The average time it takes to sell a home from listing with an agent to closing the sale is about 90 days. Many factors affect how long it takes to sell a home. These elements can include market conditions, buyer financing, the time of year, and the prep time to get a home ready for marketing.

A home that is in good condition, has good curb appeal, and is in a good location will attract buyers more quickly. Competitively pricing a home is key to having a reasonable time on the market. A cash buyer and one who is willing to buy a home in as-is condition can expedite the closing time.

Once an offer is accepted, the average closing time will be 30 to 45 days. The buyer’s loan is processed during this time along with the lender obtaining an appraisal. Property inspections also occur during the closing process. The title and escrow companies will then coordinate the signing of all the final documents, collect the buyer’s closing funds and finalize the settlement statements so the transaction can close.

As of August 2023, interest rates are somewhere around 7%, possibly higher. While this isn’t astronomically high — they have historically been over 10% — it’s too high for current homeowners to want to exchange their homes. This is because 92% of current homeowners with a mortgage have an interest rate below 6%. Almost a quarter even have locked in an interest rate below 3%.

High home prices are actually somewhat helping current homeowners, since the price boost increases their equity. Prices have increased 14% in the past two years, which results in approximately $86,000 in equity over that time period. However, this may not be enough to offset the increased mortgage costs, especially for those with very low interest rates. Assuming a mortgage of $500,000 and a current interest rate of 3%, a new purchase with the same loan amount would result in a $1,200 increase in mortgage payments per month.

Normally, when demand is low like this, supply is high. This isn’t the case right now. Previously, we would have been able to blame declining construction due to increased construction costs. That’s no longer the case, though, as construction has largely, though not completely, recovered. It may even be simple lack of demand that is the final obstacle to a full recovery for construction. To see the real problem, remember which group we’re talking about — current homeowners. These are the same people who would be selling to buy a new home. If they’re not willing to buy in the current mortgage climate, they’re not selling either.

The share of teachers able to afford homes near where they teach is dwindling rapidly. This year, teachers can afford only 12% of homes within 20 miles of their schools. This is a decrease from 17% last year. In 2019, before the pandemic, they could afford 30% of homes in their school’s area. Fortunately, there are options to help teachers.

The Department of Housing and Urban Development (HUD) is sponsoring a program called Good Neighbor Next Door, which sells homes in revitalized areas to certain government workers at half the listing price. This program is available to pre-K through 12 teachers as well as law enforcement officers and firefighters. Some of Fannie Mae’s programs, while not specifically aimed at teachers, have qualifications that teachers frequently are able to meet.

In addition to federal programs, there are also state and private programs to help teachers. California created the School Teacher and Employee program back in 2018. This specific program is discontinued, but is now folded into their MyHome program, opening it up to more people. The private program Homes for Heroes provides a 0.7% rebate on home purchases made through the organization’s specialists. It is available to firefighters, EMS, law enforcement, military, healthcare professionals, and teachers.

Real estate agents make their income from commissions when they represent buyers or sellers on the sales of homes. By law, the amount of commission charged must be negotiable. The industry average is 5% to 6% of the home sale price.

Although the percentages of the split may vary, traditionally, a 6% commission would be divided between the listing broker’s office and the selling broker’s office. The listing agent represents the seller, and despite the name, the selling agent is the one who represents the buyer. Three percent would go to the listing broker’s office, which would be split between the broker of record and the listing agent, per their office agreement. Likewise, the other 3% would be split between the selling agent’s broker of record and the selling agent.

For example, if a seller agrees to pay a 6% commission on a $1,000,000 sale price for their home, the total commission paid at closing would be $50,000. Of that, $25,000 would be disbursed to the listing office, where the agent would be paid $12,500 or more, depending on the agent’s commission agreement with the broker. The other half would be shared between the buyer’s brokerage and agent. Agents also generally pay Errors and Omissions insurance premiums as well as other transaction fees.

Year to date through July, the gross revenue for South Bay is a mere 3% above that of 2019. At the same time, sales volume, the number of homes sold, is 23% below the sales of 2019. By most standards, 2019 was the pinnacle of real estate business prior to the turbulent years of the Covid pandemic.

Many sources compare current business to that of the pandemic years, partially because it’s easy and partially because the “numbers look better.“ Undeniably, the statistics do look more favorable, however, this analysis takes comparisons beyond the normal “last month” and “same month last year” to include 2023 versus 2019. This allows our readers to see 2023 in a historical context and to more readily recognize the unfolding recession.

While median prices are still above those of 2019 right now, we project the median prices will also drop below the 2019 level before this recession ends. On a month to month basis, prices are falling approximately half the time. On a year to year basis, 2023 prices have dropped below 2022 medians 82% of the time. Median prices for June and July of 2023 fell below 2022 in all four areas both months. Buyers and sellers should anticipate the bottom of the recession in late 2024, or possibly 2025. Normal growth should return in 2026.

The July report from the Federal Reserve Bank (Fed) notes that inflation is expected to continue above the target of 2% through 2025. Accordingly, the Fed efforts to “restrain” the economy (meaning increase interest rates) will continue into 2025. The report indicates that while housing costs are slowing, they continue to increase at inflationary levels, necessitating further reduction.

In the meantime, buyers who are financially able should plan to acquire desirable properties at substantially better prices than will be available after recovery begins. Sellers who anticipate a need to sell before the economic turn-around, should look toward selling sooner rather than later, to minimize the impact of the down-trending market.

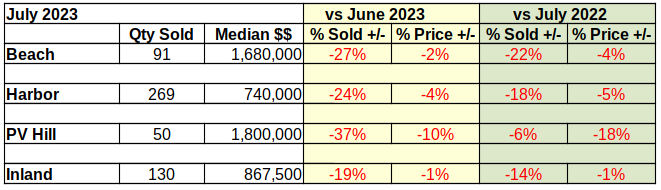

Beach Cities Summer Market Fizzles

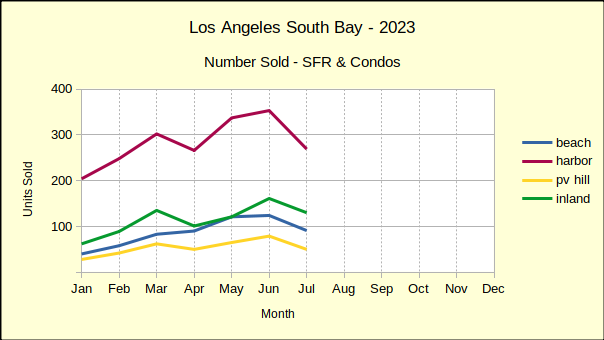

From June to July the number of homes sold in the Beach Cities fell 27% and those sold for a median price of 2% less. Some of the decline in sales is attributable to fewer homes available, as sellers hold properties off the market in hopes of improving conditions. Even more is a result of buyers who have lost significant purchasing power as mortgage interest rates have rocketed to over 7%.

Compared to July of 2022, the number of homes sold this July dropped 22% with a decline in median price of 4%. This set of statistics is somewhat deceptive in that last July the real estate market was still in the early stages of the downturn. As the current year progresses, year over year figures will demonstrate the slide more clearly.

Comparing the first seven months of 2023 to both 2022 and 2019 (the most recent year of business not impacted by the pandemic) shows the drift of sales and prices. The number of homes sold fell 24% from 2022 (802 homes) to 2023 (607 homes), while it was down 35% from 2019 (930 homes). The Fed dropped mortgage interest rates to essentially zero during the pandemic to keep the general economy afloat, which resulted in rapid price escalation which ultimately made purchasing a home unaffordable for about 25% of potential buyers. Then to control the resulting inflation, the interest rates jumped up around the 7% mark, which further slowed the real estate market by “pricing out” another 10-15% of buyers. With fewer buyers and stagnating prices, sellers are reacting by pulling property off the market and delaying planned sales.

Median prices fell 4% from 2022 and are still 28% above the median price of Beach Cities homes in 2019.

Harbor Area Sales VolumePlummets

Sales volume in the Harbor area has held up better than the Beach, possibly because median price has taken a greater hit. On a monthly basis, 24% fewer homes were sold (269 in July versus 353 in June). Comparing July of 2023 to July of last year, only 18% fewer closed escrow (269 versus 329).

Generally being an entry level market, the Harbor area tends to react faster to changes in market condition. More upscale neighborhoods frequently “stick to the price” for a longer period of time when markets are declining. Month to month median price dropped 4% in July to $565K. For July of 2022 versus July of 2023, the median fell 5%, from $780K to $740K.

Year to date through July, sales volume was off 24% from last year. Median price was down 4% when compared to the same period in 2022. Looking back to 2019, the number of homes sold during the first seven months of 2023 dropped by 21%. Median price for the same time frame shows up at 32% higher than 2019. Given the median price dropped 4% over the past month (from $772K to $740K), it’s reasonable to project the Harbor area median will end the year near $600K, as it was in 2019.

PV Hill Shows Volatility

Month over month, the number of homes sold on the PV Hill fell from 79 units in June to 50 in July, a decline of 37%. At the same time, the median price dropped 10%, ending the month at $1.8M. This despite a high sale of $12.5M, up from the high of $10M in June.

Year to year, July volume dropped 6% from 53 units in 2022, while median price plummeted 18%, from last year’s $2.2M. Palos Verdes is a unique community with large homes on large lots, many of them highly custom. Combined with the small overall number of homes, these properties truly need to be assessed on an individual basis for realistic projections.

Comparing cumulative sales data for January through July, volume is down 23% and median price is down 17% versus last year. Going back to the stable year of 2019, the number of sales is down 16% while the median is up 34%.

Interestingly, if the Fed’s annual 2% inflation target is added to the years between 2019 and 2023, the median on the Hill would be $1.5M today, instead of $1.8M. Under those circumstances, it would only take a decline of $300K to erase all gain from the past three years. Not a comforting thought for anyone who purchased recently.

Inland Cities Most Stable

The Inland area typifies a classic “middle of the road” performance in the real estate world. Generally the homes are everyday family properties, the sales trends are at the middle of the current South Bay market, and everything seems to happen with minimum drama. So there is little surprise at the minimalist 19% decline in monthly sales volume, the lowest of the South Bay. Likewise there is no shock the Inland cities came in with the lowest monthly price decline, a mere 1% below June.

Similarly, the annual sales volume showed July of 2023 only 14% below last July and the median price just 1% below the same month a year ago.

Year to date for the first seven months of 2023 compared to 2022 looks much the same. The number of homes sold dropped by 22%, 799 in 2023 versus 1021 last year. The median price fell 2% to $868K from $883K. Looking back to the 2019 sales volume for the same time period, the Inland area is off by 18% for the current year. Much like the rest of the South Bay, the median price in 2023 ($868K) remains above that of 2019 ($662K) by 31%.

Home values have been increasing across the board in the US, and the percentage of homes valued at over $1 million seemed poised to hit a record in June of 2023, when the share reached 8.2%. That record wasn’t quite hit, as it actually belongs to the value of 8.6% in June of 2022.

The total value of the US housing market did hit an all-time record in June of 2023. The total was $46.8 trillion. For comparison, in June of 2022 — when the largest percentage were over $1 million — the total value was $46.6 trillion. This isn’t much lower, but it does show that either the top end is increasing in value, bringing the total value up, or there are more homes on the low end, bringing the share over $1 million down. Both of these are possibilities, since inventory is still low despite an increase in affordable living construction.

After the pandemic hit, once lockdowns were over, many people took the opportunity to move to a cheaper neighborhood. It seems like a financially sound decision. But that may or may not be the case. A large percentage of such migrants found it didn’t work out for them, and moved back. So what went wrong?

One near universal quality of cheaper areas is that they also have lower wages and less opportunity for economic advancement. Of course, in the post-pandemic era, many people were working from home, so this wasn’t drastically felt. Now that a fair share of them have transitioned back to full-time on-site work, the math just wasn’t working out. They either needed to commute longer — with gas prices being rather high — or look for a job in their new home. And it was difficult to find one. It’s also worth considering why it’s a cheap area. Is it a nearby low income neighborhood that suddenly has an influx of people? In that case, it may be about to get more expensive to live there. Is it an undesirable area? It’s probably undesirable for you as well.

It’s also important not to overlook quality of life. Cheaper neighborhoods will also have lower tax revenue, which in turn means fewer public services. The roads could be worse and there could be less public transportation. You may not have good schools nearby. The available health care is often also of lower quality. And no matter where you’re moving, you’re going to need to reestablish your social network. People frequently report feeling lonely or isolated in new areas, even when surrounded by people, because they simply don’t know anyone.

For quite a while, most buyers have been Millennials. This is predominately related to their age. The age range for the Millennial generation varies depending who you ask, but the National Association of Realtors (NAR) uses 24 to 42. This is considered to be the prime age range for first-time homebuyers as well as those moving from their starter home to their first permanent home. Because of this, Millennials have been the largest contingent of homebuyers. That’s no longer the case.

So who’s replacing them? One might expect it to be the generation just below them — it would make sense that as time goes on the younger generations fill the shoes of those before them. But the typical homebuyer has been around age 36, which is in the Millennial range, and much of Generation Z is still too young to own a home. It’s actually Baby Boomers making a comeback. The reason for this is economic, rather than generational. The current market is not well suited to homebuying. Those who are able to buy are generally those who can afford high-end homes. And one of the best ways to afford high-end homes is by having many more years of saving and building equity. Many Baby Boomers will have paid off their mortgage by now, and their homes would also be worth significantly more than they were when they were purchased. Half of Baby Boomers purchasing now are paying cash, something that Millennials without any equity are priced out of attempting.

Representative Maxine Waters recently introduced the Downpayment Toward Equity Act of 2023, intended to help disadvantaged groups afford their first home. The bill would provide financial assistance for down payments, closing costs, and the costs to reduce interest rates for first-generation homebuyers who have not bought a home within the past three years. This mainly affects Black and Latine communities and could benefit up to around 5 million prospective homebuyers. However, while probably good-intentioned, this effort is not without its flaws.

We’re currently coming out of a historic peak in home prices. Prices have started to fall now, but they’re not going to suddenly bottom out overnight. It’s going to take a while for home values to fall. Pushing homeownership aid now is not the right time, for anyone, even if it’s directed at helping disadvantaged groups. And the last time minorities experienced a surge in homeownership turned out terrible for them in the end, albeit under different circumstances. In that case, it was predatory subprime lending that left minorities on the hook for massive mortgages with negative equity after the subsequent economic collapse. Of course, it’s doubtful that Waters’ intentions are predatory, but her plan could perhaps be better timed around the state of the economy.

The skyrocketing home prices affected homes across the spectrum of affordability. The luxury home market didn’t take as much of a hit in terms of sales, since wealthy buyers can generally afford to buy even with prices being high. But that doesn’t mean their prices didn’t increase. Nationwide, the median sale price of luxury class homes rose to $1.2 million this year, which is a 4.6% increase from last year. This is actually over three times the percentage increase for non-luxury homes, which increased 1.5% to $340,000. Both of these are record median prices. However, prices aren’t increasing everywhere.

Four major cities across the West Coast experienced double-digit percentage drops in median luxury home value from last year to now. The largest decrease was in San Francisco, where it dropped 12.7% to $4.8 million. The other three were Seattle, Oakland, and San Jose. Seattle’s luxury prices dropped 12.3% to $2.5 million. In Oakland, they decreased 11.1% to $2.8 million. San Jose’s decreased 10.3% to $4.3 million. Besides very high prices despite rapidly declining prices, these four cities also share something else in common. All four of them are major West Coast hubs for the tech industry. The tech industry has recently been hit by layoffs and stock market declines, so this is perhaps not unexpected.

The current housing market is in an interesting position. Mortgage interest rates are high, but home prices are starting to cool off. It raises the question of whether it’s a good time to buy. The advantage of buying now is that home prices, while expected to continue to drop, are the lowest they’ve been in quite a while. That means you may be able to get a home at a decent price without heavy competition, and start to build equity. The disadvantage is that you’re locking in a high interest rate.

That’s where refinancing comes in. While the price of a house can’t be renegotiated once the sale is finalized, your interest rate can. This is why buying with a high interest rate can be appealing if other conditions are favorable. But this is risky, because you never truly know how long rates will remain high. It could take a long time for interest rates to drop, and it’s even possible that by that time, home prices will also be lower. In this situation, not only did you essentially overpay for your home, but you’ve been stuck with a high interest rate for longer than anticipated. It’s also worth noting that if the current interest rates scare you enough to already be thinking of refinancing in the future before you’ve even bought the home, there’s a good chance it’s because you can’t truly comfortably afford the payments for any considerable length of time.

So should you consider buying now and refinancing later? What it ultimately comes down to is that it’s a risky time to buy, and it’s not entirely clear whether it’s worth the risk even if it pays off. What is clear is that if you can’t afford to task risks, you definitely shouldn’t. But if you can comfortably wait as long as you need to, it simply boils down to real estate as a long-term investment. In that case, it’s actually one of the lower risk types of investments, but that doesn’t negate the fact that the risk is higher than usual in the current climate. The actual answer will depend on the individual and on the future, but likely answers are either “no” or “probably not.” What are some alternatives, then? Waiting for mortgage rates to drop, or even just waiting for home prices to drop more, since that can’t be renegotiated. In the meantime, you can also consider upgrading your current home to increase its sale value for when you do buy.

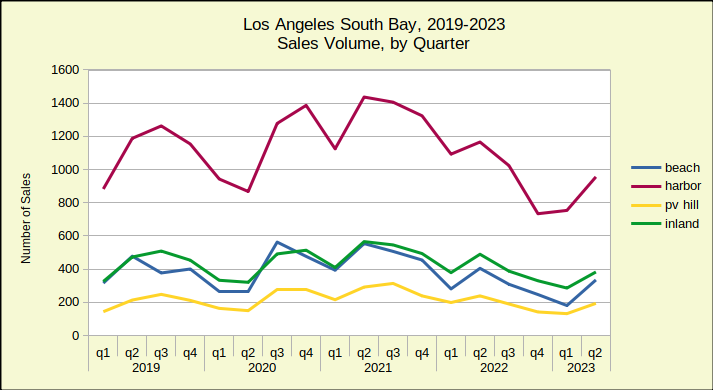

The number of homes sold in the Los Angeles South Bay during the first six months of 2023 is the lowest sales volume for a first half in the past five years. Fewer homes have been sold since the new year than sold during the same period of the worst year of the pandemic.

The first half of 2023 has ended with 24% fewer sales than the same period in 2022, which was itself down 15% from 2021. The peak of the market was early 2021, when interest rates were among the lowest in history, exploding the number of potential buyers. The lowest sales volume was during 2020 when 3311 homes were sold, which was still greater than the 3221 sold the beginning of this year.

Median Price Begins Downturn

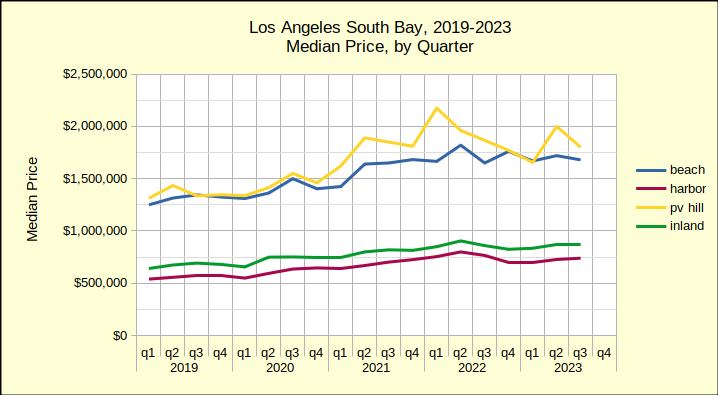

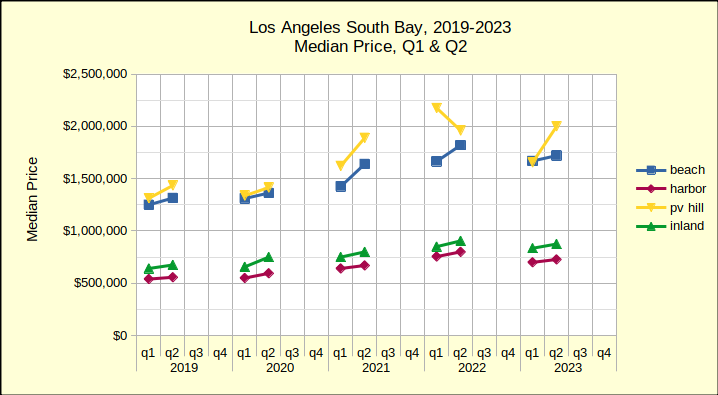

Coming right on the heels of the sales volume collapse is a drop in the median price. Prices today are down from where they were in 2022, which was the peak of the recent market. The chart below reflects the median price for the first and second quarters of the past five years. Typically, the first quarter is the slowest, with the number of sales increasing through the second quarter and then slowing again for the third and fourth quarters. Here the growth from Q1 to Q2 shows and we can see the change from year to year.

As always, bear in mind that the Palos Verdes Hill offers a comparatively small sample size, so a couple of significant sales can shift the plot lines dramatically on a chart. The chart above shows one such anomaly where PV the median price actually declines in the second quarter.

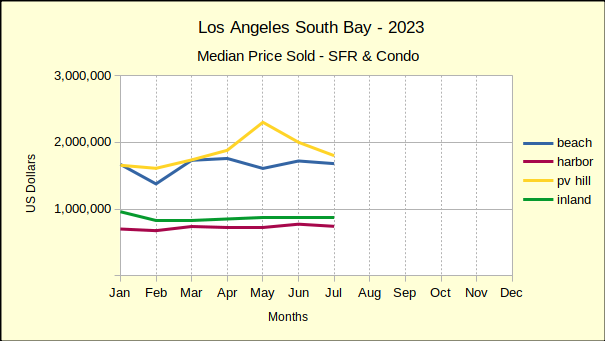

Looking across the years from 2019 all four areas show the same upward movement in median price until the second quarter of 2022. Then, comparing it to the second quarter of 2023, we can see the trend shifting downward. For example, the Beach Cities median fell from $1.82M in the second quarter of 2022 to $1.72M in the second quarter of 2023. The weakness in median prices is driven by increasingly steeper mortgage interest rates. Barring a change in market dynamics, anticipate this line turning into a steeper downslope for residential prices starting in winter of 2023/24.

When Is the Bottom?

The market is clearly taking a downward turn. Sales volume is off, median prices are turning down. Sellers are not putting properties on the market. Buyers aren’t buying. The few forecasters willing to make a guess this early are saying real estate won’t come back until 2025, possibly 2026. For those who are “waiting for the bottom of the market,” remember that by the time you read it in the headlines—you’re too late—the bottom is gone.

Beach Cities Sales Dropping Fast

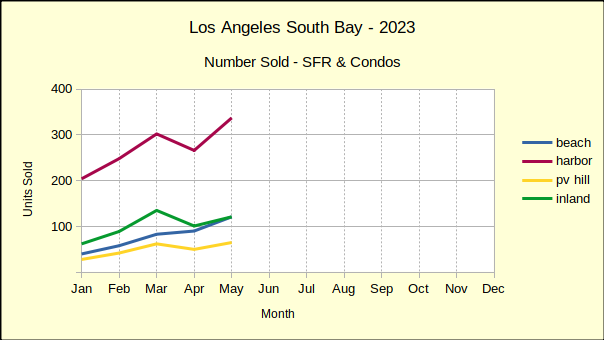

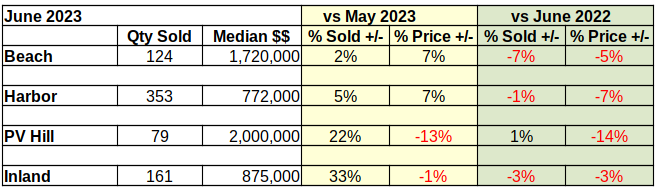

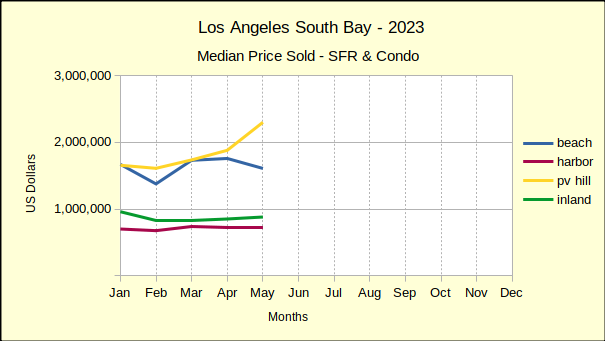

Median prices at the Beach have fallen 5% from last June, coming in this year at $1.72M, an even $100,000 below June of 2022. Year to year sales for June are down 7% from last year, at 124 units compared to 133 in June of 2022.

Month over month statistics have been highly volatile since the beginnning of 2023. Interest rates and prices have changed erratically, making short term forecasts nearly impossible. Month to month sales volume has bounced in a range from 2% to 45%. In just six months, monthly median prices in the Beach Cities have ranged between -18% and 26%.

Year to date sales volume at the Beach is down 25% from last year and is off a full 35% from 2019.

The year to date median is down 3% compared to 2022, though it is still 32% above the median in 2019.

Despite market conditions, homes in the Beach Cities remain highly desirable. For June, 78% of sales transactions closed within 30 days of listing and sold for 2.61 % above asking price. Beach homes also offer a great deal of diversity. June sales showed a 19 million dollar range between the low sale at just over $500K and the high sale at $19.5M.

Harbor Area Home Sales and Prices Down

Year to year-same month sales in the Harbor area have been negative since the first of the year. Prices were still holding up in June of last year, but sales volume had been dropping through all of May and June. As a result, the number of homes sold dropped a mere 1% coming into June of 2023. That looks good until compared with the year to date decline of 24%.

Market conditions in the Harbor last year gradually changed from joy for rock bottom interest rates at the beginning of the year to caution as sales tapered off and sales figures stated taking a hit. Median prices for June of the current year have fallen 7% from the June 2022 median of $830K.

Until now, the Harbor area has shown mixed results in the month over month statistics. For June compared to May sales volume was up by 5% (353 versus 337), while median price was up 7% ($772K versus $720K). Like the Beach Cities, the Harbor Area is following a more normal upward swing from the winter doldrums into the spring selling season.

That upward swing is not expected to go very high or last very long. At 1710 homes sold, year to date sales volume from January through June is down 24% versus 2259 sold in 2022. Sales volume is likewise down 17% from 2071 during the same six months in 2019. The variance in monthly sales is expected to drop into the single digits starting in July.

Median prices are down 4% compared to 2022 though still up 33% versus 2019. (Note: Using The Federal Reserve’s “target inflation rate”of 2% annually would have put the Harbor area median price increase at a little over 8%. That implies an “excess growth” of about 25% in median price during the pandemic buying splurge. Much of that difference, if not all of it, is expected to disappear over the next 18 to 24 months.)

June sales detail shows 77% of sales closing escrow within 30 days. Buyers were still bidding up, with the sales price exceeding the list price by 2.61%. The highest sale recorded in June for the Harbor was $4.25M; while the lowest was $527.5K.

PV Peninsula Volume and Prices Mixed

Palos Verdes, contrasting May versus June of 2023 shows a 22% increase in the number of homes sold for a monthly total of 79. At the same time, the median price dropped by 13%, falling to $2M even. Expectations for month over month statistics include fewer sales and more aggressive price reductions as 2023 wears on. The summer and fall months are projected to have weaker home sales, both in volume and pricing, as interest rates increase and buyers and sellers who “must move” run out of options.

Year over year same month sales, showed a volume growth of 1% (one sale), accompanied by a 14% drop in median price from $2.3M. That 1% increase is the first time in 2023 that any of the areas has shown positive growth in the number of homes sold. As such, and knowing that the PV Hill is considerably smaller that the other areas we measure, readers are cautioned about the wide swings in PV statistics.

Sales volume for the first six months of 2023 is down 26% compared to 2022 (326 homes in 2023 versus 438 in 2022. Similarly, sales are down 9% from 2019 when sales of 358 homes were recorded. Median prices of $1.8M for the same period are down 13% from 2022 prices of $2.1M and up 36% from $1.3M in 2019.

Market time has remained good, with 75% of sales closing withing 30 days. Sellers have enjoyed selling prices 2.3% higher than asking prices, a trend expected to disappear before the end of summer. Once again showing the range of homes available in the South Bay, the high sale in PV was $10M while the low was $610K.

Inland Area Makes Strong Showing

Sales volume of 161 homes in the Inland Area for June was up 33% over sales of 121 in May. With 33% more activity came a 1% reduction in median price, which fell to $875K after reaching $880K in May.

Comparing June of this year to June of last year showed a volume decrease of 3% from 166 in 2022. Likewise, this June showed a median price decrease of 3% from last year’s $905K.

Year to date volume for the first six months was down 68%, for 669 units sold, versus 869 in 2022. Going back to 2019, the most recent “normal business year,” sales volume was down 21% from 799 sold in 2019.

Median price of Inland area homes for the same six month period showed at $863K, down 3% from $887K in 2022; and up 32% from $652K in 2019. Days on market remained under 30 for 82% of the Inland area homes sold in June. Buyers offered 2.6% above asking price. The high market sale was $2.2M while the low was $390K.

Obviously, when looking at a home appraisal, the appraiser is the expert. But appraisers are still human, and can make mistakes. Make sure to read over the appraisal report, especially if you feel the appraisal value is wrong. It’s possible the appraiser entered something incorrectly or there was a communication error.

If you review the report thoroughly, you may be able to find discrepancies even if you don’t know much about appraisals yourself. If you do, don’t be afraid to talk to the appraiser about it. Sometimes just pointing out a mistake can solve the problem. If you do need to argue your case, though, having thoroughly read the report can only benefit you. This lets you potentially gather enough evidence that the appraiser revises their appraisal.

If that doesn’t work, you may have to request a reappraisal from the lender. Though, you should note that not all lenders allow reappraisals, and even if they do, they won’t accept your request without sufficient evidence. If you can’t get a reappraisal — whether the lender doesn’t allow them or the request was denied — the next person to talk to is the other party in the transaction. Be open with them and discuss the situation so they understand why you want to renegotiate. If you’re the seller, you may need to adjust the purchase price, and if you’re the buyer, you may need to explore other financing options.

For a long time, a new homeowner’s first purchase has likely been a starter home. A starter home means that the homeowner expects to live there a short time, sell once it appreciates, then buy a larger home. People generally live in starter homes between three and seven years. That trend is going away, though, for a few different reasons.

The largest contingent of homebuyers, and also first-time homebuyers, is currently Millennials, who are between 27 and 42 years old right now. This roughly corresponds to the 25 to 44 age range homebuyer contingent used by the National Association of Realtors (NAR). NAR discovered that among those in this contingent who bought a home last year, 40% planned to live in the home at least 16 years. Not only is this more than triple the average length of ownership of a first home, it’s also double the average length of homeownership overall. This value is 48% for the lowest age bracket, between 18 and 24 years old. For reference, Generation Z is currently between 11 and 26 years old.

The major reasons for this are economic. Interest rates have skyrocketed so high this year that those who have managed to find a home last year likely locked in a low interest rate. They’ll want to ride that rate as long as they can. Even those who weren’t able to find a low interest rate aren’t going to want to go through the hassle of finding a new home to purchase, as there simply aren’t very many homes available. Supply is lower than demand, and construction is still failing to meet demand, even as the construction rate inches back upward and demand has somewhat dropped off. They’re more likely to refinance once rates drop than look for a new home. Home prices are also a factor. Rising prices means needing to save up for longer, both before you buy your first home and while living there. There’s also a bit of a psychological factor here; if you need to wait a while to buy, you want it to be something worth the wait. There’s also another potential reason that economists may not notice at all, since it’s more cultural. Millennials are less likely than older generations to marry young or have children. This means they are also less likely to need a larger home. Their first purchase could look like a starter home, but it may actually be perfectly well suited to their long-term needs.

Real estate is widely considered one of the most reliable forms of investment. But that doesn’t mean you can go into it completely blind and expect profits. It’s entirely possible that even a bad real estate investment could net profits eventually, but you shouldn’t count on it. If you’ve never done any real estate investing before, make sure to do your research first. Even if you have, you need to be aware of shifting market conditions.

For those just starting out, start by gathering information. This could take some time, so don’t expect to start investing immediately. Build networks with more established investors as well as agents, property managers, and contractors. Do your own research as well, particularly by learning about the various property types, relevant laws, and financing options.

Once you know about investing in general, you can move on to researching specific properties to invest. Determine the goals of your investment. How much profit do you want? When do you need the money? What sort of risks are you willing to take? Knowing the different property types is particularly important for this step, since it allows you to better pick the right investment as well as diversify your investments. Now you can examine the market trends and see what’s available that fits your plan. If there isn’t much around, you may need to adjust your plan. When identifying properties, take into account factors such as the location, expected appreciation, rent values, and property condition.

If you’ve ever bought a home, chances are you’ve heard of a property being “in escrow.” But what does this actually mean? Escrow is the term for a neutral third party holding funds and documents to be disbursed during a real estate transaction. This is typically either an escrow officer or a title company, and even if it’s a company, the entity will be referred to as the escrow officer. The reason for this is to safeguard funds to avoid misallocation or fraud, which is why it’s important that the escrow officer is trusted by all parties involved.

The escrow process is initiated when the buyer and seller open an escrow account and deposit the funds after agreeing on the terms of the transaction. This is also when the buyer deposits their earnest money and the escrow officer collects all necessary documents, such as the purchase agreement, title documents, and loan documents, among others. Once escrow is initiated, the buyer will then have a period to investigate the property and conduct inspections. If the buyer finds any issues during this period, that’s when they can request repairs or renegotiate the agreement. Once the buyer is satisfied, the next step is to remove contingencies, after which the transaction enters the closing process. During the closing process, the escrow officer prepares closing documents and coordinates signatures. Only after the documents are signed by all parties can the funds be disbursed and title transferred to the buyer.

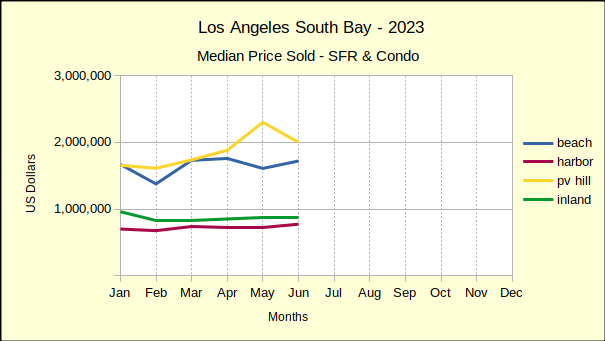

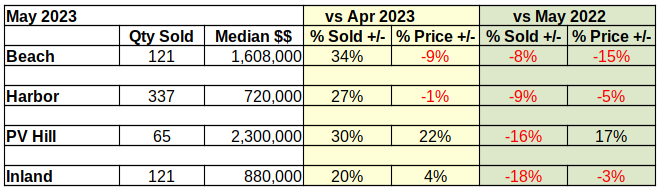

Compared to last month, South Bay home sales look very positive, except for a little tarnish in the Beach cities prices. The sales volume was up by substantial margins in all areas. Prices were mixed with a remarkable median price increase on the Hill. The only exception: After showing positive growth for the past two months, prices at the Beach took a substantial tumble in May.

Year over year activity was an entirely different story. Sales volume was down significantly from last year in all areas. Prices took a hit everywhere except on the Palos Verdes peninsula. (More about that below.) Entry level homes in the Harbor and Inland areas were impacted the least, though even a 3% drop in a single month is significant in the world of real estate.

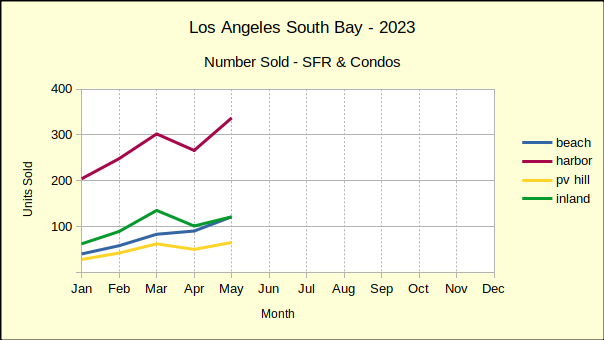

We report actual statistics rather than “seasonally adjusted”.numbers. May is traditionally the launch into buying season in the South Bay, so a May increase in volume from April is to be expected. On the other hand, a 10-20% decrease from May of last year indicates a heavily retrenching market. Every month since the beginning of this year, the number of homes sold in the South Bay has decreased in comparison to 2022.

Similarly, median prices across the South Bay have dropped from the highs of 2022. There have been scattered instances of positive change, like the 17% increase over May of last year for PV. Overall though, prices have been collapsing at an ever more steeply declining rate since January.

Much has been said about the steep rises and falls of sales volumes and median prices since the Covid pandemic hit in early 2020. That leaves 2019 as the last “normal” year of business. At the mid-year point we’ll give a more in depth comparison to 2023 to hopefully provide a more stable picture of the market. In the meantime, year to date statistics for the first five months reflect an overall decline of 23% in sales volume, and an increase of 33% in median price. The sales slowdown has most affected the Beach Cities with a drop of 39%, followed by the Inland area at 21%, the harbor at 19%, and finally the PV Hill with a 14% slip. A review of the changing median prices across that many years requires adjusting for desired inflation as opposed to uncontrolled inflation.

Beach Cities: More Sold at Lower Prices

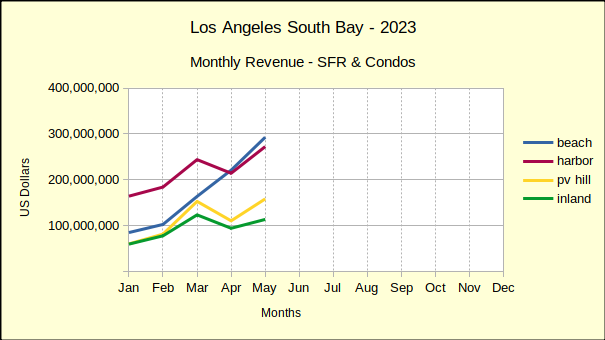

Monthly, the Beach Cities have been on a roll. Even in April, when the other three areas took a nose-dive, the Beach climbed steadily higher in both sales volume and median price. The blue line on the monthly revenue chart below shows surprisingly strong growth.

A closer look at the sales data shows some of the detail. Two of the 121 Beach area sales were on the Strand, with one selling at $18.6M and the other at over $15M. Sales in that rarefied atmosphere tend to be few and far between. In fact, one of those properties sat on the Multiple Listing Service (MLS) for almost exactly three years before it sold. With the April median price at $1.6M, the impact to the aggregate statistics becomes apparent quickly.

Market time for the Beach Cities in May was actually quite prompt, with 79% of the homes sold having spent less that 30 days on the MLS. Pricing was equally strong, with sales prices coming in at two percent above asking price. While the high sale was $18.6M on the Strand, the low was $530K at Brookside Village in Redondo Beach.

Harbor Area: Sales Up – Prices Down

As the red line in the chart below reflects, Harbor area sales entered the spring selling period with a bang! Sales volume was up 27% over April—but, remember April sales were down by 12% in the Harbor and down 13% across the South Bay. Downward pressure on prices has been showing up since the beginning of the year. Out of the first five months of 2023, month to month median prices of Harbor area homes have dropped three times. May saw a 1% decline, which was a repeat of April’s price slip.

Annual statistics cast a recessionary shadow across the picture. Looking back at May of 2022 shows the same month this year with 9% fewer sales and a drop of 5% in median price. Year to date, 2023 has lost 29% in sales volume and 5% in median price.

Compared to the first five months of 2019, the last “normal” business year, Harbor area volume was off 19%. The median price remains positive at 33% above the 2019 median. So far this year the median at the Harbor has declined an average of 5% per month. Given that rate, it’s reasonable to expect a total loss of the price gains since 2019.

Like the rest of the South Bay, the time on market for May was short as 75% of sold properties went into escrow within 30 days of listing. The low sale for the month was $269,500 and the high was $4M, a relatively high price in what is generally considered an entry level market. Interestingly, the high sale was originally listed at $9M in March of 2021, sitting on the market for two years before an accepted offer.

Palos Verdes: Home Sales & Prices Hot On The Hill

On a month to month basis, homes on the Hill came in with a 22% increase in median price, that being on top of back to back 8% increases for March and April. We’ve long said that homes on the Hill are undervalued. It looks as though that will soon be changed.

Monthly sales volume also jumped 30% for PV, though it has slowed since February and March when it was up 50% and 48% respectively. This pattern of sales increases slowing holds true for most of the South Bay. During the first quarter of 2022 the local real estate market was on fire, and then came the interest rate increases.

When the interest rates were bouncing around 5% during April and May of last year, the PV sales volume had already begun a long, slow decline. Sales figures were off by 30%-40%. So far this year, sales have continued to fall and are, in aggregate, now 31% below 2022 volumes.

Again on a year to date basis, median prices in PV are down 11%. Because the PV Hill has a comparatively small amount of homes, statistics can be volatile. June was the peak of PV business in 2022. While the summer months are typically busier and more competitive, expect this June to be less “exuberant” than May, or last June.

Like the rest of the South Bay, about 75% of homes sold on the Palos Verdes peninsula were active on the market for 30 days or less. On average, the sales price was 2.6% above the asking price.

Inland Area: Seasonal Bump In Sales and Prices

In May, the Inland area kicked off the spring selling season by pushing month to month sales volume upward 20%. While the volume of sales increased on a month to month basis, the median price went up by 4%. This seasonal bump in sales and prices contrasts sharply with the longer look of a year over year view. Comparing May numbers from last year to this year gives a reverse result. The number of homes sold in the Inland area fell 18% from May of 2022, and the median price fell 3%, dropping back to $880K from $910K last year.. The longer perspective shows a clear decline in sales accompanied by a hint of decline in median prices.

Looking at the first five months of the year shows sales volume off in total by 68%, or an average monthly decline of nearly 15%, another indicator of the slow market. It’s joined by a 1% drop in the year to date median price. On the positive side, 87% of the Inland area sales for May closed within 30 days of being listed. With business slip-sliding away, everyone involved is making the transactions happen as quickly and smoothly as possible. The high and the low sales figures for the Month were $1.7M and $310K, respectively. Sellers rejoiced at, and willing buyers paid, an average sales price of 2.9% above the asking price.

Purchasing a home is a tough decision. You’re probably going to live there around eight to ten years, on average, so you want to make sure it’s somewhere you want to live. The good thing about building new is that you can make sure the home itself is right for you. But it’s really not that simple. There are pros and cons to both buying and building.

The most obvious advantage to buying an existing home is the reduced hassle. You don’t need to oversee the design and construction, making sure everything is to your specifications. You don’t need to wait for construction to finish before moving in, and while delays are still possible, there are fewer opportunities for delays. Another is that purchasing a home may be less expensive. This depends on the area, but construction costs are still high. Moreover, existing homes have almost immediate resale value, which can mean greater equity when you go to sell it. A less apparent advantage of buying an existing home is location. You might imagine that when you’re building new, you can pick anywhere to build as well, but the fact of the matter is that there are far more existing homes than empty lots, so you don’t get as much choice of where to build unless you’re planning to bulldoze an existing home.

The primary benefit to building new is customization. Whether you’re buying or building, you should have a good idea of what you need or want in a home. By building new, you ensure that you get those things, as long as they’re within your budget and no complications occur. A new home also means fewer issues, at least once the construction is finished. Any major structural issues would be the fault of the builders and not age. The property will use the latest building technologies, which are generally safer and more energy efficient. Building new is also a safer investment, albeit not necessarily a highly profitable one. It may take longer for a newly constructed home to accrue equity, but it’s extremely unlikely to go negative by the time you sell.

There are four different types of commercial leases that each place different responsibilities on the tenant and landlord. These are known as net lease, double net lease, triple net lease, and absolute triple net lease. They can be abbreviated as N, NN, NNN, and Absolute NNN respectively. In general, N places the fewest responsibilities on the tenant and Absolute NNN places the most. However, in certain cases a tenant may prefer an NN lease over an N lease, if the tenant is adamant about not paying maintenance costs.

For each of these lease types, the tenant is responsible for their base rent plus some additional property expenses. The landlord in turn is responsible for structural issues, for all except an Absolute NNN lease, and may be responsible for some other costs. In an N lease, the additional property expenses tenant is responsible for include a portion of the property taxes, insurance, and maintenance costs. The landlord is responsible for major repairs. With an NN lease, the tenant is responsible for the entirety of the property taxes and insurance, but unlike an N lease, it’s the landlord who is responsible for maintenance costs. With an NNN lease, the landlord’s only responsibility is major structural repairs. The landlord’s only role for an Absolute NNN lease is collecting rent.

The high mortgage interest rates we’ve been experiencing have been the result of benchmark rate increases by the Federal Reserve. The benchmark rate isn’t directly tied to mortgage interest rates, but the benchmark rate does have a strong effect on interest rates. Now, though, no more rate hikes are expected, which should cause interest rates to level off, and then start to decline.

This levelling off followed by a decline is exactly what the Fed was aiming for with the rate hikes. It’s impossible for mortgage rates to drop without the real estate market, and in turn the economy as a whole, taking a hit. By raising rates above what they should be during a period of high prices, what the Fed has done is soften the blow by allowing the decline to be more gradual. Of course, this comes at the cost of significantly decreased affordability for the period of the rate hikes. Once interest rates fall below 6%, which should happen before the end of the year, the market should pick back up again. However, the effect may not be noticed until next year, as the end of the year is not generally a time of heavy market activity.