Due to the Fed increasing benchmark rates, the rates of fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs) are both continuing to increase at a rapid rate. The current average 30-year FRM rate is 6.70%, and it’s 5.96% for ARMs, as of Sept 30th.

It’s normal for FRM rates to be higher than ARM rates, but that may not be the case soon, because of the reasons for the rapidly increasing rates. The ARM rates are directly tied to the benchmark rates — as the benchmark rates increase, the ARM rates will also increase proportionally. While FRM rates are also increasing, it’s not directly because of the increasing benchmark rate. FRM rates are actually tied to bond market rates. However, since the FRM rates are already increasing much faster than bond market rates, they can’t sustainably go much higher, while ARM rates don’t have that restriction and are quickly catching up.

As a result of the Federal Reserve’s decision to increase benchmark rates, both fixed and adjustable rate mortgages have been increasing. Rates are now beginning to reach a stable point. Of course, the rates are in constant flux, but the fluctuations are starting to level out. This doesn’t mean a reversal of the recent increases; the 30-year FRM rate is levelling at somewhere around 5.5%, which is still relatively high in comparison to recent years.

What it does mean is that the uncertainty regarding rates is decreasing. With this, the popularity of ARMs will drop, as uncertainty is their primary drawback. They had experienced a surge of popularity while FRM rates were similarly unstable, since FRM rates tend to be higher than ARM rates during the same time period. This is despite the fact that ARM rates also drastically increased between July 2021 and July 2022, from 2.48% to 4.30%.

Conventional wisdom is that it’s more financially sound to buy a house than rent, if you can afford to do so. However, this may not be entirely true anymore. While house prices and rent prices are both increasing, house prices are increasing at a much higher rate. The gap between mortgage payments and rental payments increased from $25 in April 2021 to over $800 a year later. This difference is the highest in over 20 years. Unless you’re planning to live there for over thirty years, you’re probably better off renting. Importantly, this is based on a down payment of 5%, which is significantly lower than the commonly recommended 20%, but many buyers may not be able to afford a 20% down payment.

This won’t be permanent, but it could last several years. Home price growth has already started to lessen, but interest rates are high right now. Prices aren’t expected to be at a low until around 2025. Increased construction could aid in further reducing home prices. Given that we’re seeing the the beginnings of another recession, though, that probably won’t happen until a couple years after prices bottom out. Even after a return to normality, California is still going to have a lot of renters. With many lower-income workers permanently priced out of buying, the state has consistently had the first or second lowest homeownership rate of any state, frequently swapping places with New York.

When getting a mortgage loan, that money generally comes from a bank. But it’s important to realize that a bank isn’t just an impersonal repository of money. Banks are businesses, and as such, they’re always looking for profit. This extends to deciding your interest rate, which is nearly always not the best rate you could get.

One of the ways banks pull a profit is by looking to the future of interest rates. They will frequently take an expected future average rate rather than the current average rate if they expect rates will rise soon. They get slightly ahead of the game this way. The other reason rates are often higher is not entirely within the bank’s control, although it is partially a result of their actions. A common method of reducing risk is for a bank to sell debt to an investor. This also frees up capital for the bank. But it introduces an additional party also looking for a profit, and the bank may need to make concessions for the deal to go through. Increasing interest rates is a way to recoup these losses.

Commercial real estate has been struggling in recent years, just as many other sectors of the economy have been struggling. However, one advantage that most commercial buyers have over residential buyers is that they’re more willing to take on debt because their living expenses are likely a lower percentage of their income. As a result, loan originations for commercial properties increased dramatically in the first quarter of 2022.

As can be expected, the effect is greatest in the areas either least affected or most in demand as a result of the 2020 recession. These include hotels, industrial, retail, and healthcare. Loan originations for hotels increased a whopping 359% from 2021. Mortgages for the industrial sector also increased over 100%, by 145%. Increases in retail and healthcare were also significant at 88% and 81% respectively. Lesser increases were noted for multi-family dwellings at 57% and offices at 30%, but these still increased, not decreased. However, one should note that the available data isn’t entirely up to date. Mortgage rates have increased significantly since Q1, so despite the fact that they’re starting to slip back down just now, there may have already been a downward trend in commercial loan originations that we haven’t noticed yet.

Primarily as a result of actions by the Federal Reserve, mortgage rates have been trending upward since January. The rates peaked in June, and have now begun their decline in July. ARM rates are currently more volatile than FRM rates, and may continue to flip-flop, but they are still lower than FRM rates.

The 30-year FRM rate peaked at around 5.7% in late June. It’s since dropped slightly to 5.3% as of the first week of July. The 15-year fixed rate followed a very similar trend line, albeit at a lower peak rate of just under 5%. This is normal; the 15-year rate has always trended lower than the 30-year rate. The ARM rate was 4.34% at its highest in June, and has now dipped below 4%.

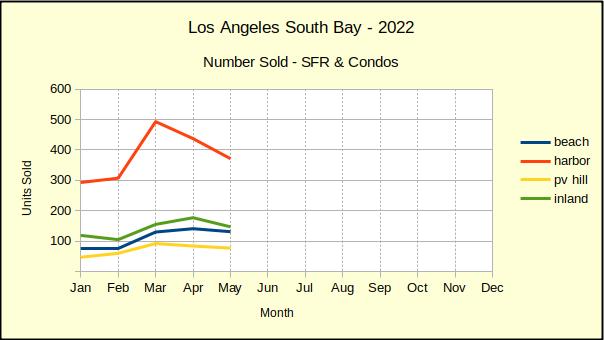

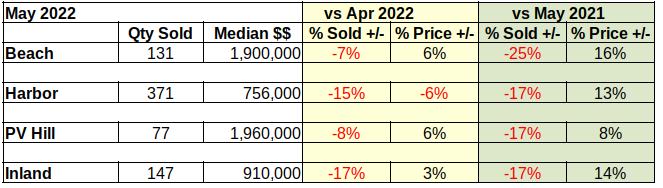

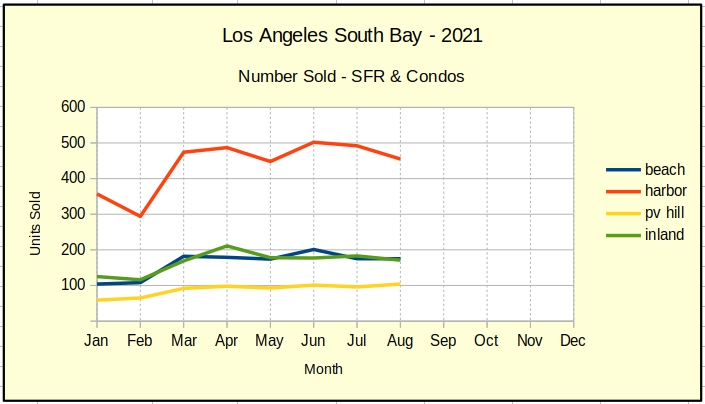

The number of homes sold in the South Bay has declined from last month, and has declined from last year. The quantities are actually rather dramatic given that May is typically a time of increasing sales. The drops range from -7% to -17% lower than April sales of this year, and from -17% to -25% below May of last year.

With over half the year remaining, mortgage interest rates have doubled, currently sitting around 6%. The hike in interest rates has so far reduced the average buying power by about -25%. Coupled with home price increases estimated to have risen 38% since the start of the pandemic, the immediate future of real estate looks dismal.

Inflated consumer prices are also blocking potential home buyers as the Consumer Price Index (CPI) climbs toward a 10% annual hike. There’s little chance of saving for a down payment when the price of everything on the shopping list is going up..

Retirement accounts are often a source of down payment funds. As of this writing the major stock market indices are all down: Dow Jones Industrial Average, -16%; S&P 500, -22%; Nasdaq Composite, -31%. Forecasts are growing for a Fed-induced recession that may begin as soon as this fall. Some potential buyers may see borrowing from their retirement fund to purchase a property as a means to preserve the capital during a recession. Others may not be in a position to do that.

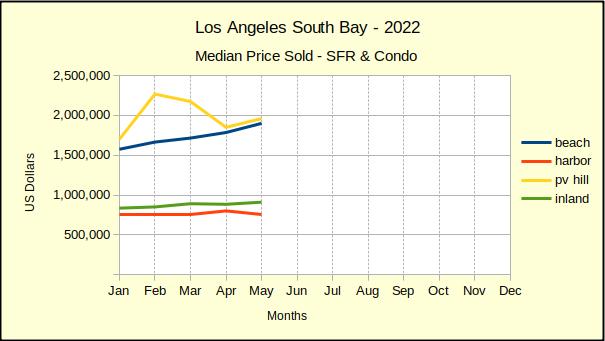

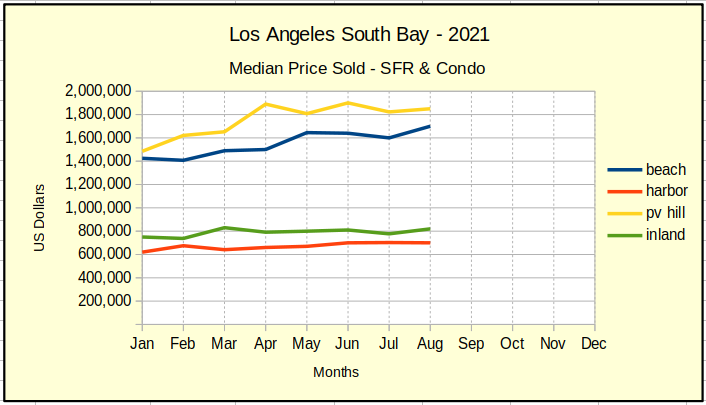

Median Price Sold

May prices delivered a mixed message. The Palos Verdes Peninsula, which had seen two months of decline from a temporarily high median price, headed back up again. The Beach cities continued a steady climb, and the Inland area showed a modest price increase after having dropped 1% in April.

However, the Harbor area, which is as large as the other three areas combined, took a -6% hit to prices. We anticipate the Harbor and Inland areas, which comprise the bulk of the traditional middle class family homes in South Bay, to be the first to react to the economic stress.

Typically, the recession cycle starts with a slowing of sales. As properties languish on the market, sellers begin to reduce prices. One after another, median sales prices will drop until the price reduction offsets the impact to buyers. At that point, buyers will begin to support the reduced purchase prices and we can see growth in the market.

Experts differ in their estimates of how long this cycle will take, and when we can expect the market bottom. There are some predicting a rapid fall based on the speed with which the Federal Reserve Bank (Fed) is reacting. The June meeting of the Fed ended with a .75% hike in the prime rate, and a promise to raise it at least another .75% before the end of the year. While that could slow the economy as early as the beginning of 2023, more conservative minds suggest the end of 2023 for a turn-around.

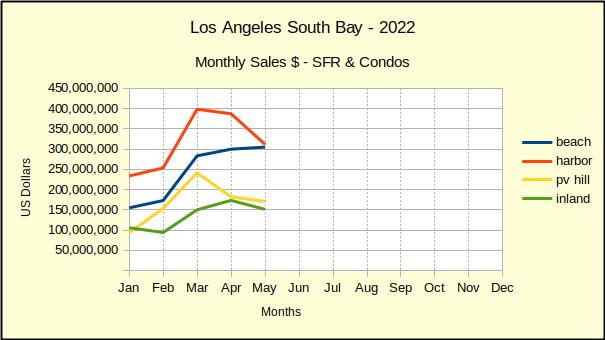

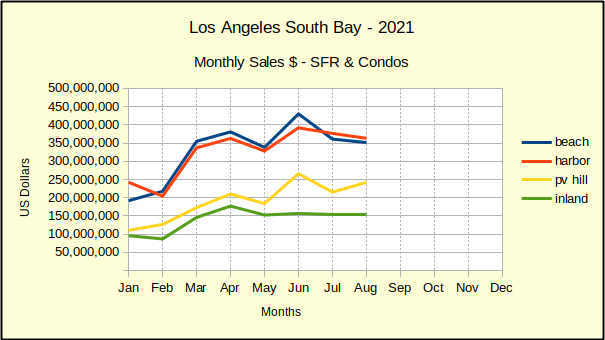

Area Sales Dollars

The total sales dollars tell the truest story. While sales are slowing and median prices are beginning to slow, the combination shows up here.

Everywhere except the Beach is showing reductions in total sales on a month to month basis, and on a year over year basis. The declines are small to date, with year over year ranging from -1% to -10% in May. Month to month changes ranged from +2% at the Beach to -19% in the Harbor area.

These early numbers follow the general pattern we’ve seen in recent recessions, whereby entry level homes are the first impacted and the last to recover. We anticipate the Harbor area to lead the charge down, followed by the Inland area. Recent years have shown the Beach to be the strongest growth area, so we expect the recession to hit there last, following declines on the Hill.

The nature of the impending recession is still uncertain. Some pundits are saying that at least initially we should expect “stagflation,” that odd environment we first encountered back in the 1990s when prices of everything continued to climb, along with job layoffs and massive unemployment. Other forecasters suggest that because the international economy is roiling with continuing high tariffs (courtesy of the last administration) and new monetary sanctions daily (courtesy of the current administration), this particular recession may last much longer than normal.

In Summary

As the table below shows, the majority of the negative impact for May happened in the quantity of housing units sold. With one exception, prices continued to escalate. We believe this is temporary and likely to change before the end of the year. The -6% drop in median price at the Harbor presages the direction of home pricing as inventory grows and listings stagnate.

Approximately 3 out of 4 listings coming across our desk recently have been either Price Reduction or Back On Market. That means property is staying on the market longer. The Average Days On Market (DOM) for May ranged from 10 days on the PV Hill to 14 days in the Harbor area. As recently as this winter we were still seeing multiple offers on the first day the property was available.

Another measure of the market condition is how far the average sales price declines in the first 30 days on market. We did a quick look for May and came up with these statistics. Thirty days after the original listing, the price had dropped from the original: at the Beach, -9%; the Harbor -6%; PV Hill -18%; Inland -5%. As of May, we’re also seeing property that has been on the market for several months, with several price reductions.

Notable Properties

The high and low sales for May were not terribly dramatic. A Manhattan Hill section home and a downtown Long Beach condominium. Thay are simply very big, and very small.

High Sale

Located at 812 5th St, this Manhattan Beach hill section home was originally listed at $10.5M and sold for $8,980,000 after 34 days active on the market. The home offers six bedrooms and seven full bathrooms in 5576 sq ft. Amenities included ocean view, pool, spa, custom waterfall & fire features, a full basement with recreation/media room, home theater, storage, a temperature-controlled wine cellar, and private guest quarters.

Low Sale

Measuring barely 381 sq ft, the studio condo at 819 E 4th St #25 sold for $215,000 in one day. Located in the vibrant East Village of Downtown Long Beach this tiny home offers a remodelled kitchen and bathroom. The unit sits on the second floor, overlooking the intersection of 4th and Alimitos and within walking distance of many downtown shops, clubs and eateries.

The California Housing Finance Agency (CalHFA) has introduced a new loan program called the Forgivable Equity Builder Loan. It comes with some heavy restrictions — only first-time homebuyers are eligible, and it only covers up to 10% of the purchase price. This is because it’s a supplementary loan that can only be taken out in combination with a CalFHA first mortgage. The good news is that this loan has an interest rate of zero percent, and is also forgivable if you occupy the residence continually for five years. However, standard interest rates apply to the CalFHA first mortgage.

The program also requires borrowers to complete a course on homebuyer education and obtain a certificate of completion. This course does require a one-time fee of $99 if taken online, or a variable-rate fee if taken in person. You must also occupy the new home as your primary residence, as well as meet income requirements. The property must be a single-family residence or manufactured home. This can include condominiums if they meet the requirements for the CalFHA first mortgage, or ADUs in some cases.

After a period of low mortgage rates, they’re going back up quickly. That is the expected effect of current Fed policy, but we may hit 5% faster than expected, possibly as early as next month. As of the beginning of April, the average 30-year fixed rate was 4.59%. If they do hit 5%, it would be highest rate in the past decade, though they did get close in November of 2018 at 4.94%.

The increasing rates are definitely going to slow down the real estate market. That may be a good thing for the market, given how hot it’s been, but it’s definitely not good for buyers. Demand isn’t going to disappear completely, though. And the effect is probably mostly psychological. Historically speaking, 5% isn’t a particularly high rate. It’s just that rates have been trending downward for quite some time, so it isn’t going to be familiar territory for the new generations of buyers.

There are two main reasons to refinance your home. One is to reduce your monthly payments in order to free up cash, and the other is to pay off the loan more quickly. But refinancing doesn’t just simply do this automatically; you have to choose a new mortgage with terms that work for you. Figure out what your goal is and pick the right mortgage.

Reducing your interest rate is the surest way to free up cash, but it can also simply be used to pay off the loan faster. With a lower interest rate, a greater percentage of the principal is reduced each time you make a payment. However, this only works if you can qualify for a lower interest rate. If you don’t qualify normally, consider reducing the length of the mortgage. This will probably result in higher monthly payments, but will also likely allow you to qualify for a lower rate, and almost certainly allow you to pay off the mortgage faster as long as you make the payments. If you have plenty of cash on hand and just want to save money in the long run, consider replacing your mortgage with one that allows you to make larger payments on your principal. This is more costly in the short term, but would allow you to pay off the loan early and thus spend less on interest, reducing the overall cost.

Many people are blindsided by rising mortgage rates after getting a preapproval, thinking that the preapproval has locked their rate. It hasn’t. The first opportunity to lock your mortgage rate happens when your final loan application is approved, though you don’t even have to lock it until shortly before closing on a purchase, if you think rates will go down. In addition, the lock period is not indefinite. It usually lasts anywhere from 15 to 60 days, and it could definitely take longer than that to find a home.

There are ways to mitigate the issues presented by shifting mortgage rates. Rates don’t tend to change much during a typical closing period, but you want to lock early when rates are rising and late when rates are falling. Consider budgeting for a loan lower than your preapproved amount in order to account for fluctuations in mortgage rates. Different lenders also have different locking policies. Make sure to shop around and ask about lock periods, renewing options for locked rates, and the possibility of locking out rising rates but not falling rates.

The most commonly used benchmark rate to determine mortgage rates has long been the LIBOR, or London Inter-Bank Offered Rate. However, this has some issues. The LIBOR is not tied to actual transactions. Because of this, bankers that have influence on the LIBOR can simply manipulate the rate to their benefit. This occurred in the 2008 recession, where the LIBOR was kept artificially low to encourage people to borrow money. The financial world has finally decided LIBOR won’t cut it as a benchmark, and it’s being phased out.

Financial institutions won’t be forced to stop using the LIBOR, but if they do use it, they will be required to include at least one rate that isn’t LIBOR-based as a backup. They will have until the end of 2021 to comply. The front runner for a backup rate in the US is the SOFR, or Secured Overnight Financing Rate. This rate is administered by the New York Fed. It’s not subject to the same manipulation that LIBOR is because it does take into account actual completed transactions. Fannie Mae and Freddie Mac already swapped from LIBOR to SOFR in 2020.

Back in 2019 the first eight months of the year saw 5,706 homes sold. During the same period in 2020, in the early response to Covid-19, sales dropped off by 12% to 5,003. As the market came out of the Covid doldrums in 2021, sales took a dramatic 57% jump. It’s most easily seen looking at the sales volume for the Harbor area in March on the chart below.

Part of that jump was the approximately 700 sales which didn’t happen in 2020. We don’t know how many of those “deferred” transactions have jumped back into the market. As of August the South Bay sales were at 6845, a 20% increase over the 2019 sales for this point in the year.

Seeing that a huge part of the March increase came in Harbor home sales tells part of the tale. The biggest piece of that market in recent months has been entry level or first time home buyers. Closely following are investors in small income properties.

Stories from the street imply that the growth in ADU additions and conversions has had an out size impact on that market as well. Both homeowners and landlords benefit from having additional living spaces.

For right now, the pandemic appears to be fading, which would tend to boost sales. Similarly, the low mortgage interest rates continue to support the market. At the same time we’re moving into fall and winter, when sales typically slow. August showed just a hint of a seasonal downward movement. September should be a directional indicator.

Sales Prices Up

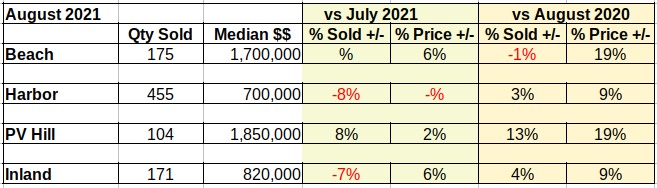

That jump in sales volume was accompanied by a bigger jump in the median price of the homes selling. Pent up demand and low interest rates combined to create bidding wars and drive median prices up. As of the end of August, the median price of a home at the Beach was $1.7M. That number was $1.5M in 2019 and $1.4M in 2020.

Median prices on Palos Verdes trended about the same at roughly $100K more per unit.The Inland cities and the Harbor area both showed mosest increases in the $50K neighborhood.

Area Sales Dollars Slowing

The monthly sales value of homes sold across the Los Angeles South Bay for August declined in all areas except the Palos Verdes Peninsula.

Compared to July, the number of sales on the Hill increased 8% in August, with a 2% increase in median price. That translated into a $150M increase in monthly sales since the first of the year.

Activity in the Inland cities has been stable for three months already, having risen about $50K per month since the first of January.

Monthly sales at the Beach and in the Harbor area pulled back for a second month in succession. Looking at the blue line for the Beach, we see a sharp drop in July which softened considerably in August. The Harbor area shows a steady decline over the same period.

As of August monthly sales totaled ~$150M higher than the beginning of the year at the Beach. During the same period monthly sales totals were up ~100M. As we move into the fall and winter season these numbers should slow somewhat.

Statistics – by Month, by Year

Interestingly, the number of homes sold in the Beach cities was unchanged from July, while the median price increased 6% at the same time.

There were 175 homes sold in both months. So how did Beach homes grow from a median price of $1.6M to a median price of $1.7M in one month? In July, 27 of those properties sold below $1M. In August, only 20 sales closed escrow for under $1M. The entire market simply moved up, pushing the median price up $100K in one month.

On a month to month basis, prices are holding or increasing across the board. At the same time we’re seeing slowing or flat sales everwhere but Palos Verdes. Continued slowing for the season is to be expected.

There’s still a lot of buyer traffic at open houses, but sales volume is slowing and buyers are showing price resistance. There’s also some chatter out there about what’s beginning to look like inflation in the real estate market. My crystal ball is showing a slow steady ride through the next month. It’s all cloudy after that.

While mortgage rates are certainly not high, we can no longer safely call them low. The average rate for a 30-year fixed conforming loan is considered low when it’s below 3%. They’ve been slowly increasing. In the first half of August, it barely qualified at 2.99%. Now, the number sits at 3.06%.

As a result of increasing mortgage rates, demand for refinances has also decreased, dropping by 5% as soon as the rate passed 3%. Applications for purchase loans are less sensitive than refinance applications, and dropped only 1%. Despite the decreases in number of mortgage applications, the total dollar volume is still high, as a result of high prices fueled by heavy competition.

2020 saw a large increase in mortgage originations, particularly refinances, as a result of low interest rates. It was expected that this would start to fall off in 2021, since interest rates are starting to go back up. However, they’re still low enough that refinances continue to be common. The statistics are a bit misleading for purchases, though. Low inventory is boosting home prices, accounting for a significant part of the increase in loan origination dollar amount even beyond increasing the number of loans originated.

Something is still missing, though. Even though much fewer loans are delinquent now than in 2020, the share of them that are over 90 days delinquent is increasing. This is because people continue to tread water through moratoriums, but aren’t earning any money. Jobs still haven’t recovered from 2020. Foreclosure moratoriums and forbearance programs are going to end eventually, and that’s going to be a problem for some people who have lost their jobs during the pandemic and haven’t been able to find work yet. If home prices continue to rise without an actual jobs solution, these stopgap measures are going to be the proverbial dam that causes the market to crash when it breaks.

The FHA has its origins in the Great Depression, as a method for people down on their luck to secure a loan without much upfront cost. Given the current recession’s similar circumstances, it may be expected that FHA loans would increase in popularity around this time. That isn’t the case at all, because now there’s competition. FHFA loans — those backed by Fannie Mae or Freddie Mac — are currently a better deal.

The normally low upfront cost of FHA loans is countered by the fact that they have mortgage insurance premiums (MIPs), part of which is an upfront cost. This means that you are spending more over the life of the loan than with a conventional loan even with an equal interest rate. This MIP can be cancelled after 11 years if the down payment was at least 10%. However, the appeal of an FHA loan was the minimum down payment of only 3.5%, so this circumstance rarely came up.

But now, 3.5% isn’t even the lowest minimum down payment. FHFA loans have adopted a 3% minimum. What’s more, their upfront costs are actually lower, with no upfront mortgage premium. The MIP cancellation criteria are also different: The down payment amount and loan length don’t matter, and it can instead be cancelled whenever the home equity reaches 80%. Given that it’s rare for a house to be owned for 11 years, especially for first-time buyers who benefit the most from low down payment minimums, this flexibility is highly attractive.

I’m sure you all know that when you take out a mortgage loan, you pay back the principal plus interest over the life of the loan, in monthly payments. But it’s important to understand that monthly payments are not simply the principal plus interest divided by the total length in months. Because the amortization schedule ensures that each monthly payment is the same amount, it may appear as though each payment is identical. However, this is not the case.

Amortization schedules determine what percentage of each monthly payment is principal and what percentage is interest. When you first get a loan, nearly the entirety of your monthly payments are used to pay off interest, with scarcely any reduction in the principal. As you pay off more of your interest over the life of the loan, a greater percentage goes towards the principal. When you sell a home that still has a mortgage, the amount of money you receive due to equity depends on how much of the principal amount is paid off. If it’s still very early in the loan’s lifetime, you haven’t paid much of the principal, so your equity will be quite low.

When the pandemic began towards the end of the first quarter in 2020, people were understandably reluctant to start purchasing houses. As a result, mortgage applications saw a sharp decrease. However, they rebounded quickly, surpassing 2019’s numbers even while trending downwards again in December. In the week ending December 23rd, 2020, mortgage applications dropped 5% from the prior week, yet remained 26% higher than the same week in 2019. As a result of low mortgage rates, refinances shot up in 2020, increasing 4% in the aforementioned week to end 124% higher than the prior year.

So we know that more people sought new mortgages in 2020 because mortgage rates are low, but what does the recent downward trend mean for the market in the near future? Well, probably not much. While some attribute the decrease to the housing shortage and rising prices, the fact of the matter is that this has been the case for quite some time. It’s actually more likely just seasonal variation — mortgage applications already have a tendency to decrease near the holiday season. The pandemic could have some impact, but we’ve already seen that the sharp decline earlier in the year was completely mitigated by low rates increasing demand. A more telling statistic is the average loan balance, which set a record high of $376,800. This is because much of the available housing is on the higher end, pointing to a deficit of affordable housing.

The Consumer Financial Protection Bureau (CFPB) is planning to make some changes aimed at widening the accessibility of mortgage loans by allowing lenders more freedom in determining a borrower’s ability to repay. Currently, one of the requirements for a qualified mortgage (QM), the loan type preferred by both lenders and consumers, is a debt-to-income ratio of no more than 43%. This criterion is designed to be an indicator of the borrower’s ability to repay. However, there are other methods of determining this that can broaden the range of QMs. The CFPB’s solution is to compare the loan’s annual percentage rate (APR) to the average prime offer rate (APOR). Because a borrower with a high DTI would likely also have a high APR compared to APOR, DTI considerations are still indirectly included, but there will also be people with a high DTI but low risk of default that are able to get a good APR to APOR ratio and therefore successfully get a QM loan.

You may have heard the term MID in the context of purchasing a home or filing taxes. But what does this term mean? MID stands for mortgage interest deduction, and is a type of reduction in taxable income available to homeowners with a mortgage on their first or second home, or secured by their first or second home. When filing taxes, you can either take the standard deduction or itemize your expenditures. It’s common to simply take the standard deduction because many people aren’t sure how to itemize and may not even benefit from doing so. However, MID is one reason homeowners with a mortgage may want to itemize, since it is one of the itemizable deductions. The amount that the MID reduces your taxable income varies from 10% to 37% based on your homeowner’s tax bracket. It’s still possible that you would be better suited taking the standard deduction, depending on your expenditures and tax bracket.