, more and more buyers are beginning to realize they can no longer afford to buy, or would prefer to buy something less expensive. Sometimes this moment of realization hits them after they’ve already signed a purchase agreement, and now they want to back out. This is entirely legal, but does come with some potential costs.

When prices are increasing, breach of contract isn’t a huge deal, but can annoy sellers who have to delay their home’s sale. But when prices are decreasing, as is beginning to happen now, sellers have more to lose. Which is why they have a few different options to remedy the situation: they can enforce the purchase agreement, relist their property, or just withdraw the listing and wait for a better time. If the seller chooses to relist, they may be entitled to compensation from the buyer who breached contract. If the profit from the sale after relisting is less than what it would be given the original contract amount, the amount of the buyer’s deposit that would be returned to them is decreased by the amount of the seller’s losses. There may be cases in which there was an agreed-upon limit to this amount, in which case the agreed-upon limit is used, plus an interest rate of 10%.

A certain element of the homebuying process that sometimes crops up, especially in competitive markets, is the homebuyer love letter. This isn’t actually a declaration of love, except possibly for the home they’re trying to buy. A love letter is simply a personalized note included with an offer in an attempt to connect to the seller on an emotional level. Sellers respond to this variously, and may simply ignore them if they’re receiving them constantly.

But the major issue with love letters isn’t the question of their effectiveness. The problem is why they have the ability to be effective. If a seller has a reaction to a love letter — whether positive or negative — and uses this in their decision of which offer to select, it means they’re biased based on some personal detail of the buyer. Most of the information a buyer would provide doesn’t have protected status, but if it does, the seller could be sued for discrimination. Of course, it’s very difficult to prove exactly why the seller accepted one offer over another, so this rarely actually happens even if the buyer suspects discrimination. But this is exactly why some states have banned love letters, or, in the case of Oregon, are trying to ban them.

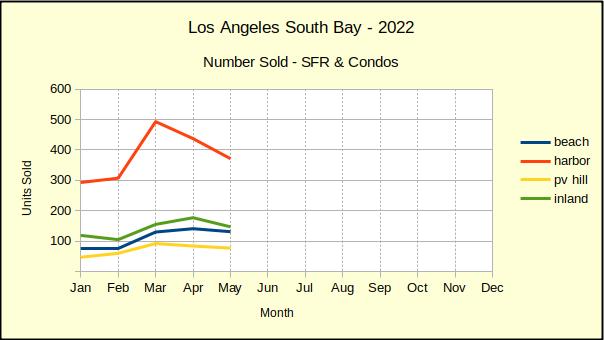

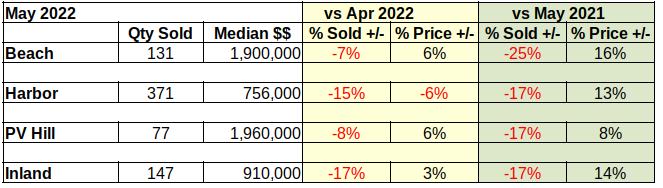

The number of homes sold in the South Bay has declined from last month, and has declined from last year. The quantities are actually rather dramatic given that May is typically a time of increasing sales. The drops range from -7% to -17% lower than April sales of this year, and from -17% to -25% below May of last year.

With over half the year remaining, mortgage interest rates have doubled, currently sitting around 6%. The hike in interest rates has so far reduced the average buying power by about -25%. Coupled with home price increases estimated to have risen 38% since the start of the pandemic, the immediate future of real estate looks dismal.

Inflated consumer prices are also blocking potential home buyers as the Consumer Price Index (CPI) climbs toward a 10% annual hike. There’s little chance of saving for a down payment when the price of everything on the shopping list is going up..

Retirement accounts are often a source of down payment funds. As of this writing the major stock market indices are all down: Dow Jones Industrial Average, -16%; S&P 500, -22%; Nasdaq Composite, -31%. Forecasts are growing for a Fed-induced recession that may begin as soon as this fall. Some potential buyers may see borrowing from their retirement fund to purchase a property as a means to preserve the capital during a recession. Others may not be in a position to do that.

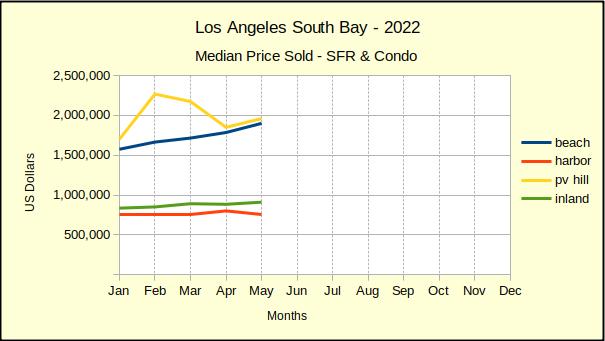

Median Price Sold

May prices delivered a mixed message. The Palos Verdes Peninsula, which had seen two months of decline from a temporarily high median price, headed back up again. The Beach cities continued a steady climb, and the Inland area showed a modest price increase after having dropped 1% in April.

However, the Harbor area, which is as large as the other three areas combined, took a -6% hit to prices. We anticipate the Harbor and Inland areas, which comprise the bulk of the traditional middle class family homes in South Bay, to be the first to react to the economic stress.

Typically, the recession cycle starts with a slowing of sales. As properties languish on the market, sellers begin to reduce prices. One after another, median sales prices will drop until the price reduction offsets the impact to buyers. At that point, buyers will begin to support the reduced purchase prices and we can see growth in the market.

Experts differ in their estimates of how long this cycle will take, and when we can expect the market bottom. There are some predicting a rapid fall based on the speed with which the Federal Reserve Bank (Fed) is reacting. The June meeting of the Fed ended with a .75% hike in the prime rate, and a promise to raise it at least another .75% before the end of the year. While that could slow the economy as early as the beginning of 2023, more conservative minds suggest the end of 2023 for a turn-around.

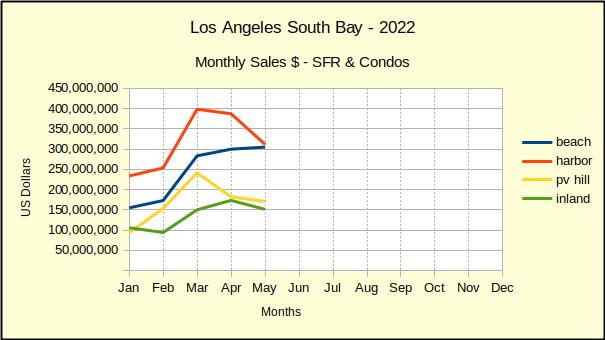

Area Sales Dollars

The total sales dollars tell the truest story. While sales are slowing and median prices are beginning to slow, the combination shows up here.

Everywhere except the Beach is showing reductions in total sales on a month to month basis, and on a year over year basis. The declines are small to date, with year over year ranging from -1% to -10% in May. Month to month changes ranged from +2% at the Beach to -19% in the Harbor area.

These early numbers follow the general pattern we’ve seen in recent recessions, whereby entry level homes are the first impacted and the last to recover. We anticipate the Harbor area to lead the charge down, followed by the Inland area. Recent years have shown the Beach to be the strongest growth area, so we expect the recession to hit there last, following declines on the Hill.

The nature of the impending recession is still uncertain. Some pundits are saying that at least initially we should expect “stagflation,” that odd environment we first encountered back in the 1990s when prices of everything continued to climb, along with job layoffs and massive unemployment. Other forecasters suggest that because the international economy is roiling with continuing high tariffs (courtesy of the last administration) and new monetary sanctions daily (courtesy of the current administration), this particular recession may last much longer than normal.

In Summary

As the table below shows, the majority of the negative impact for May happened in the quantity of housing units sold. With one exception, prices continued to escalate. We believe this is temporary and likely to change before the end of the year. The -6% drop in median price at the Harbor presages the direction of home pricing as inventory grows and listings stagnate.

Approximately 3 out of 4 listings coming across our desk recently have been either Price Reduction or Back On Market. That means property is staying on the market longer. The Average Days On Market (DOM) for May ranged from 10 days on the PV Hill to 14 days in the Harbor area. As recently as this winter we were still seeing multiple offers on the first day the property was available.

Another measure of the market condition is how far the average sales price declines in the first 30 days on market. We did a quick look for May and came up with these statistics. Thirty days after the original listing, the price had dropped from the original: at the Beach, -9%; the Harbor -6%; PV Hill -18%; Inland -5%. As of May, we’re also seeing property that has been on the market for several months, with several price reductions.

Notable Properties

The high and low sales for May were not terribly dramatic. A Manhattan Hill section home and a downtown Long Beach condominium. Thay are simply very big, and very small.

High Sale

Located at 812 5th St, this Manhattan Beach hill section home was originally listed at $10.5M and sold for $8,980,000 after 34 days active on the market. The home offers six bedrooms and seven full bathrooms in 5576 sq ft. Amenities included ocean view, pool, spa, custom waterfall & fire features, a full basement with recreation/media room, home theater, storage, a temperature-controlled wine cellar, and private guest quarters.

Low Sale

Measuring barely 381 sq ft, the studio condo at 819 E 4th St #25 sold for $215,000 in one day. Located in the vibrant East Village of Downtown Long Beach this tiny home offers a remodelled kitchen and bathroom. The unit sits on the second floor, overlooking the intersection of 4th and Alimitos and within walking distance of many downtown shops, clubs and eateries.

While we can all agree that high prices and low inventory is not a recipe for a healthy real estate market, reversing the trend too quickly can cause issues as well. Prices are predicted to start declining towards the end of 2022 and throughout 2023 and 2024. This may be good for prospective homebuyers, but it’s not good for sellers who purchased relatively recently.

A sharp decline in prices could result in negative equity for some people looking to sell, meaning that they won’t be able to sell normally and may have to go into foreclosure. This is not the same type of recession that we’ve just experienced, but it’s a recession nonetheless. Fortunately, it’s not likely to result in a crash, since the continued low inventory is a positive for sellers. The market is expected to begin to stabilize in 2025, but not without steep economic losses.