The initial estimate of the median home price in California in the first quarter of 2023 was $760,260, for single-family residences (SFRs) only. Using this estimate, about 20% of California households could afford to purchase a median-priced home. This demonstrates a rebound from the last quarter of 2022, where it had dropped to 17% of households, down from 24% in the first quarter of 2022.

Affordability is weakest in Mono County, which experienced no change from its very low 7% affordability. The most affordable county has remained Lassen County, despise a slight drop from 54% at the end of 2022 to 53% now. Mendocino County had the largest increase in affordability, an increase of 12% from 14% at the end of 2022 to 26% now. No decreases in affordability exceeded 3% during the same time frame.

Though the US as a whole is significantly more affordable that the rather expensive California, the numbers show a similar trend. Affordability was higher in the first quarter of 2022, at 47%. It had dropped to 38% in the last quarter of 2022 before inching back up to 40% in 2023. Only three California counties — Siskiyou, Plumas, and Lassen — have a higher affordability rating than the national average.

In the US in general, the market has been slowing down. This is leading to a higher inventory — in March 2023, the number of homes for sale was 9% higher than in March 2022. But this isn’t the case in California. In fact, for-sale inventory in California’s largest metro areas was actually down 14% between the same two months. The difference is most stark in San Jose, where inventory dropped 32%.

However, this does have a couple of explanations. Available inventory is a raw number. It doesn’t take into account the number of buyers. Home sales volume is more indicative of the number of buyers, and that dropped significantly more than 14% between March 2022 and March 2023, by 33%. Thus, the ratio of homes available per buyer is actually higher than it was last year. In addition, California is still being affected by lower construction rates, while it has recovered in many other states. The major reason is pushback from local homeowners who don’t want additional construction in their neighborhood.

Real estate is almost always a solid investment. The two major barriers are the high initial investment required and the necessity to manage the property. The former can’t really be fixed, but there are things you can do about the latter. While there is always the option to hire a property manager, this increases the investment required and can make the profits less attractive. Fortunately, there are some other options for real estate investment without being involved in management, which is termed passive real estate investment.

The other options are real estate investment trusts (REITs), real estate crowdfunding, private real estate funds, and exchange-traded funds (ETFs). In all of these cases, you are investing only a portion of the funds. This also reduces the barrier to entry, but at the cost of lower profits. REITs are trusts that own and manage income properties. Investors can purchase shares of REITs that pay dividends. Similar to REITs, ETFs are publicly traded; however, ETFs are traded on the stock market rather than purchased as shares of a company. Real estate crowdfunding and private real estate funds both involve a group of investors pooling money for an investment project. Crowdfunding gives each investor more choice about which projects they’re interested in, which is better for an investor who knows what they’re doing while still not putting the onus of management on them. Private real estate funds are the option for investors who just want to throw money at an investment and not be involved at all, as they are managed by professionals that choose the projects.

A bridge loan is a type of loan that uses equity in your current home to finance the purchase of a new home. Like nearly any loan, a bridge loan has interest and is paid off in installments. Unlike a traditional loan, though, the balance is paid off when your current home is sold. While you don’t technically need to sell your current home to pay off a bridge loan, it’s most useful in situations in which you want to both buy and sell.

Some seller-buyers will sell first, then use the sale proceeds to purchase a new home. However, this comes with potential uncertainties about how long you will be left without a home, especially if you make offers and aren’t successful. You may be staying in hotels or renting for longer than anticipated. Another option is to buy a home first using a traditional loan, then sell. If bridge loans weren’t a thing, there wouldn’t be anything inherently wrong with this. But they are a thing, and this is exactly the situation they’re designed for. While bridge loans do come with a higher interest rate than traditional loans, the length of the loan is typically much shorter. After all, most traditional loans are 15 or 30 years, and no one is going to be waiting that long for a sale to finalize. One caveat of bridge loans is that since they are based on the equity in your current home, if your equity is low, the loan amount will also be low.

When people think of a lien, what most people think of is a mortgage lien, whereby the mortgage lender retakes possession of a property in the event of missed mortgage payments. Most don’t realize that the lien is actually created as soon as you get the mortgage loan; it merely doesn’t have any effect unless the contract is breached. Lien is a rather general term that applies to any situation in which one party has the right to possess another’s property until a debt is paid or waived. One type of lien is a mechanic’s lien, which is the type a contractor can place to use your property as collateral for their work.

There are two broad categories of liens, consensual and nonconsensual. Mortgage liens are consensual because they are initiated by the property owner when they get a loan. On the other hand, mechanic’s liens are nonconsensual, and can’t be placed unless the contractor is legally able to. This means that while a mortgage loan is always in effect in case of a breach of contract, a mechanic’s lien that occurs as a result of the breach of contract can’t be placed until the breach occurs. Breach of contract is only one reason for a mechanic’s lien, though. It can also be placed in the event of nonpayment, unpaid property taxes or fees, deceptive practices by the property owner, or disputes over the work performed.

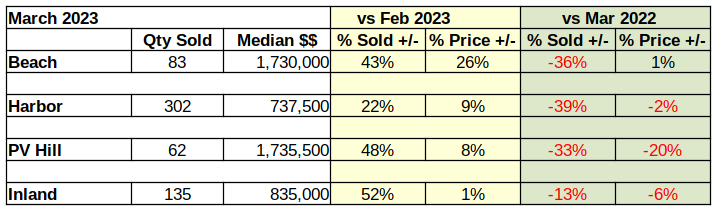

A glance at the table below confirms that year over year statistics are overwhelming the monthly numbers. Buyers were out there buying in March, and they were buying more than they did in February, which was up from January. That’s to be expected. We report actual numbers, as opposed to “seasonally adjusted,” so coming from the depths of winter into spring always increases real estate activity.

Because of that simple fact, the year over year statistics are far more important as an indicator of where the market may be headed. The big increase in March sales doesn’t offset how far down sales volume has gone since last year. Nor does it hint at the level to which median prices are taking a hit.

Compared to last year, sales volume is off by a third in nearly all areas of the Los Angeles South Bay. Median prices haven’t dropped nearly as large a percentage, but we can clearly see the direction. The Federal Reserve System (Fed) comment in the April “Beige Book” said it all: “Residential and commercial real estate activity fell, and lending activity declined substantially.”

Beach Cities Median Still Rising

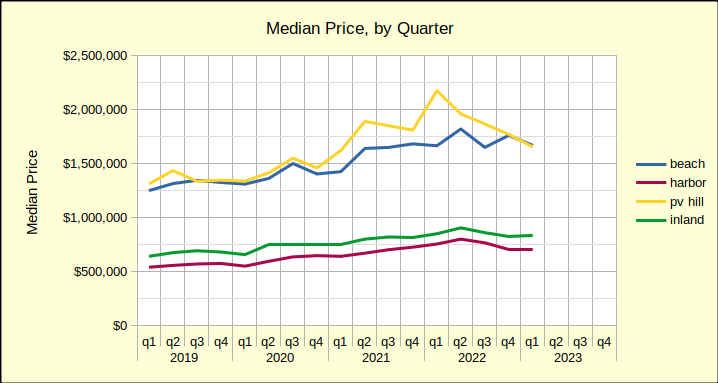

As the over-all real estate market begins a dive into the depths of a Fed-induced recession, we find the Beach Cities as the only remaining local market with year-over-year positive median price growth. It’s not much. A mere 1% growth over March of 2022 is hardly an investment recommendation, especially with inflation running around 6%. And, the rest of the Los Angeles South Bay is already negative compared to this time last year.

This is the second time in 2023 buyers at the Beach have nudged the median price up while the rest of the residential market fell. January showed a 6% increase which collapsed February in a 17% free fall. February’s dismal numbers contributed to what looks like a good March in the month to month measurement.

Staying positive in March appears to be predominately the result of a single sale in Hermosa Beach. At nearly 5000 sq ft, with stunning ocean views, the property was bid up from its $5M dollar list price to just over $6M, closing with a cash offer in only 12 days. Without that transaction the Beach Cities marketplace would have stood at 0% growth.

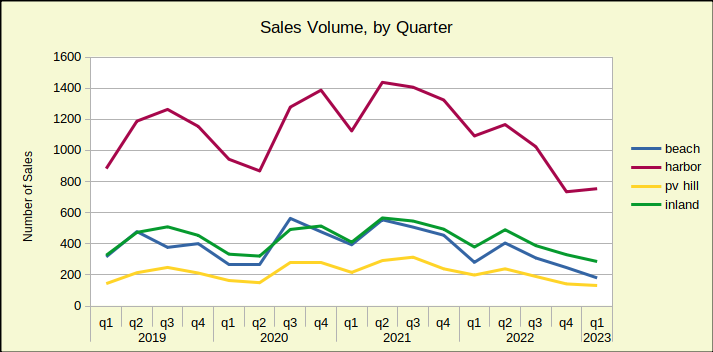

The big story at the Beach is the sales volume versus the most recent “normal” year of real estate business. The chart below shows the number of homes sold in each of the South Bay areas, with seasonal shifts.

Notice that 2019, the last normal year, begins low, with few sales in the winter months. Sales peak in quarter three, in the heat of summer, then decline back down to about where they started.

Compare that to what happened in 2022, when everything seemed to head down.

Only 83 homes were sold in March of this year, and only 181 homes sold across the first quarter of 2023. In 2019 the area averaged monthly sales of over 100 units; approximately 425 homes per quarter. That amounts to a 43% decline in the number of sales compared to pre-pandemic levels.

As this is written there are 152 homes available in the Beach Cities with an average of 62 days on market. Both, the level of inventory and the time on market are increasing daily. Those factors, especially working together, will cause price decreases. With a constantly increasing mortgage interest rate, there’s little doubt the valuation gains of the pandemic era will not hold up to the recession in the world of real estate.

Harbor Area Sales Volume Plummets 39%

The Sales Volume, by Quarter chart above shows relatively synchronous movement across time by three of the four areas. The fourth area, the Harbor, floats at the top of the sales volume chart. Similarly, the Harbor area sinks to the bottom of the median price chart.

Homes in the Harbor area are typically what’s known as “entry level.” They are small homes, often condominiums, and are priced at the bottom of the scale. These are the homes newly wed couples buy, and the homes that house growing families. They are the type of properties occupied by most Angelenos, whether they be homeowners or tenants.

None of that explains the huge swings, though. What does is family economics—cash flow. When both prices and interest rates are low, the entry level market sings. When the cost of home ownership rises, this is the first area to fall and it usually falls the deepest. March sales across the Harbor dropped by 39% from March of 2022. At the same time median pricing at the Harbor dropped 2%–not nearly enough to offset interest rates that are running in the 6%-7% range. Until the mortgage interest rate goes down, or the asking price drops, or both, this market is going to be slow.

Inventory is currently 336 homes on the market, with time on the market averaging 60 days.

Median Down 20% for Homes on the PV Hill

Even more volatile than the Beach, homes on the Palos Verdes Peninsula dropped over a half million dollars in median price from the first quarter of 2022 to the first quarter of 2023. That steep yellow line on the chart below shows the downward direction of home prices in the area. Interestingly, the Beach Cities and the PV Hill declines have been almost exactly the same for the past 90 days.

As noted above, the Peninsula, with its large lots and relatively few homes, invariably shows a lot of volatility. The 20% drop in year over year median price is matched by a 33% drop in sales volume since March of 2022. Much of the median price increase seen last year resulted from a series of new construction sales. Those newly built homes came in at top dollar and helped elevate the median price nicely.

Builders are now anticipating a long, slow recession/recovery, so the PV market is not likely to see that benefit come back for a few years.

This newsletter focuses on residential, but it should be noted the Palos Verdes commercial marketplace has also taken a significant hit since the pandemic. Retail lease prices are at rock bottom and lots of space is available. It would not be surprising to see some of the older commercial space re-configured to meet residential needs. Such a transition could help the cities on the Hill meet their obligation to the State for additional residential construction to alleviate the housing shortage.

Inventory today shows 83 homes available, with an average time of 80 days on the market.

Stability Marks the Inland Area

The “family friendly” Inland Area is surrounded on three sides by the Beach Cities, PV Hill and the Harbor Area. It’s a quiet environment, usually without the drama and speculation found in the more upscale Beach and Hill areas. Anchored by Torrance, the market direction is normally the same as the rest of the South Bay, without the more radical ups and downs. March real estate activity reflected that nature in price and sales volume compared to March of last year.

The “Median Price by Quarter” chart above shows a year over year decrease of 6%, in keeping with annual results from the Hill and Harbor areas. The chart also shows a long, steady green line that doesn’t offer surprises, or dramatic movements in any direction. The current recession is expected to bring prices down somewhat, making the Inland area an excellent target for home buyers, or investors during the coming months.

Available as of this writing, are 130 homes. In keeping with the Inland image of slow and steady, the statistics still show only an average of 47 days on the market. Compare that to 80 on the Hill and 62 at the Beach. Buyers are more abundant here, as long as mortgage interest rates are affordable.

Footnotes

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Two measures went into effect this spring, Measure GS in Santa Monica on March 1st and Measure ULA in Los Angeles on April 1st, both of which enact an additional transfer tax on the sale of very expensive homes, dubbed the Mansion Tax. Measure GS affects properties sold at over $8 million and Measure ULA has two tiers, one affecting properties sold at over $5 million and another affecting properties sold at over $10 million.

Prior to these measures, the transfer tax in both cities was a small dollar value per $1000 of purchase price regardless of property value. Including county taxes, this value is $5.60 in Los Angeles, and Santa Monica has two tiers, one at $4.10 per $1000 and another at $7.10 per $1000. Measure GS added a third tier to the Santa Monica system, which is a significantly higher $56 per $1000 value for homes over $8 million. Los Angeles still only has one base value of $5.60 per $1000, but with an additional tax of 4% for homes between $5 million and $10 million, and 5.5% for homes over $10 million.

Spring is already halfway over, so if you’re planning to sell your home this season, you should get on it quickly. Especially since you may need to do some sprucing up to get a good deal. If you bought your home during or shortly before the pandemic, this may be your last chance to benefit from the spike in prices. But buyers aren’t simply snatching up any home they see, like they were during the pandemic. They’re being more deliberate, so you need your home to be appealing.

This means all the standard procedures for increasing your home’s appeal apply. These include things such as repairs, upgrades, repainting, curb appeal, and staging. In some markets, you can get away with not doing these things, or only doing some of them, because the buyers are happy to purchase a cheaper home and perform the upgrades themselves. Not the case this spring. The seller will have to make the investment, which hopefully translates to a higher price as well.

For the past couple of years, house prices had been rising dramatically across the country. Here in California, we’re now starting to see prices drop since the start of this year. Prices are now falling in all 12 major housing regions west of Texas, as well as in Austin, TX. The same can’t be said everywhere, though. In the 37 largest metros east of Colorado, excluding Austin, TX, prices are still rising. Of course, markets can differ drastically by state, but such a clear divide between eastern and western US may be unprecedented.

Falling home prices was the expected result of the federal benchmark rate hikes. It seems to be working in the western US, as prices become too unsustainable to continue to increase. The regions with the most significant price drops are the ones that were rather expensive. But there are still other factors at play in the eastern US, driving prices still upward. Some areas, such as Hartford, CT and Buffalo, NY, never reached unsustainable home prices and remain rather affordable. They also have rather low inventory. These factors combined are keeping prices from dropping, leading to an 8% increase in prices in January. Florida is attracting many new employees with multiple financial companies relocating to Miami in 2021 and 2022. Prices are expected to eventually start falling even in the east, but don’t expect anything drastic. Low inventory across the country is preventing any sudden market collapse.

Wrap-around mortgages are not very common, but it’s still a good concept to know in case you find it difficult to get a more traditional mortgage loan. A sale with a wrap-around mortgage has two important components distinguishing it from a regular sale: First, the seller retains the current mortgage on the property being sold. This differs from standard sales in which the seller normally pays off the remaining mortgage as part of the sale process. Second, the loan is not issued by a lender but rather by the seller. In this way, the seller is most likely planning to pay their mortgage using the money gained from payments the buyer makes to the seller on their new mortgage.

Wrap-around mortgages have both advantages and disadvantages. The primary reason to get a wrap-around mortgage is that they don’t have any standardized qualification requirements. This mostly benefits the buyer, but can also be useful to the seller if they’re having difficulty finding buyers. The primary drawback is that the buyer and seller must write up the contract themselves, since there is no lender involved. That means both parties need to be legally and financially savvy. It’s also impossible to wrap around a mortgage that doesn’t exist, so the seller needs to have a mortgage. There are also cons specific to the seller and buyer. The seller in this instance incurs the same financial risk that a lender would normally. The buyer is very likely paying a higher interest rate, since the arrangement is not worth the risk to the seller unless they are profiting.

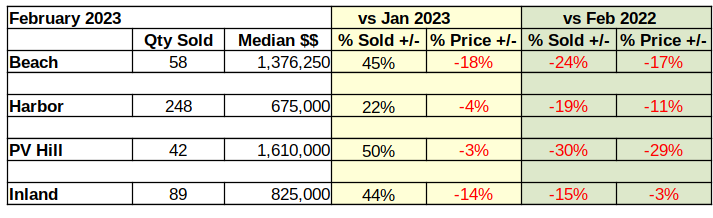

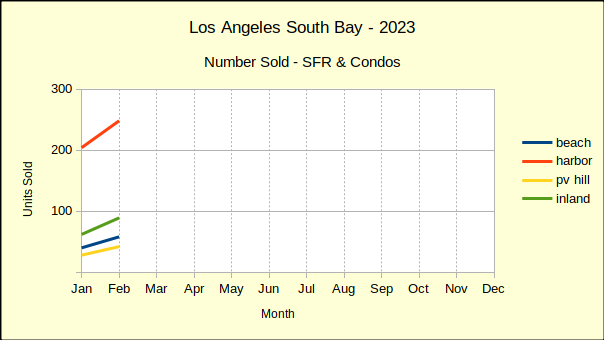

Last year ended with sales volume off, median prices coming down and revenue dropping fast. January showed little change. February of this year shows sales volume up from January by as much as 50%. The reason why is obvious–the median price is simultaneously dropping by percentages as high as 18%.

Comparing February activity to February a year ago shows significant declines in both sales volume and in median price. At that point in 2022 the market was just beginning to dip a toe in the recessionary waters. Now we’re wading into it.

The first week of March Fed Chairman Jerome Powell told Congress, “…the ultimate level of interest rates is likely to be higher than previously anticipated.” Powell’s pointed remark clearly tells us the most recent pause in interest rate hikes is momentary. The lowest local mortgage rates we could find at the time was 6.75%. As such, we anticipate rates in excess of 7% by summer.

February Sales Volume Climbs

About the second week of January mortgage lenders began loosening the interest rates in anticipation of a relaxation by the Federal Reserve. For the most part, local rates stayed below 6% until late in February when the Fed began dropping hints that inflation was still raging.

After a “soft” January, sellers in the market were dropping prices and buyers responding positively by making offers. Now that mortgage rates have resumed climbing, sellers will have to drop prices some more to remain attractive to buyers.

With only two months behind us this year, there are indications lenders will “see-saw” the rates throughout the year. Already this year we have seen retail mortgage rates moving up and moving down without influence from the Fed. It seems to be an effort to induce buyers to accept high interest rates based on the theory they were higher last week so this temporary reduction is a good deal.

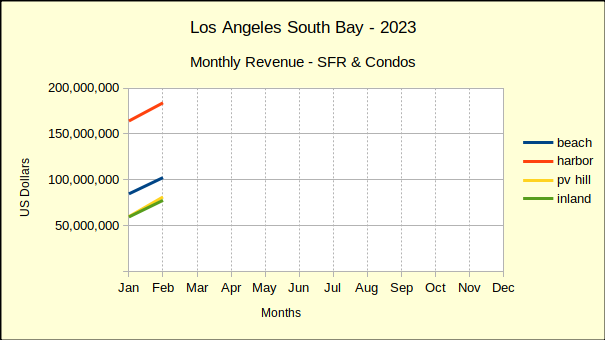

RevenueClimbs From January Depth

On a month-to-month basis, revenue across the South Bay is up 21% from January of this year. Don’t get excited—it’s only one month. January was one of the lowest performing months we’ve seen recently.

On a year-over-year basis, revenue is down 34% from last February! January was 38% lower than January of 2022. Year to date through February, revenue in the South Bay is down 36% and is expected to continue falling.

One of the more important statistics to note is how 2023 activity compares to 2019, which was the most recent “normal” year of real estate business. Across the South Bay real estate revenue for the first two months of 2023 is 7% below the same period in 2019. Restated, the South Bay has already lost over four years of gain in real estate revenue.

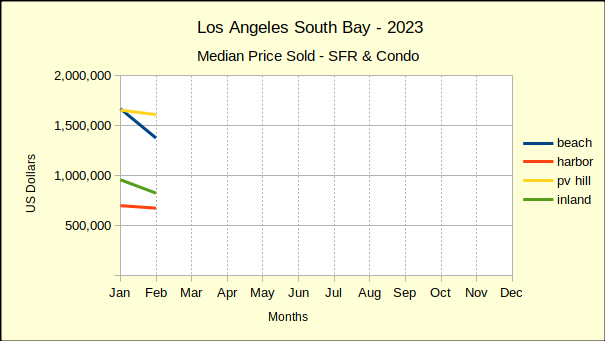

Median Price Slips, Volume Rises

More units of housing were sold in February than January, and the median price was lower in February. The Beach Cities saw a drop of 18% from January while the PV Hill held the decline to 3%. The Harbor area fell 4% and the Inland area dropped 14%.

Comparing February of this year to February of 2022 brought a harsher focus to the picture. All four areas have fallen from last years median price. The Beach is down 17%, the Harbor down 11%, the Hill is off 29% and the Inland cities down just 3%.

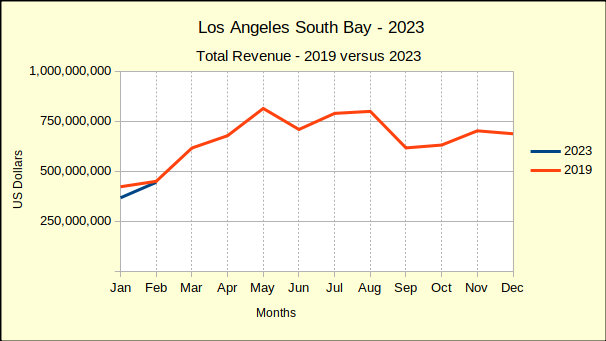

2023 Versus 2019 Shows a Sinking Market

The summary numbers comparing the first two months of 2023 to the most recent “normal” year of 2019 are not encouraging. Overall, sales revenue has fallen 7% below revenue figures for the same period in 2019. The Harbor area has fared the best, showing a 9% increase in revenue over January and February activity in 2019. Of course, that was four years ago and classic inflation would give that type of gain. It’s clear the “inflation on steriods” we’ve been experiencing is gone from the real estate industry.

The Beach cities provide an excellent indication of where the real estate economy is going. The first two months of revenue for 2023 is down 32%. Palos Verdes is down 2%, while the Inland area is up be a mere 1%. After four years of pandemic, recession, inflation and Federal Reserve manipulation the real estate market is tanking.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Real estate articles will frequently talk about first-time buyers, since they are a significant proportion of buyers overall. Less discussed are first-time sellers. It may be time to change that, since it seems like they could use some advice from experts. In the past two years, 84% of first-time sellers wished they did something differently during the sale process. The four things first-time sellers most regret are their decisions regarding pricing, online presence, timing, and repairs.

The most frequent comment was that they should have priced their home higher. Of course, that depends on the market. That may have been true when they sold, but don’t necessarily take that to heart. It’s also possible to list too high, which may be a more common regret this upcoming spring. Regardless of the list price, though, 90% of first-time sellers believe they could have done something to get a higher price. For 39% of them, this may be better listing photos. Virtual curb appeal is important nowadays when many people are looking online for their purchases. Since listings with virtual tours get 69% more views, this could boost your chances by quite a bit, and 25% of people agree a virtual tour would have helped. According to Zillow, the optimal time to sell is the second half of April. Not everyone has the flexibility to do this, but 25% still wish they listed at different time. 36% also didn’t have a good idea of how long it would take to sell. Even though 66% of first-time sellers completed at least two home improvements before selling, 25% believe a bigger investment in repairs or improvements would have increased the sale price.

Most agents are probably familiar with a pocket listing, but if you aren’t an agent, you may not know what that is. Even if you do know what it is, you may not realize why they’re a problem. A pocket listing is a listing that is temporarily exclusive, before a delayed release into the open market. At first glance, this can seem like a win-win-win situation. Sellers don’t need to do as much preparation and their agent can vet the buyers for them. Buyers don’t have to deal with nearly as much competition. The agent gets double the commission by representing both sides.

However, it’s not all upside. There are also plenty of cons to pocket listings, and they may outweigh the benefits. A big problem is that pocket listings simultaneously skew the market while not being governed by the market. Not listing the properties on the market reduces inventory values, which skews both competition and prices upward, significantly hurting buyers overall. You may think this benefits the seller, but it actually doesn’t. Because the pocket listing isn’t governed by this upwardly skewed market, the buyer of a pocket listing is likely to pay significantly less than the distorted high prices. In fact, because of the total lack of competition, they’re likely to pay less than the actual market value. For the agent, being a dual agent is a lot of work and stress, and it’s only increased by attempting to make it a pocket listing. In the event the seller suggests a pocket listing, this isn’t as much of an issue. But an agent truly can’t push for a pocket listing without breaching their fiduciary duties to the seller, which include taking reasonable steps to locate a buyer. Even if it’s on the seller’s suggestion, there will always be a conflict of interest when representing both sides that the agent will need to delicately navigate.

No matter which region of California you’re looking at, things initially appear pretty dire for home sales. From December 2022 to January 2023, it’s down in every single major area. The decrease is smallest in the Inland Empire at 15.4% and highest in the San Francisco Bay Area, where sales dropped 38.1%. They also dropped significantly in the Central Valley, by 30.8%. Even in the Far North, where prices actually increased by 4.9%, home sales are down 18.4%. Most regions experienced a decrease of approximately 19%.

However, that rate is not seasonally adjusted. Winter is the slowest season in terms of home sales, so it makes sense that sales would be down. One rate that is seasonally adjusted is the statewide single-family residence (SFR) data. With sales being down in every region, you’d expect sales to be down statewide, since those regions do encompass the entire state. But with seasonal adjustment, we discover that the month-to-month SFR sales actually increased ever so slightly, by 0.4%. In fact, this was the second straight month of seasonally adjusted increase in SFR home sales. It’s hard to say just yet whether this is an overall increase in market confidence, or simply preparation for the often-hot spring season, but in either case, expect sales to increase. If spring sees not only an increase — which is expected regardless — but a seasonally adjusted increase, then we’ll know that market confidence has improved.

Spring is almost always the hottest season for real estate. It’s very likely that it will be this spring, as well. However, things are going to be a bit different. The market feels somewhat volatile at the moment, with prices having plummeted rapidly immediately after a dramatic increase. Mortgage rates, having reached their peak, are now beginning to tick down over time, but it’s hard to gauge rates on a day-to-day basis. Sales can’t be predicted at all based on job growth, since the job growth is primarily reduced unemployment. This uncertainty is going to make buyers more cautious than usual this spring.

That’s not necessarily a bad thing if you are looking to buy, though. Prices may not be at their lowest point, but they don’t have much farther to fall given inflation. Mortgage rates are no longer inordinately high. And importantly, competition isn’t going to be as high as it is most spring seasons. That means you have time to shop around, look for the best deals, and watch how the market pans out. If you get out there looking now, you’ll have a better idea of where the market stands by the time you find something that’s right for you. But make sure you’re prepared to buy and have a pre-approval. If you wait too long, demand will start to go back up as mortgage rates continue to fall, and suddenly you have competition.

Much of the slow progress of zoning reform can be attributed to Not-in-my-backyard advocates, or NIMBYs for short. This refers to the homeowners that are resistant to reform because they believe it will decrease their home’s value, thus reducing their future sale profit. One big target for NIMBYs is low-income housing. It’s true that low-income housing is probably less valuable itself than the NIMBYs’ homes; however, to assume that it would drag down the value of nearby homes is simply inaccurate.

In fact, the addition of low-income housing actually increases the value of mid- and high-tier housing within a half mile radius by about 4%. There are a few different reasons for this. First, low-income housing in mid- or high-income areas generally also translates to multi-family residences. Higher density housing means an uptick in population density, which also usually increases home values. In addition, new multi-family housing construction is most often replacing either tear-downs or vacant lots. The area’s average value would actually increase just with that new construction alone, without any change to nearby home values. Finally, in areas that are already experiencing price growth, low-income housing further accelerates it by increasing existing high demand in that area.

The housing shortage we’re currently experiencing has been attributed in large part to lack of construction. There’s a lot more to the story, though. First of all, the slow construction doesn’t even account for all of our housing shortage — there are other factors such as increasing population, a rapidly changing housing market, and vacant homes not for sale or rent. As far as construction, the problem isn’t merely a lack of it. It’s true that construction dropped significantly during the pandemic, but it’s mostly recovered now. The actual issue is that the homes being constructed are frequently not adding additional units.

The statistics you see when looking at construction starts account for all types of construction. However, much of the construction that’s occurring right now isn’t on vacant land. In 2021, 76% of builders reported that the number of available lots is low to very low. In California, a lot of this has to do with zoning laws. Many areas aren’t zoned for multi-family residences or even for residences at all. Even in areas that allow condos or apartment buildings, single-family residences (SFRs) are in higher demand in California. Building SFRs in the right place is also difficult. 28% of SFR construction is reliant on lots called infill sites. While these are vacant land, which is good, they’re in areas that already have a high density of housing and are less in need of additional construction. A further 20% of SFR construction starts come after teardowns, merely replacing one SFR with another SFR.

One of the statistics used to track health of the rental market is Fair Market Rent, or FMR. By the name alone, one might think FMR is a normative measure that suggests what rent prices should be. Of course, such a measurement would have to take into account construction costs and home prices, but it would also have to take into account the tenant’s income. As a renter, you may be looking for rent prices at or below FMR thinking anything above that is simply a bad deal. But is it actually fair to anyone? Is it even a normative measure at all?

The first question that needs to be answered, though, is: What really is FMR? Well, at its core, it’s a series of vague estimates. The Department of Housing and Urban Development (HUD) calculates FMR on a per-metro basis for five separate categories of homes based on number of bedrooms. Homes with more than 4 bedrooms are excluded entirely. In reality, though, only one category is actually calculated. This is the category for the average home size of 2 bedrooms. The median rent price of 2 bedroom homes, excluding outliers, is averaged over a multi-year period, then the value is multiplied by various ratios to determine FMR for homes of different bedroom counts. Note that this calculation doesn’t factor in either construction costs or income, just rent price, although the price itself generally is indirectly related to constructed costs. This means that if it’s fair to anyone at all, it can only possibly be whoever bought the home. So, no, looking for a rental at or below FMR has no bearing on whether it’s fair to the tenant.

Does FMR perhaps still have some use, though? Though it’s a multi-year average, it’s based on actual rent prices, so maybe it be used to estimate current rent values. It’s a decent assumption, but unfortunately, it’s not actually very good at estimating rent prices. If you’re looking at FMR when considering whether to move to an area, don’t be surprised if your actual rent is far different, especially for multi-bedroom homes. Multi-year averages can’t very easily take into account economic cycles, and broad examinations of metro areas can significantly skew the numbers. Another issue the calculation faces is the notion of rent control. Rent control doesn’t generally happen in an entire metro, so the prices of rent-controlled units are significantly more likely to be taken as outliers and completely dropped. Even if they aren’t dropped, they will skew the median.

For a specific example, let’s take the local area — the Los Angeles metro. This metro area is rather large, and includes multiple cities of highly varied income levels. Despite this, the FMR for the Los Angeles metro is actually lower in every single category than that of the City of Los Angeles. The LA metro FMR for a studio is $1631, quite a bit lower than than actual median rent price for a studio in Los Angeles of $2100, between mid-June and mid-December. The difference only gets larger the bigger the home. The metro’s FMR for 4 bedroom homes is $3377. But the actual median rent of a 4+ bedroom house in LA is $8995, over 2.5 times as much. Considering homes larger than 4 bedrooms to be outliers, as the FMR criteria do, doesn’t do much to help the case for FMR, as the actual median rent is still $7900. The disparity is even greater for higher income regions of the metro, such as the Beach Cities — Manhattan Beach, Hermosa Beach, Redondo Beach, and El Segundo — with a studio median of $2495 and a 4+ bedroom median of $9175. This suggests that high-income units are being excluded as outliers, which isn’t particularly useful if you’re looking to rent in a place such as Manhattan Beach.

Why is FMR lower even for smaller homes, though? Well, there may be a valid reason for that. The actual median data presented here is calculated using information from a Multiple Listing Service (MLS), which is a service used by real estate agents to upload and search listings. Because this is an agent service, only properties listed by an agent will appear in the list. For lower income rental properties, the owner is less likely to use an agent, because they may feel it’s not worth the expense with a small revenue. But the HUD can access that information, which could drag the median down for smaller homes. So, the FMR may be useful to a tenant planning to rent a low-income property. However, remember that the studio FMR isn’t directly assessed, but rather calculated as a ratio of 2-bedroom FMR, so if FMR is more consistent with real values for studio rentals, this is at least partially coincidental and could mean either the 2-bedroom FMR is low or the ratio is off. Moreover, off-market rentals do very little to explain any disparity for larger homes, and especially not such a large disparity.

We’re taking a little different approach with this post. Because it’s not only the end of the month, but the end of the year, we’re doing a quick summary of the monthly data, followed by some more detailed discussion of how the individual areas have fared over the past year. We’ll even try some crystal gazing while we walk through the annual data for each neighborhood.

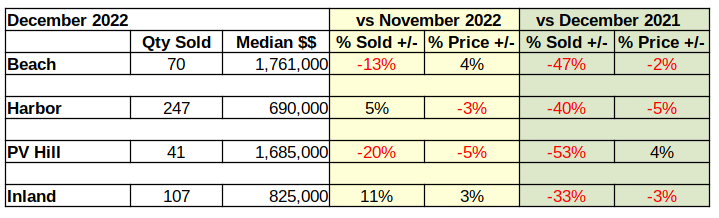

This is a great place to bring in our At A Glance table. It displays in just a few numbers how all the areas of the LA South Bay are doing compared to last month, and compared to this same month last year.

Looking at December vs November, once again the percentage of unsold homes has increased and the number of homes sold below last month’s median price has also marginally increased. More importantly, on a year over year basis the amount of red ink is even greater. Losses in number of sales and in the value of those sales is clearly growing.

Despite all the negative numbers, there may be a light in the future. For the past couple weeks we have observed a softening in the mortgage interest rates. If that turns out to be more than a mid-winter teaser rate, this spring may shine a bit brighter than previously anticipated. We’re not holding our breath though. Recent speeches from Federal Reserve Bank leaders have stated a clear intent to “hold the line” on driving down inflation with mortgage interest rate increases.

Beach Cities Home Sales Down 47%

Compared to 2021, fewer homes have been sold in the Beach Cities every month of 2022 than the same month the previous year. January started the trend with a decline of 28% versus the number of homes sold in 2021. That difference continued to increase all year. By December sales were 47% lower than the previous December.

As the interest rates climbed, the number of home sales dropped. Looking at the total sales volume for the year, 35% fewer homes were sold in the Beach area during 2022, than were sold in 2021. Of course, 2020 and 2021 were the highly erratic pandemic years. So, looking into sales at the Beach for the last few years we find the number of homes sold has already dropped 21% below the number sold during 2019, our last normal economic year. Effectively, the Covid-19 pandemic created. Then erased any gains of the past three years at the Beach.

Homes sold in: 2019 – 1572 (market normal) 2020 – 1572 (market direction down six months, up six months) 2021 – 1910 (market direction down two months, up ten months) 2022 – 1242 (market direction down twelve months)

While the Beach Cities suffered the largest drop in sales volume for 2022, the South Bay as a whole has also dropped below the sales figures for 2019.

Sales Volume Down Across the Board

All areas started the 2022 year down from the prior month and down from the same month in the prior year. February results were mixed with the Harbor and Palos Verdes areas showing stronger results. March sales jumped up as buyers realized the rising interest rates were about to price them out of the market. From April on, sales volume across the South Bay was trending down on a year over year basis.

In sheer number of sales, the Harbor area fell the farthest. In 2021 annual sales 5292 homes were sold in the Harbor cities, while in 2022 the number dropped to 4017. That amounted to only a 24% decrease compared to the 35% annual collapse in the Beach areas.

On a month to prior month measure, sales declined six months out of nine across the South Bay. Occasionally one or two areas would post a positive sales month, but in the end, 2022 showed a 26% drop in sales volume from 2021 across the South Bay.

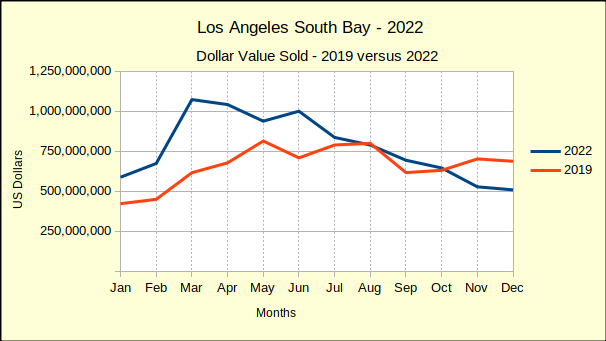

Sales Dollars Diving

With the number of sales dropping in a range of 25% to 50% it’s not a surprise to discover the total dollar value of those sales has taken a dive. As the chart below shows, the first quarter of the year was generally positive, then reality set in and the buyers started walking away. The rest of the year was little more than a measure of the recession.

Monthly revenue in the Harbor area alone dropped $200 million between March and December. The Beach cities and the Palos Verdes area lost about $150 million a month in sales value. Inland area sales for the same period are off approximately $75 million.

One should consider these declines in the context of the pandemic. Early on, while much of the world was in lockdown, the government flooded the citizenry with easy money, hoping to keep the economy afloat. Mortgage interest rates were already at the bottom because the economy was just recovering from the last recession. The result was a real estate boom starting in summer of 2021, which continued until March of 2022.

The housing market is now in the “bust” part of the cycle and we anticipate it to last through 2023. Gross sales across the South Bay jumped up from $8 billion in 2019 to $12 billion in 2021. That’s clearly unsustainable, especially from the perspective of a Federal Reserve System which is looking for 2% growth. So far the market decline has taken back about 23% of that $4 billion bubble.

Median Price Is Slipping

There is a lull between when buyers stop buying and prices start dropping. Most sellers need to see headlines about the market change before they make a price reduction. Median prices started to slide in August at the Beach and on PV Hill. The year ended with most areas having experienced multiple monthly declines in the median price. Despite that, median prices still exceeded those of 2021 by roughly 7%.

Comparing 2022 to 2019 better shows the inflation factor. Generally speaking the South Bay ended the year with median prices 30%-35% higher than they were in 2019.

The Palos Verdes market is comparatively small, thus is typically volatile on a monthly basis. The yellow line on the chart above shows the range of high and low median prices. Since mid-year the median price has drifted down and merged into the downward trend.

Year End Versus 2019

We’ve been comparing 2022 to 2019 all year because real estate sales during the height of the pandemic were so out of the ordinary, regular year over year comparisons yielded untenable results. The chart below depicts the current year total sales for the South Bay compared to sales from 2019.

Tracking the blue line, one can see where sales dropped below 2019 values in August, recovered in September, then slipped below again for the fourth quarter of the year. December sales didn’t fall quite as far as projected, but still came in about $200 million less than December of 2019.

The end of the year reflected accumulated sales of approximately $9.3 billion. That would mean 2022 total dollar sales come in at $1.3 billion above the $8 billion total dollar value sold in 2019. Across the South Bay that was an 18% increase.

Broken out by community, we found total dollars sold in the Beach cities to be 4% above 2019, followed by the Inland area with a 20% increase. Harbor came in next with a 21% increase and the PV Hill with a 35% increase.

We expect both sales volume and median price to continue declining through most, if not all, of 2023. By mid-year of 2024 there should be evidence of the beginnings of a recovery.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Data from December 2022 shows us that home prices in California are unquestionably going back down. December 2022’s median home price of $774,580 was just barely below November 2022’s median price, only by 0.4%. This isn’t necessarily a trend, but what is a trend is that it’s 2.8% below prices at the end of 2021. Home prices are down in every major region of California, and across both single-family residences and condos. However, all regions except for the San Francisco Bay Area had at least one county experience price growth.

The far northern regions of California had the most notable shifts. Year-over-year, prices are down a whopping 41.8% in Lassen County. Granted, this isn’t a massive dollar value given that Lassen County is the least expensive county in the state, with a median home price of just $170,000 in December 2022. Even so, it was actually the third cheapest at the end of 2021 — both Del Norte County and Siskiyou County were cheaper in December 2021, but both actually experienced price growth this past year. In fact, Del Norte was the county that had the most significant price growth at 13.8%. Del Norte and Siskiyou counties both border Oregon, and Lassen County is just south of Modoc County, which also borders Oregon but is not included in the rankings.