There are many barriers to homeownership. Many of them are economic, and unfortunately no small percentage of them are the result of discrimination. But one very frequent barrier to homeownership is lack of understanding of the process. Plenty of people who can afford to buy don’t think they can, or don’t think they should, because of misconceptions about mortgages.

One myth that, despite repeated attempts by experts to clarify it, continues to plague prospective homebuyers is the 20% down payment requirement. There is actually no such requirement — it’s a suggestion. It’s a rather economically sound suggestion in many cases, but that doesn’t mean you can’t buy with a lower down payment. The reason it’s so heavily suggested is that not only does a higher down payment translate to reduced loan value and potentially a lower interest rate, but it also avoids private mortgage insurance (PMI). PMI is an additional cost that you won’t incur if your down payment is at least 20%. So a minimum of 20% down payment significantly reduces your overall monthly cost. These high monthly costs are perhaps what’s leading people to believe that renting is cheaper than buying. It can be, in the short term, but almost never is in the long term. But the reason it can be cheaper in the short term is not high mortgage costs; it’s actually the upfront cost of buying a home. Monthly rents usually go up at the same time house prices do, and are often fairly close to monthly mortgage payments. Moreover, buying a home builds equity and allows for resale, while there is no return on investment for renting. Another misperception that leads people to think they can’t get a mortgage is credit requirements. Lenders do look at your credit, but it doesn’t need to be perfect. Most people do not have perfect credit. As long as the lender believes you could reasonably pay back the mortgage, you can qualify with a credit rating as low as 500, though you may only qualify for mortgages with higher interest rates.

The misunderstanding doesn’t stop with whether or not one can qualify for a mortgage. Even once a prospective homebuyer gets to the stage of choosing a mortgage option, there is some confusion about which mortgage options are the best for you. Many people categorically refuse adjustable-rate mortgages (ARMs) and always pick the loan with the lowest interest rate. Neither of these are necessarily the right idea. Fixed-rate mortgages (FRMs) definitely offer stability and can be excellent for people who plan to keep their new home for a while or who are uncertain about their future. On the other hand, ARMs typically have a lower initial interest rate than FRMs. This means they can be more financially sound for people who don’t plan to own the home very long, or who are better positioned to take risks. A low interest rate is obviously a good thing, but it’s far from the only cost associated with getting a loan. If you need to pay PMI, that’s also a factor. But even if you don’t, there will always be closing costs, property taxes, homeowner’s insurance, and maintenance costs. Some of these depend on the price of the home, but some depend on the lender, so be sure to get a breakdown of all the costs before committing to a loan.

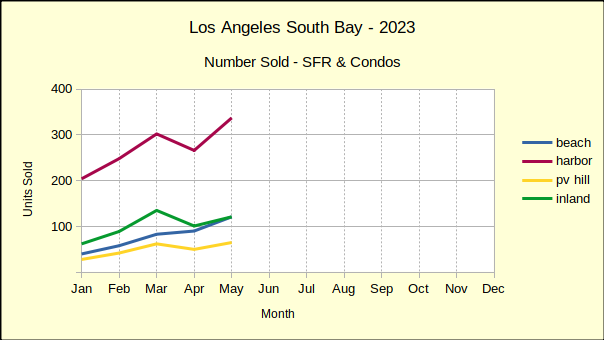

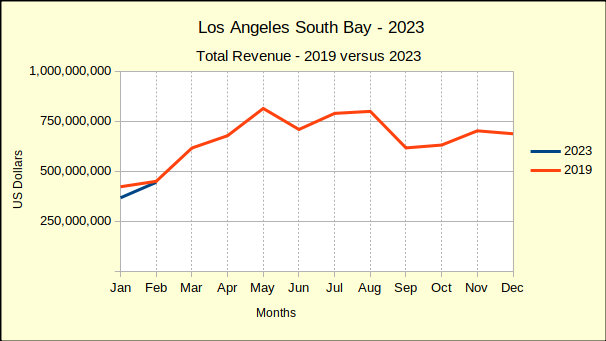

The number of homes sold in the Los Angeles South Bay during the first six months of 2023 is the lowest sales volume for a first half in the past five years. Fewer homes have been sold since the new year than sold during the same period of the worst year of the pandemic.

The first half of 2023 has ended with 24% fewer sales than the same period in 2022, which was itself down 15% from 2021. The peak of the market was early 2021, when interest rates were among the lowest in history, exploding the number of potential buyers. The lowest sales volume was during 2020 when 3311 homes were sold, which was still greater than the 3221 sold the beginning of this year.

Median Price Begins Downturn

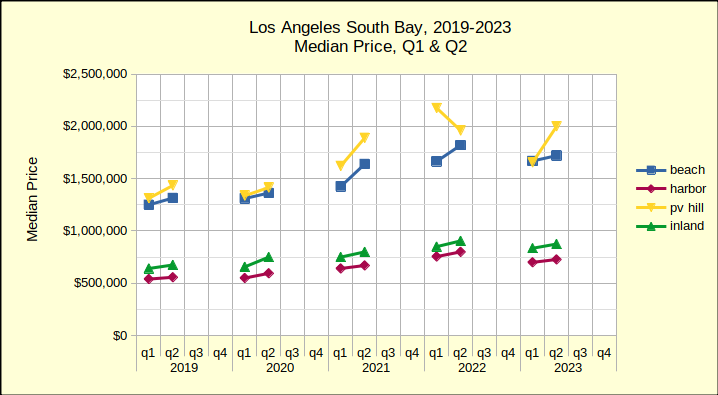

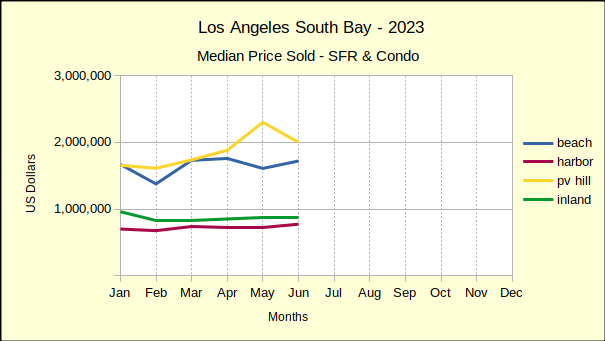

Coming right on the heels of the sales volume collapse is a drop in the median price. Prices today are down from where they were in 2022, which was the peak of the recent market. The chart below reflects the median price for the first and second quarters of the past five years. Typically, the first quarter is the slowest, with the number of sales increasing through the second quarter and then slowing again for the third and fourth quarters. Here the growth from Q1 to Q2 shows and we can see the change from year to year.

As always, bear in mind that the Palos Verdes Hill offers a comparatively small sample size, so a couple of significant sales can shift the plot lines dramatically on a chart. The chart above shows one such anomaly where PV the median price actually declines in the second quarter.

Looking across the years from 2019 all four areas show the same upward movement in median price until the second quarter of 2022. Then, comparing it to the second quarter of 2023, we can see the trend shifting downward. For example, the Beach Cities median fell from $1.82M in the second quarter of 2022 to $1.72M in the second quarter of 2023. The weakness in median prices is driven by increasingly steeper mortgage interest rates. Barring a change in market dynamics, anticipate this line turning into a steeper downslope for residential prices starting in winter of 2023/24.

When Is the Bottom?

The market is clearly taking a downward turn. Sales volume is off, median prices are turning down. Sellers are not putting properties on the market. Buyers aren’t buying. The few forecasters willing to make a guess this early are saying real estate won’t come back until 2025, possibly 2026. For those who are “waiting for the bottom of the market,” remember that by the time you read it in the headlines—you’re too late—the bottom is gone.

Beach Cities Sales Dropping Fast

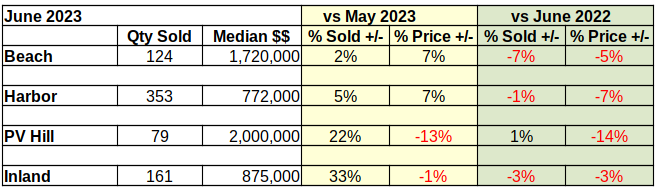

Median prices at the Beach have fallen 5% from last June, coming in this year at $1.72M, an even $100,000 below June of 2022. Year to year sales for June are down 7% from last year, at 124 units compared to 133 in June of 2022.

Month over month statistics have been highly volatile since the beginnning of 2023. Interest rates and prices have changed erratically, making short term forecasts nearly impossible. Month to month sales volume has bounced in a range from 2% to 45%. In just six months, monthly median prices in the Beach Cities have ranged between -18% and 26%.

Year to date sales volume at the Beach is down 25% from last year and is off a full 35% from 2019.

The year to date median is down 3% compared to 2022, though it is still 32% above the median in 2019.

Despite market conditions, homes in the Beach Cities remain highly desirable. For June, 78% of sales transactions closed within 30 days of listing and sold for 2.61 % above asking price. Beach homes also offer a great deal of diversity. June sales showed a 19 million dollar range between the low sale at just over $500K and the high sale at $19.5M.

Harbor Area Home Sales and Prices Down

Year to year-same month sales in the Harbor area have been negative since the first of the year. Prices were still holding up in June of last year, but sales volume had been dropping through all of May and June. As a result, the number of homes sold dropped a mere 1% coming into June of 2023. That looks good until compared with the year to date decline of 24%.

Market conditions in the Harbor last year gradually changed from joy for rock bottom interest rates at the beginning of the year to caution as sales tapered off and sales figures stated taking a hit. Median prices for June of the current year have fallen 7% from the June 2022 median of $830K.

Until now, the Harbor area has shown mixed results in the month over month statistics. For June compared to May sales volume was up by 5% (353 versus 337), while median price was up 7% ($772K versus $720K). Like the Beach Cities, the Harbor Area is following a more normal upward swing from the winter doldrums into the spring selling season.

That upward swing is not expected to go very high or last very long. At 1710 homes sold, year to date sales volume from January through June is down 24% versus 2259 sold in 2022. Sales volume is likewise down 17% from 2071 during the same six months in 2019. The variance in monthly sales is expected to drop into the single digits starting in July.

Median prices are down 4% compared to 2022 though still up 33% versus 2019. (Note: Using The Federal Reserve’s “target inflation rate”of 2% annually would have put the Harbor area median price increase at a little over 8%. That implies an “excess growth” of about 25% in median price during the pandemic buying splurge. Much of that difference, if not all of it, is expected to disappear over the next 18 to 24 months.)

June sales detail shows 77% of sales closing escrow within 30 days. Buyers were still bidding up, with the sales price exceeding the list price by 2.61%. The highest sale recorded in June for the Harbor was $4.25M; while the lowest was $527.5K.

PV Peninsula Volume and Prices Mixed

Palos Verdes, contrasting May versus June of 2023 shows a 22% increase in the number of homes sold for a monthly total of 79. At the same time, the median price dropped by 13%, falling to $2M even. Expectations for month over month statistics include fewer sales and more aggressive price reductions as 2023 wears on. The summer and fall months are projected to have weaker home sales, both in volume and pricing, as interest rates increase and buyers and sellers who “must move” run out of options.

Year over year same month sales, showed a volume growth of 1% (one sale), accompanied by a 14% drop in median price from $2.3M. That 1% increase is the first time in 2023 that any of the areas has shown positive growth in the number of homes sold. As such, and knowing that the PV Hill is considerably smaller that the other areas we measure, readers are cautioned about the wide swings in PV statistics.

Sales volume for the first six months of 2023 is down 26% compared to 2022 (326 homes in 2023 versus 438 in 2022. Similarly, sales are down 9% from 2019 when sales of 358 homes were recorded. Median prices of $1.8M for the same period are down 13% from 2022 prices of $2.1M and up 36% from $1.3M in 2019.

Market time has remained good, with 75% of sales closing withing 30 days. Sellers have enjoyed selling prices 2.3% higher than asking prices, a trend expected to disappear before the end of summer. Once again showing the range of homes available in the South Bay, the high sale in PV was $10M while the low was $610K.

Inland Area Makes Strong Showing

Sales volume of 161 homes in the Inland Area for June was up 33% over sales of 121 in May. With 33% more activity came a 1% reduction in median price, which fell to $875K after reaching $880K in May.

Comparing June of this year to June of last year showed a volume decrease of 3% from 166 in 2022. Likewise, this June showed a median price decrease of 3% from last year’s $905K.

Year to date volume for the first six months was down 68%, for 669 units sold, versus 869 in 2022. Going back to 2019, the most recent “normal business year,” sales volume was down 21% from 799 sold in 2019.

Median price of Inland area homes for the same six month period showed at $863K, down 3% from $887K in 2022; and up 32% from $652K in 2019. Days on market remained under 30 for 82% of the Inland area homes sold in June. Buyers offered 2.6% above asking price. The high market sale was $2.2M while the low was $390K.

Freelance workers and some self-employed people typically don’t have a consistent income. This leads some to doubt whether or not they qualify for a mortgage loan. Lenders will never blanket deny everyone with an irregular income, but it certainly could be more difficult to get a loan. As long as your credit history and debt-to-income ratio are good, it shouldn’t be too much of an issue — you simply may need more documentation to prove that you’re good for it. While lenders will always look at recent income, in the case of irregular income, they may also consider whether or not you’re likely to have clients in the near future based on your occupation.

If you get rejected outright, it’s likely that now isn’t a good time for you to buy in the first place. As long as you aren’t getting rejected, the worst case scenario is a non-qualified mortgage loan, or non-QM loan. Non-QM loans don’t meet the Consumer Financial Protection Bureau guidelines that are designed to ensure borrowers are able to repay their loans, and not all lenders offer them. They may be used for self-employed people, people with irregular income, people with low credit scores, or non-traditional types of properties. Because non-QM loans are riskier for the lender, they do have a drawback for the borrower. They typically have higher interest rates, larger down payment minimums, and/or shorter repayment periods.

The high mortgage interest rates we’ve been experiencing have been the result of benchmark rate increases by the Federal Reserve. The benchmark rate isn’t directly tied to mortgage interest rates, but the benchmark rate does have a strong effect on interest rates. Now, though, no more rate hikes are expected, which should cause interest rates to level off, and then start to decline.

This levelling off followed by a decline is exactly what the Fed was aiming for with the rate hikes. It’s impossible for mortgage rates to drop without the real estate market, and in turn the economy as a whole, taking a hit. By raising rates above what they should be during a period of high prices, what the Fed has done is soften the blow by allowing the decline to be more gradual. Of course, this comes at the cost of significantly decreased affordability for the period of the rate hikes. Once interest rates fall below 6%, which should happen before the end of the year, the market should pick back up again. However, the effect may not be noticed until next year, as the end of the year is not generally a time of heavy market activity.

Some parents want to help their kids any way they can, including by helping them pay their mortgage. Or perhaps they’ve suggested that their inheritance be used for this purpose. Others want to instill the importance of financial responsibility or independence. Some simply can’t afford to help. But if you do want to help your kids with their mortgage, there is some important tax information you should be aware of.

One very common way for parents to assist their kids is with a financial gift. This isn’t just as simple as giving them money. Financial gifts above a certain amount per year do need to be recorded, and may be subject to a gift tax. In 2023, this amount is anything over $17,000 annually, but this value could change each year. Income tax could come into play if instead of gifting your child money, you provide them with a loan. The interest you receive on the loan must be reported as income and may be subject to income tax, and may also be deductible for your child. Capital gains tax is relevant if your kid inherits a property from you or you gift them a property. In the case of a gift, when your kid sells the home, they will need to pay capital gains tax if the home appreciated in value. In the case of inheritance, the capital gains tax amount is based only on the amount of appreciation and not the total value of the home.

Private Mortgage Insurance, or PMI, is a type of insurance that many lenders require for any mortgage with a down payment less than 20%. This is the main reason a minimum 20% down payment is so widely suggested. But if you aren’t able to put 20% down and are forced to take PMI, you needn’t worry too much. It’s also possible to get rid of existing PMI in certain circumstances.

One method that doesn’t require any specific action on your part is to simply wait until automatic termination of PMI, which occurs when you reach 22% equity and are current on your mortgage payments. However, it’s possible to request to terminate it earlier as long as your equity is at least 20%. There are a few ways to do this faster. The simplest option is to pay more than the required mortgage payment. This allows you to reach 20% equity faster while also reducing your PMI costs along the way. Another way you could potentially reduce payments to speed up equity gain is to refinance to a lower interest rate. Depending on your circumstances, this may or may not increase your total mortgage cost excluding PMI, but could eliminate PMI faster. There’s one more possibility: Reappraising your home. It’s possible that your home has accrued enough value that determining the new value of your home reveals that you actually do have at least 20% equity. If you do, you can request to remove PMI.

With how much discussions of real estate tend to pit buyers and sellers against each other, it’s easy to forget they’re often actually the same people. Many sellers are also buyers, either planning to buy to replace the home they’re selling, or already bought another home. This isn’t always the case, of course — it’s entirely possible that someone could have never purchased anything, inherited two homes, and sold one of them. But this isn’t most sellers. What this means is that market conditions that are generally considered to primarily affect buyers will also affect sellers.

Such as right now, where it appears that the high interest rates that are holding buyers back are also making sellers hesitate. The majority of homeowners now have an interest rate lower than the current rates, especially if they took advantage of ultra-low rates such as the rates during the pandemic. If these homeowners were to sell and buy a new home, they would be losing their low interest rate and gaining a high interest rate. For 82% of them, that may not be worth it. Over half of those considering selling right now are deciding to wait until interest rates drop.

Having a 20% down payment used to be a requirement for nearly all loans. That hasn’t been the case for quite some time, but it’s still touted as the conventional wisdom. In many cases, that may be true, but it’s not always the best idea. There are both advantages and disadvantages to putting 20% down.

If you have the money available already, it’s quite likely that the benefits heavily outweigh the drawbacks. Even though 20% down is no longer a requirement to get a loan, it is still a requirement to avoid mortgage insurance fees. Putting 19% down, for example, simply makes no financial sense at all, regardless of your financial situation. It’s also good to put down as much as you feasibly can in order to reduce the loan amount, thereby reducing your payments. The 20% mark is important if you can reach it.

If you still need to save money in order to achieve a 20% down payment, you’re going to need to crunch some numbers and also make some predictions in order to arrive at the correct solution. If you’re close to being able to put down 20%, it may be in your best interest to continue saving up to avoid mortgage insurance fees. But if you aren’t close, it may be best to simply forget about it. Even if you are definitely able to save money, by the time you get to the point that you can put down whatever 20% is now, home prices are likely to be significantly higher. In that case, it may be better not to wait. You also need to consider other costs and where you’re getting the money. If you need to take out a loan or draw on investments to reach 20%, this is probably not a good investment, unless it’s the only way you can viably make a home purchase.

If you’re planning to renovate your home, whether you intend to continue to live in it or to sell it at a profit, you need to think about how to pay for the renovations. Of course, it’s possible you have the cash on hand, which is great. But if not, there are a few financing options you can look into. It’s common to get a home equity line of credit (HELOC) or simply take out an additional loan. However, another option you may not be aware of is cash-out refinancing. It works by refinancing to a loan amount higher than your current loan balance, and taking the difference as cash.

The most important thing to consider when determining if you should get a cash-out refinance loan is the interest rate. It very likely won’t be the same as your current interest rate. If the rate is higher or even the same, it’s probably financially negative in the long run unless you can increase your home’s value significantly with the renovations. That’s why it’s a good option specifically for renovations. On the other hand, it’s entirely possible the rate is lower, or simply lower than traditional loans or HELOCs, in which case it’s a good financing option for any purpose. However, you may not want to use cash-out refinancing for large projects. Since you don’t receive the entire value of the new loan, but only the difference between the new loan balance and old loan balance, you’d need to increase the principal significantly to finance large projects. This could increase your interest payments by quite a bit even if the rate is lower.

The California Housing Finance Agency (CalHFA) recently launched the Dream For All Shared Appreciation Loan, a secondary loan to be used in conjunction with CalHFA’s Dream For All Conventional first mortgage. This secondary loan carries its own set of requirements, which may or may not differ from the initial Dream For All Conventional first mortgage. The requirements of the secondary loan are provided here, but you should consult with CalHFA to be sure that you meet all requirements. The requirements are provided for two categories, both for the borrower and for the property.

The borrower must be a first-time homebuyer, which CalHFA defines as not having owned and occupied a home in the past three years. The borrower must also occupy the property as their primary residence and meet income limits for the program. In addition, the borrower, or at least one of the co-borrowers if there is more than one, for any CalHFA first-time homebuyer loan must take a CalHFA approved Homebuyer Education and Counseling course. This course does have a fee, which varies by method and agency, and can be done online or in-person. The Dream For All program also has its own additional course. Fortunately, this course is free, but it is only accessible online.

The property requirements are simple for single-family residences and manufactured homes, which are both allowed, but may be more complex for other types of properties. Condominiums must also meet the guidelines for whichever initial mortgage you choose. Guest houses, granny units, and in-law quarters may be eligible, but would not be eligible in addition to the main residence, since the property must be only one unit.

Wrap-around mortgages are not very common, but it’s still a good concept to know in case you find it difficult to get a more traditional mortgage loan. A sale with a wrap-around mortgage has two important components distinguishing it from a regular sale: First, the seller retains the current mortgage on the property being sold. This differs from standard sales in which the seller normally pays off the remaining mortgage as part of the sale process. Second, the loan is not issued by a lender but rather by the seller. In this way, the seller is most likely planning to pay their mortgage using the money gained from payments the buyer makes to the seller on their new mortgage.

Wrap-around mortgages have both advantages and disadvantages. The primary reason to get a wrap-around mortgage is that they don’t have any standardized qualification requirements. This mostly benefits the buyer, but can also be useful to the seller if they’re having difficulty finding buyers. The primary drawback is that the buyer and seller must write up the contract themselves, since there is no lender involved. That means both parties need to be legally and financially savvy. It’s also impossible to wrap around a mortgage that doesn’t exist, so the seller needs to have a mortgage. There are also cons specific to the seller and buyer. The seller in this instance incurs the same financial risk that a lender would normally. The buyer is very likely paying a higher interest rate, since the arrangement is not worth the risk to the seller unless they are profiting.

Some of the questions on a mortgage application may seem unnecessary, but they’re all there for a reason. Certain omissions can lower your interest rate and make your offer seem more appealing. But even if you haven’t done anything wrong — especially if you haven’t done anything wrong — you should always disclose all relevant information.

Money changes hands all the time, and the transfer doesn’t always leave a paper trail. But lenders will still find it odd for you to suddenly have additional money or fewer debts. It’s perfectly legal to ask a friend or family member for some cash to help you buy a home or pay off a debt. That money came from somewhere, though, and if you don’t list it, your lender could assume you are hiding something and deny your application.

A common lie that seems more innocuous but can actually have even more drastic consequences is stating that you plan to live in the home when you actually don’t. People do this because interest rate is lower on loans for primary residences, and they figure it’s fine because of course they can always change their mind. However, this is actually a crime. It’s considered a form of mortgage fraud.

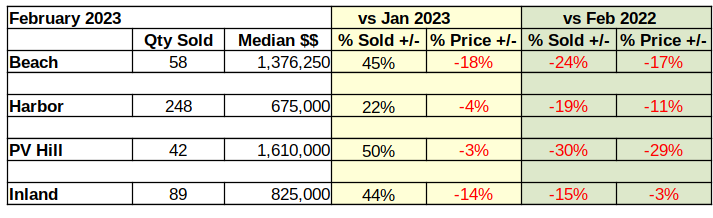

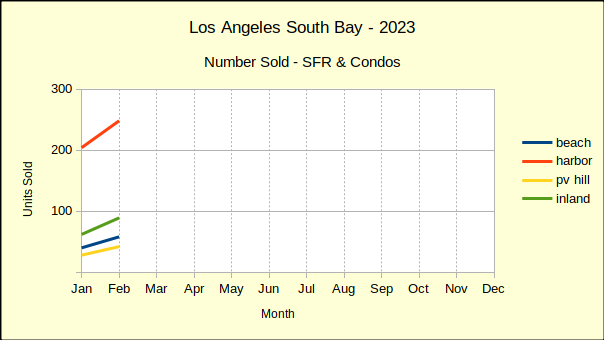

Last year ended with sales volume off, median prices coming down and revenue dropping fast. January showed little change. February of this year shows sales volume up from January by as much as 50%. The reason why is obvious–the median price is simultaneously dropping by percentages as high as 18%.

Comparing February activity to February a year ago shows significant declines in both sales volume and in median price. At that point in 2022 the market was just beginning to dip a toe in the recessionary waters. Now we’re wading into it.

The first week of March Fed Chairman Jerome Powell told Congress, “…the ultimate level of interest rates is likely to be higher than previously anticipated.” Powell’s pointed remark clearly tells us the most recent pause in interest rate hikes is momentary. The lowest local mortgage rates we could find at the time was 6.75%. As such, we anticipate rates in excess of 7% by summer.

February Sales Volume Climbs

About the second week of January mortgage lenders began loosening the interest rates in anticipation of a relaxation by the Federal Reserve. For the most part, local rates stayed below 6% until late in February when the Fed began dropping hints that inflation was still raging.

After a “soft” January, sellers in the market were dropping prices and buyers responding positively by making offers. Now that mortgage rates have resumed climbing, sellers will have to drop prices some more to remain attractive to buyers.

With only two months behind us this year, there are indications lenders will “see-saw” the rates throughout the year. Already this year we have seen retail mortgage rates moving up and moving down without influence from the Fed. It seems to be an effort to induce buyers to accept high interest rates based on the theory they were higher last week so this temporary reduction is a good deal.

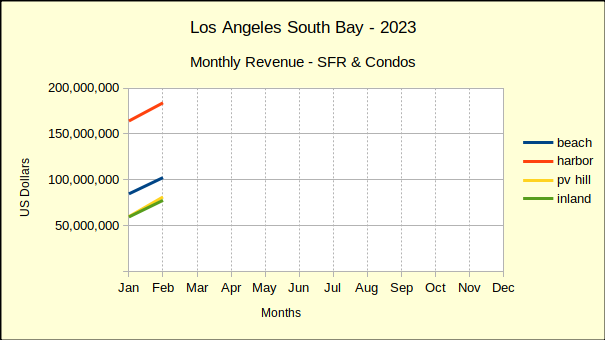

RevenueClimbs From January Depth

On a month-to-month basis, revenue across the South Bay is up 21% from January of this year. Don’t get excited—it’s only one month. January was one of the lowest performing months we’ve seen recently.

On a year-over-year basis, revenue is down 34% from last February! January was 38% lower than January of 2022. Year to date through February, revenue in the South Bay is down 36% and is expected to continue falling.

One of the more important statistics to note is how 2023 activity compares to 2019, which was the most recent “normal” year of real estate business. Across the South Bay real estate revenue for the first two months of 2023 is 7% below the same period in 2019. Restated, the South Bay has already lost over four years of gain in real estate revenue.

Median Price Slips, Volume Rises

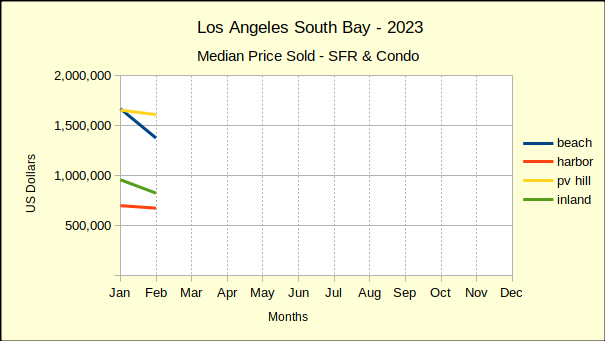

More units of housing were sold in February than January, and the median price was lower in February. The Beach Cities saw a drop of 18% from January while the PV Hill held the decline to 3%. The Harbor area fell 4% and the Inland area dropped 14%.

Comparing February of this year to February of 2022 brought a harsher focus to the picture. All four areas have fallen from last years median price. The Beach is down 17%, the Harbor down 11%, the Hill is off 29% and the Inland cities down just 3%.

2023 Versus 2019 Shows a Sinking Market

The summary numbers comparing the first two months of 2023 to the most recent “normal” year of 2019 are not encouraging. Overall, sales revenue has fallen 7% below revenue figures for the same period in 2019. The Harbor area has fared the best, showing a 9% increase in revenue over January and February activity in 2019. Of course, that was four years ago and classic inflation would give that type of gain. It’s clear the “inflation on steriods” we’ve been experiencing is gone from the real estate industry.

The Beach cities provide an excellent indication of where the real estate economy is going. The first two months of revenue for 2023 is down 32%. Palos Verdes is down 2%, while the Inland area is up be a mere 1%. After four years of pandemic, recession, inflation and Federal Reserve manipulation the real estate market is tanking.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

There’s plenty of advice out there telling you that negotiating your mortgage is important and that you should get multiple opinions. However, unless you know what you’re looking for, you’re probably not actually getting the best deal. On the surface, it may look like the lowest rate you can find, but it likely isn’t. You’ll often need to dig and ask the right questions.

So what are the right questions? Ultimately, you want to know the exact breakdown of the estimate. As you probably already know, interest rates aren’t based on just one factor. You may not realize that some of these factors are actually negotiable, or you may even have more information about it than the lender and be able to correct the estimate. Ask if the estimate includes any discount points. Discount points are an up-front payment that lenders aren’t going to tell you actually lowers your interest rate, rather than being just a standard fee. Discount points are negotiable, but lenders won’t mention that unless you bring it up. The estimate that a lender provides may or may not also include closing costs. Discount points and lender fees are part of closing costs, but a significant portion of them are not actually under the lender’s control. Lenders frequently underestimate escrow fees, so when it comes time for you to pay the closing costs, your fee may be higher than the estimate even if the rate is locked. Make sure to only compare costs the lender can control.

Those who are not citizens or possibly not even residents of the US may have trouble qualifying for mortgage loans. Fortunately, there is an option available, so you don’t necessarily have to be stuck renting if you have just recently moved to the US. ITIN stands for Individual Taxpayer Identification Number, and is a number that the IRS can assign to taxpayers who cannot get a Social Security Number. If you apply and are assigned an ITIN, this can help you qualify to get an ITIN loan.

While you don’t need to be a resident or citizen, there are still some requirements for ITIN loans. You do need to provide tax returns and may have to fill out Form W-7. It’s possible that you will also be asked for additional forms of identification, such as a driver’s license or birth certificate. As with any mortgage loan, you will be expected to provide proof of income, assets, or employment.

We’re taking a little different approach with this post. Because it’s not only the end of the month, but the end of the year, we’re doing a quick summary of the monthly data, followed by some more detailed discussion of how the individual areas have fared over the past year. We’ll even try some crystal gazing while we walk through the annual data for each neighborhood.

This is a great place to bring in our At A Glance table. It displays in just a few numbers how all the areas of the LA South Bay are doing compared to last month, and compared to this same month last year.

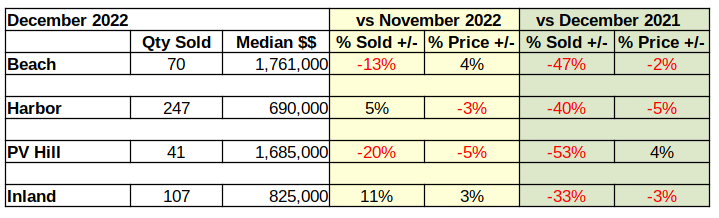

Looking at December vs November, once again the percentage of unsold homes has increased and the number of homes sold below last month’s median price has also marginally increased. More importantly, on a year over year basis the amount of red ink is even greater. Losses in number of sales and in the value of those sales is clearly growing.

Despite all the negative numbers, there may be a light in the future. For the past couple weeks we have observed a softening in the mortgage interest rates. If that turns out to be more than a mid-winter teaser rate, this spring may shine a bit brighter than previously anticipated. We’re not holding our breath though. Recent speeches from Federal Reserve Bank leaders have stated a clear intent to “hold the line” on driving down inflation with mortgage interest rate increases.

Beach Cities Home Sales Down 47%

Compared to 2021, fewer homes have been sold in the Beach Cities every month of 2022 than the same month the previous year. January started the trend with a decline of 28% versus the number of homes sold in 2021. That difference continued to increase all year. By December sales were 47% lower than the previous December.

As the interest rates climbed, the number of home sales dropped. Looking at the total sales volume for the year, 35% fewer homes were sold in the Beach area during 2022, than were sold in 2021. Of course, 2020 and 2021 were the highly erratic pandemic years. So, looking into sales at the Beach for the last few years we find the number of homes sold has already dropped 21% below the number sold during 2019, our last normal economic year. Effectively, the Covid-19 pandemic created. Then erased any gains of the past three years at the Beach.

Homes sold in: 2019 – 1572 (market normal) 2020 – 1572 (market direction down six months, up six months) 2021 – 1910 (market direction down two months, up ten months) 2022 – 1242 (market direction down twelve months)

While the Beach Cities suffered the largest drop in sales volume for 2022, the South Bay as a whole has also dropped below the sales figures for 2019.

Sales Volume Down Across the Board

All areas started the 2022 year down from the prior month and down from the same month in the prior year. February results were mixed with the Harbor and Palos Verdes areas showing stronger results. March sales jumped up as buyers realized the rising interest rates were about to price them out of the market. From April on, sales volume across the South Bay was trending down on a year over year basis.

In sheer number of sales, the Harbor area fell the farthest. In 2021 annual sales 5292 homes were sold in the Harbor cities, while in 2022 the number dropped to 4017. That amounted to only a 24% decrease compared to the 35% annual collapse in the Beach areas.

On a month to prior month measure, sales declined six months out of nine across the South Bay. Occasionally one or two areas would post a positive sales month, but in the end, 2022 showed a 26% drop in sales volume from 2021 across the South Bay.

Sales Dollars Diving

With the number of sales dropping in a range of 25% to 50% it’s not a surprise to discover the total dollar value of those sales has taken a dive. As the chart below shows, the first quarter of the year was generally positive, then reality set in and the buyers started walking away. The rest of the year was little more than a measure of the recession.

Monthly revenue in the Harbor area alone dropped $200 million between March and December. The Beach cities and the Palos Verdes area lost about $150 million a month in sales value. Inland area sales for the same period are off approximately $75 million.

One should consider these declines in the context of the pandemic. Early on, while much of the world was in lockdown, the government flooded the citizenry with easy money, hoping to keep the economy afloat. Mortgage interest rates were already at the bottom because the economy was just recovering from the last recession. The result was a real estate boom starting in summer of 2021, which continued until March of 2022.

The housing market is now in the “bust” part of the cycle and we anticipate it to last through 2023. Gross sales across the South Bay jumped up from $8 billion in 2019 to $12 billion in 2021. That’s clearly unsustainable, especially from the perspective of a Federal Reserve System which is looking for 2% growth. So far the market decline has taken back about 23% of that $4 billion bubble.

Median Price Is Slipping

There is a lull between when buyers stop buying and prices start dropping. Most sellers need to see headlines about the market change before they make a price reduction. Median prices started to slide in August at the Beach and on PV Hill. The year ended with most areas having experienced multiple monthly declines in the median price. Despite that, median prices still exceeded those of 2021 by roughly 7%.

Comparing 2022 to 2019 better shows the inflation factor. Generally speaking the South Bay ended the year with median prices 30%-35% higher than they were in 2019.

The Palos Verdes market is comparatively small, thus is typically volatile on a monthly basis. The yellow line on the chart above shows the range of high and low median prices. Since mid-year the median price has drifted down and merged into the downward trend.

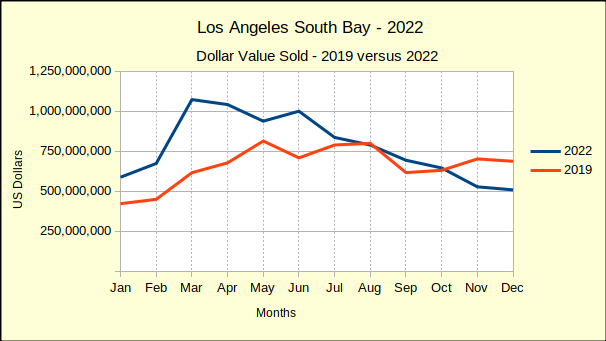

Year End Versus 2019

We’ve been comparing 2022 to 2019 all year because real estate sales during the height of the pandemic were so out of the ordinary, regular year over year comparisons yielded untenable results. The chart below depicts the current year total sales for the South Bay compared to sales from 2019.

Tracking the blue line, one can see where sales dropped below 2019 values in August, recovered in September, then slipped below again for the fourth quarter of the year. December sales didn’t fall quite as far as projected, but still came in about $200 million less than December of 2019.

The end of the year reflected accumulated sales of approximately $9.3 billion. That would mean 2022 total dollar sales come in at $1.3 billion above the $8 billion total dollar value sold in 2019. Across the South Bay that was an 18% increase.

Broken out by community, we found total dollars sold in the Beach cities to be 4% above 2019, followed by the Inland area with a 20% increase. Harbor came in next with a 21% increase and the PV Hill with a 35% increase.

We expect both sales volume and median price to continue declining through most, if not all, of 2023. By mid-year of 2024 there should be evidence of the beginnings of a recovery.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Buying a home is a major life decision. Because of this, it’s important that prospective homebuyers take the time to research the best option for them. Unfortunately, that tends not to happen with mortgage loans. Only about 13% of prospective buyers spend at least a month researching lenders. By contrast, 28% spend just as much time researching cars, and 23% vacation options.

One major reason is that they’re simply not well informed. 30% of prospective buyers believe that their credit score will take a major hit if they shop around, the most common reason cited for not shopping around. This is not accurate, as it’s only getting a pre-approval that reduces your credit score, not consulting with lenders. You can submit as many applications as you want within a 45 day period and your credit score will only drop once. 15% also believe that all lenders use the exact same rate, so there’s no reason to get a second quote, which is definitely not the case.

The terms of mortgage loans have a lot more variance than one might expect. It’s well known that the average interest rate is just that, an average, but there would be no competition if that were the sole factor. Be sure to get lots of estimates, comparing both different types of loans at the same institution as well as the same type of loan at different institutions.

Make sure you understand the terms clearly, especially because some loans have hidden costs. These can include fees for printing documents or prepayment penalties, among others. Not all lenders have these, nor necessarily for all loans, so shop around. It’s also important to know the rate lock period, so you can be sure that the rate will still be valid by the time you finalize getting the loan. Some costs may even be negotiable, such as loan closing fees and interest rate.

Before you get a mortgage loan, ask yourself whether you want a qualified mortgage (QM) or non-qualified mortgage (Non-QM). You may be wondering under what circumstances you’d want your mortgage to not be qualified. Well, there are advantages and disadvantages to both. Non-QMs don’t conform to the regulations set forth by the Consumer Financial Protection Bureau (CFPB), but they’re actually entirely legal — the government simply can’t guarantee consumer protections.

So what are these protections, and why might you want to risk going without them? A QM loan cannot last longer than 30 years, cannot have prepayment penalties, cannot be a balloon loan, and should not have negative amortization. It requires a process for verifying several sources of information, including but not limited to bank statements and income. Because of this, it’s often more difficult to qualify for a QM loan. Therefore, someone who can’t qualify for a QM, such as many gig workers, may risk a non-QM loan. Investors, especially foreign investors, also frequently opt for non-QM loans that only require payments on interest. It’s also possible that you want to go for a longer-term loan, which would come with smaller payments, albeit a higher total amount paid once the loan is fully paid off. In any case, you probably want to ask a professional to explain the terms and risks of any loan you are considering taking, whether qualified or not.

One of the offerings of the Department of Veterans Affairs is mortgage loans. Of course, this is limited to current or past members of the US military. With this restriction comes a few significant benefits if you qualify. VA loans have perks for both low-income and high-income homebuyers.

If you have the money to buy a more expensive home as long as you can get a loan, VA loans may have you covered. There are jumbo loans available which can even exceed $1 million. This may be a good bet even if you are not currently a high-income earner, as long as you are purchasing investment property. This is because there is no minimum down payment for VA loans; you can borrow up to 100% of the home’s value. You don’t even need to worry about private mortgage insurance (PMI), which is required for conventional loans with a down payment under 20%, but not for VA loans regardless of your down payment amount. If your investments pay off, or you start earning more money, you can also pay off the loan faster. VA loans have no penalty for accelerating payments.