Most people who have been paying attention to real estate are aware that the construction industry has been struggling lately. But there’s one area where the industry is doing just fine, and that’s townhouses. Townhouse construction dropped in 2020 along with everything else, but it’s already recovered and is now above pre-pandemic levels. It seems townhouses are simply in fashion right now, as they feel like single-family homes — and are considered as such by some categorization methods — but are generally less expensive.

The truth is a little more complex, though. In reality, townhome construction has been on the rise for about a decade, and 2020 was merely a small dip — which also happened in 2011 and 2012. Perhaps townhome construction specifically was largely unaffected by the most recent recession, and this is just a continuation of the trend. It was actually the Great Recession in the latter half of the 2000s that caused townhome construction to plummet, and it’s been steadily recovering ever since. It’s not quite back at 2006 levels, slightly lower than the 2005 peak, but it’s not far off.

Almost everyone has a few smoke detectors and a fire extinguisher somewhere in their home. If you don’t, you definitely should, and are required to by law in California. Unfortunately, that’s as much care as many people take in their fire safety. That may not be enough.

Smoke detectors should be spaced around your home so that they can be heard regardless of where you are. California requires smoke detectors in certain areas of the home. This includes every bedroom, every hallway that leads to a bedroom, and at least one per floor in a living area. Check to make sure that you are conforming to code, and that your smoke detectors have working batteries. If your home is large, you may also want to consider additional smoke detectors above the minimum requirements to cover more area.

Homes are only required by law to have one fire extinguisher. However, this is the bare minimum and not ideal. You want to have easy access to a fire extinguisher regardless of where you are. The suggested number is one per floor. If you live in a multi-family building, every unit should have easy access to a fire extinguisher. This doesn’t necessarily need to be inside the unit, if there are hallways with access to multiple units. But having just one for the entire building isn’t a good idea, even if there are only a few units.

Technology has made it easier than ever to secure a tenant for your rental property, as long as you’re making good use of the technology. There are several websites that you can use to help spread the word about your listing. Some of these are websites you may use already for other purposes, and others are specific to real estate. You can even create your own website, though you’ll have to make sure people find out about it.

There’s a number of websites that allow you or your agent to list properties for rent. There’s the local MLS, which would need to be accessed by your agent, but this will also spread to aggregator sites like Zillow and Redfin. Alternatively, you can post to Zillow and Redfin yourself. Other similar websites include Zumper, HotPads, and ListHub. Make sure to verify the information after a property is listed, since automated systems can get things wrong. In your descriptions, include certain frequently searched keywords, like the school district, amenities, area, and some basic features.

Email campaigns still work, but it’s not the only way to expand your reach. Social media websites are excellent at this. It’s especially necessary if you’ve created your own website. The obvious ones include Facebook and Twitter. perhaps less obviously, you can post pictures or videos of your property on Pinterest and Instagram. You can also reach out to your network on LinkedIn.

Airbnb is a commonly used method for vacation-goers to find lodgings. It’s usually — though not always — cheaper than a hotel, and often significantly more flexible and easier to book. All of this makes it attractive to people going on vacation. But what about the other party? Is Airbnb a good investment over traditional income property? Well, that depends.

If your property is in a heavily touristy location, it can probably earn quite a bit as an Airbnb rental. Part of this is the per night costs, which add up quickly if you have guests most nights. In addition, cancellations aren’t as backbreaking as losing a tenant. However, overhead costs may be higher, with Airbnb taking a cut and the high likelihood that you’ll be paying for utilities and housekeeping. You don’t want long periods of inactivity with high overhead costs. Unfortunately, such periods are likely because vacations are frequently seasonal.

We’re currently either at or approaching the top of the market, which means it’s generally not a good time to buy. Sometimes it’s inevitable, but that just means you need to be prepared for losses if you don’t keep your home long enough to gather equity. When you buy at the top of the market, your home’s value will go down before it goes up, so you’ll need to wait a while in order to sell at a profit.

If you’re an investor, don’t look at flipping right now. It’s just not going to provide the return on investment that you want, especially with construction costs being high. Instead, look at purchasing rental property, as rent prices are also on the rise. You can collect rental income now and sell much later down the line when the cycle completes itself.

For many people, their goal is to pay off their mortgage so that they can continue to live in their home without any more mortgage payments to make after retirement. This is certainly a good financial decision, but with a bit more planning, it could be made even better. Consider downsizing going into retirement. You may even be able to sell your home and purchase a smaller, cheaper home without a mortgage at all.

That’s not the only way smaller homes are cheaper. Insurance and tax payments would also be lower. Smaller space generally means less utility usage. A smaller home probably won’t have a pool to maintain and may not have much lawn or garden space to take care of. Money isn’t the only thing you’ll save, either; you’ll also spend less time cleaning and maintaining your home. With the time and money you’ll save, you’ll also have the opportunity to take more vacations and relax even further.

Home offices have become more popular as more people are transitioning to work-from-home. This has increased the popularity of larger homes with additional space that can be used for a home office. But a home office doesn’t actually require that much space, and certainly doesn’t need its own room, unless you need privacy.

If you have an attic or basement, either of these spaces can be converted into a home office. Converting the attic can even add to your home’s value, and an office space probably won’t even take up the entire basement. Another feature your home may have is a breakfast nook. Often, this is superfluous and the same purpose is served by a dinner table. It would not be difficult to convert the breakfast nook into an office space. Even if your home doesn’t have any of these features, you can probably find an unused corner of a bedroom or the living room to put a small desk and a chair.

The commercial real estate market has been experiencing mixed performances, with some sectors doing better than others. That’s not about to change any time soon. The industrial sector is still going strong, the retail sector continues its recovery, and the office sector keeps lagging behind.

Already low vacancy rates in industry have dropped to near-zero, as what few vacancies remain are completely unusable. New construction isn’t focusing on the industrial sector, except in the Inland Empire, which nevertheless still has a mere 0.9% vacancy rate, down from 3.1% in 2020. San Diego has the highest vacancy rate in Southern California at 2.3%. In the retail sector, the vacancy rate didn’t change much, only increasing 0.2% in San Diego from 4.7% to 4.9%. However, the availability rate — which includes all properties on the market, whether vacant or currently leased — dropped from 6% to 5%. It’s likely that this is representative of off-market leases. Offices are still struggling, with vacancy rates above 12% and availability rates around 17%. The solution to the office problem will probably come in the form of conversions to residential or mixed-use property, which are far more in demand than office space.

As of the end of last week, the average 30-year FRM rate is at 3.69%. It’s been steadily increasing since the historic lows of 2020. The ARM and 10-year Treasury Note rates also increased between January and February. Periods of historic lows followed by steady increases aren’t necessarily unexpected, though. That’s been the trend for at least the past three decades — ups and downs but a clear overall downward trend. Precipitous drops have tended to result in a period of reduced average. For the past decade it has averaged somewhere around 4%, but it’s unclear whether the sharp decline in 2019-2020 will result in a reduced average for the coming future.

What may prevent a reduced average is the Fed’s plans for the future. Their gradual reduction of purchases of mortgage-backed bonds (MBBs) has kept mortgage rates relatively stable. They will cease buying MBBs entirely in March, at which point they will begin increasing their benchmark rate throughout 2022. This is going to result in higher interest rates. With the rate already approaching 4%, the increasing rates will likely result in the average going above 4% and continuing the trend of the past decade.

While homebuyers don’t necessarily have the experience to know everything they should be considering when buying a home, they definitely know what they want. It may not be easy or even possible to match all the criteria at once, but there are several top priorities buyers look for in an ideal home. These are the factors buyers typically tell their agents they’re considering most.

The first is safety. Buyers will usually research a specific area’s crime rate before considering it, though if they don’t have a predetermined idea of which area they want to live in, they may not know all of the crime rates in various regions. You shouldn’t only rely on statistics, though. Go visit and see for yourself what the area is like. Spend some time there. If you don’t feel safe, you probably don’t want to live there, even if the crime rate doesn’t seem very high. Something else buyers want is proximity to work, friends and family, and community amenities. However, they also want to be careful to balance this with light traffic, while being close enough to main roads. There’s going to be some sacrifice made. Make the commute yourself before buying, instead of just looking at map data. Another extremely important factor for most buyers is having a good school system. It’s very difficult to enrolls your children in a school system outside of your school district, though it is technically possible. Buyers also want to make sure the area isn’t too expensive to live in outside of purchasing the home, meaning low cost of living and low local taxes.

As of the end of 2021, fewer buyers are choosing to waive contingencies than earlier in the year. This is a return to normalcy, as the frequency of waivers was inflated during the period of heavy competition. Buyers had sought to improve sellers’ perception of their offers by foregoing things such as inspections and appraisals in order to expedite the process. As competition dwindled, fewer buyers felt the need to do that. In addition, the appraisal process is starting to move faster with increased vaccination rates, and home prices remaining high means buyers want to make sure they’re getting their money’s worth.

The percent of people who did not waive any contingencies increased steadily from the trough of 21% in June to the peak in December of 40%. Inspection and appraisal contingencies were most often waived, though there are other types of contingencies. For waivers of inspection contingencies, the peak was 27% in July, down to 19% in November and December. The percent waiving appraisal contingencies decreased from 29% in June to 21% in November and December.

Most everyone has had the unfortunate experience of losing their house keys and being locked out of their home at least once. Some people end up having to break into their own home, which can cause some misunderstandings. Otherwise, you’ll have to call a locksmith, or have a spare key hidden somewhere. But you can avoid this entirely with an electronic or smart lock. Not only that, smart locks can also help you keep track of who comes and goes, and it’s much easier to change a smart lock code than a manual lock if it becomes necessary.

Not all electronic locks work the same way, though, and not all of them use smart technology. The most basic electronic locks just require a code to unlock the door. Some use a form of unique identification instead, such as fingerprints, RFID, or Bluetooth recognition. Smart locks have the potential to issue multiple codes to different people, and log which codes have been used when. You also need to make sure that if you plan to connect the lock to your phone, choose a smart lock that is compatible with your model. You should also look into what types of security measures the smart lock has.

More and more young adults are moving back in with family members after college. The assumption is that this is an economic necessity, as those saddled with debt are unable to buy a home. However, even if this is true at the time, it turns out it could be more temporary than expected. Many are transitioning directly into homeownership right after their stay, rather than having a period of renting as most people do.

About half of those living with parents or other family members are paying rent, but it’s likely less than actual market value, though this hasn’t been confirmed. The other half are staying rent free. In both cases, their expenses are much lower than if they were attempting to live on their own. That could be because they can’t afford it otherwise, but it’s also possible they would be able to afford getting their own place, but saving money helps them pay down debt or save up for a down payment. Of course, the vast majority of people — 73% — are still renters before they are buyers, but the percentage who lived with parents, relatives, or friends before buying their first home has increased from 12% to 21% over the past three decades.

Owning a home used to be a large part of the American Dream. Homeownership was considered a point of personal pride, signalling that you’ve achieved something that everyone in the US wants. It still demonstrates the same thing, that you are able to own a home, but nowadays the reasons are far more practical than simply pride.

In 2021, 43% of first-time homebuyers cited pride of ownership as the reason to buy. In 2022, though, this plummetted all the way down to 0%. Instead, investments took the #1 spot at 51%, though this was still important last year at 34%. Replacing that spot is reducing housing costs at 38% in 2022, a similar reason to 2021’s #3 spot, saving money, at 15%. Added to the 2022 list is social pressure at 11%.

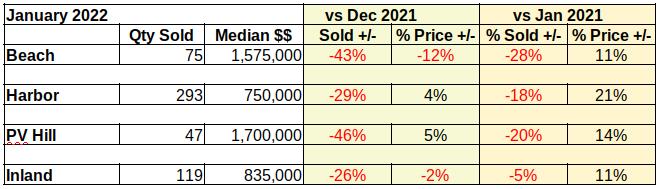

January 2022 showed a different face than we were seeing all last year. Of course, in many respects that’s a good thing. Depending on whether you’re buying or selling, the real estate market for 2022 could be wonderful or horrible. As always, the location will make an even bigger difference.

Sales Volume Dropping

Check out all the red ink in the table below. Compared to December, sales volume is down by nearly 50% at the Beach and on the Hill. November and December of 2021 were heavy with transactions spurred on by the fear of increasing interest rates. The number of homes sold in comparison to January of last year also dropped, though not to as great an extent.

Sales volume down, prices up

As of right now interest rates are expected to hover in the 3.5% to 4% range for the balance of the year. The increase from under 3% to roughly 3.5% has served to lock a substantial portion of entry level buyers into the rental pool. Those who found a place and could afford to buy last year did. The first part of this year is expected to continue to show declining sales volume as many first time buyers drop out of the purchasing market.

Prices Starting to Reverse Direction

Prices meanwhile are faltering in the unsustainable march upward. As the table above shows, the Beach and the Inland areas have already begun declines in the median price. Simultaneously buyers in the Harbor and Palos Verdes communities have continued pushing purchase prices higher, though not nearly as fast as last year.

We expect price corrections in all four areas as the year rolls out. Initially, we anticipate buyers in the Inland and Harbor areas to balk at the combination of higher interest rates and historically higher prices. Lower priced homes are traditionally impacted sooner and to a greater degree by changes in mortgage interest.

Homes on the Palos Verdes Peninsula and in the Beach communities of the South Bay are expected to also experience price declines as the market adjusts to the new reality of higher prices, steeper interest rates and the shrinking impact of Covid.

The Covid Connection

Covid wreaked havoc with social lives, business practices and just about every other aspect of society. When the pandemic struck in 2020 the real estate world was already heated because of low interest rates. Unfortunately, protecting society from Covid meant slowing down much of the business world, including real estate transactions. For months agents were dealing with masks, alcohol gel and the task of wiping every surface touched by potential buyers. And the buyers kept coming because the interest rates made buying a home affordable for many.

By the time 2021 started, the industry had found ways to show property and ways to consummate paperwork with relative safety from Covid. Keeping one eye on the mortgage interest rate, the buying public responded promptly. It was one of the busiest years ever for brokers and agents. As the year ended and lenders continued raising the cost of purchase loans, buyers started showing signs of stress.

January appears to have been the fulcrum point for a shift in market dynamics. The people involved are more than ready for relief from Covid. Bidding wars have all but ended. Price reductions are coming after only a few weeks on the market. The State has declared Covid “endemic.” Essentially we’re ready for normal business.

The first month of the year has pointed in the direction of a slowing market, with some pricing shifts to compensate for over-exuberant purchases in the close out of 2021. We anticipate February to show more of the same. We’ll be back soon with charts comparing the monthly progress. (You’ll find the beginning charts for 2022 at the bottom. Not real exciting without data to compare.)

The High Sale and the Low Sale

We’ve had requests for a little “human interest” added to the dry statistics we throw out here every month. We’re going to try to do that while still maintaining privacy for the people involved. Let us know how we’re doing.

For example, an observation we made this past month was the highest sale versus the lowest sale as reported by TheMLS for January. Those of you who follow us know the Beach areas are invariably at the top of the chart, so you won’t be surprised to find that the highest sale in January was in the Manhattan Beach hill section. New in 2021, this expansive 6 bed, 6.5 bath home sold for $6.5M. At nearly 6500 square feet, that’s over $1,000 per sq ft.

It’s far from the highest price we’ve seen there, but that piqued our curiousity. So we looked to the other end and found the lowest January sale in our part of the South Bay. Down from 6500 sq ft to 400 sq ft, and from $6.5M to $255K, this studio condo in Long Beach calculates out to a hair over $600 per sq ft. In other words, about 60% of the cost to build new construction in Manhattan Beach.

2022 Charts – The Beginning Point

The first chart of the year is less than exciting. We’ve included them here for reference. In March, when we can compare January to February and we can be confident we are past the bulk of the pandemic, these should be much more interesting and informative.

April 2021 was one of the most fiercely competitive months for real estate in history, in no small part due to the pandemic frenzy. But spring is always one of the more active seasons in the real estate market, being right after the holidays. And this year is not going to be an exception.

What sparked so many bidding wars last year is high demand and low inventory, and neither of those things has changed. Inventory is still 43% below pre-pandemic levels, and there are still plenty of Millennials, as well as some Gen Z, aging into first-time homeownership. Where there is some difference is the current state of interest rates, but it’s still going to result in the same type of market. Last year, interest rates were staying low, so buyers knew it was a good time to buy. Now, interest rates are expected to increase throughout 2022. In the long term, this will reduce demand, but as long as the increases are expected and not already here, demand will go up as buyers want to take advantage of the rates before they increase.

There’s a statistic that you may not have ever heard of, but it’s definitely being tracked, and that is the number of homes a buyer views before purchasing. The average has been decreasing, and sits at 8 — a record low — as of last year, compared to a peak of 12 a decade ago. It was holding steady around 10 between 2014 and 2019. As far as length of search time, it’s only ever been lower in the early 2000s.

Part of the recent dropoff is due to low inventory and the heavy competition that followed lockdowns. After all, you can’t look at many homes if there aren’t many to look at and you’re being encouraged to make quick decisions. That’s not the entire story, though. What has enabled buyers to make such quick decisions is technology. Internet-based methods of home viewing are becoming increasingly popular, such as virtual tours and highly detailed photography and videography.

In response to the pandemic, California launched a program to help a segment of the homeless population acquire temporary housing via hotel conversions. This initial project, called Project Roomkey, applied only to those 65 or older or who had underlying conditions, and would only be active during the pandemic. Seeing its success, California has launched a new, more expansive project, which they’ve called Project Homekey.

Project Homekey seeks to expand conversions to include several different types of properties, not just hotels. In addition, the project is designed to create both temporary and permanent homeless housing. This is made possible by the recent changes to zoning and land use laws, and currently has an $846 million acquisition budget. Unfortunately, managing such large projects requires specialized knowledge that isn’t in large supply. In addition, there has been pushback from local opposition that doesn’t want to see low-density housing converted into high-density homeless housing.

The Homeowner’s Exemption is a method of property tax savings that has been in place since 1974. It allows any homeowner who has owned their home since January 1st of the year to apply a reduction of up to $7000 to their home’s assessed value for property tax purposes. The full $7000 reduction will only be applied if the homeowner applies for the Homeowner’s Exemption between January 1st and February 15th, otherwise the amount will be prorated. In addition, parent-to-child transfer benefits from Prop 19 also require the child to apply for a Homeowner’s Exemption within 12 months of the transfer.

Despite the fact that the majority of homeowners qualify for the Homeowner’s Exemption, almost a third of homeowners in Los Angeles County don’t apply for it. This accounts for about $30 million in unclaimed exemptions each year. If you are in LA county, in order to apply, fill out the application at www.assessor.lacounty.gov/hox. It can be printed and mailed to the LA County Assessor’s Office, or emailed to HOX@assessor.lacounty.gov. Currently, there is no fully online application, but there are plans for one soon.

California Governor Gavin Newsom has shifted his priorities for affordable housing development. Previously, Newsom was looking at open rural areas as the setting for new projects. The logic is obvious — rural areas boast a large quantity of land to build on, so you won’t run out of space. Unfortunately, there are other problems. Rural areas are more prone to wildfires and have weak infrastructure, and building there negatively affects the ecosystem.

In light of this, Newsom now plans to focus his efforts and budget on urban projects. The downtown areas already have infrastructure in place, and the land is already in use so the ecosystem won’t be affected as much. Of course, there are also cons to the shift. Urban areas are already high density, and increased affordable housing will only increase the density. Newsom hopes that getting more people into urban areas will reduce vehicle traffic, but in order for that to happen, California would need significant improvements to its public transportation system, which is relatively lacking. In addition, California’s urban areas already have a high vacancy rate. We’re not actually lacking housing; people just can’t afford it.