It’s rather common for neighbors to get curious about open houses and just pop in for a look. Most of the time, they aren’t planning to buy anything, let alone a house right next to where they already are. This has the potential to frustrate some sellers who are perceiving more interest than there actually is, but the neighbor is not necessarily simply being a nuisance. Open houses are an excellent opportunity for people planning to sell, as well.

Buyers usually don’t look in their own area, but as a seller, you can definitely use prices in your own area for a general assessment of the value of your own home. This is especially true if the homes are similar, but even a vague less than/greater than guess is better than nothing. Just keep in mind that it’s only a loose estimate. The price point isn’t the only information you can gather from an open house, though. Recently remodeled homes are great pointers for current trends, and can help you decide on how to remodel your own home. You can also pick up general decor tips. Even the things that you find wrong with the house can tell you what not to do.

Commercial real estate has been struggling in recent years, just as many other sectors of the economy have been struggling. However, one advantage that most commercial buyers have over residential buyers is that they’re more willing to take on debt because their living expenses are likely a lower percentage of their income. As a result, loan originations for commercial properties increased dramatically in the first quarter of 2022.

As can be expected, the effect is greatest in the areas either least affected or most in demand as a result of the 2020 recession. These include hotels, industrial, retail, and healthcare. Loan originations for hotels increased a whopping 359% from 2021. Mortgages for the industrial sector also increased over 100%, by 145%. Increases in retail and healthcare were also significant at 88% and 81% respectively. Lesser increases were noted for multi-family dwellings at 57% and offices at 30%, but these still increased, not decreased. However, one should note that the available data isn’t entirely up to date. Mortgage rates have increased significantly since Q1, so despite the fact that they’re starting to slip back down just now, there may have already been a downward trend in commercial loan originations that we haven’t noticed yet.

Primarily as a result of actions by the Federal Reserve, mortgage rates have been trending upward since January. The rates peaked in June, and have now begun their decline in July. ARM rates are currently more volatile than FRM rates, and may continue to flip-flop, but they are still lower than FRM rates.

The 30-year FRM rate peaked at around 5.7% in late June. It’s since dropped slightly to 5.3% as of the first week of July. The 15-year fixed rate followed a very similar trend line, albeit at a lower peak rate of just under 5%. This is normal; the 15-year rate has always trended lower than the 30-year rate. The ARM rate was 4.34% at its highest in June, and has now dipped below 4%.

It’s pretty typical for first-time homebuyers to purchase a starter home, one that is cheaper and smaller, but that they aren’t planning to live in for an extended period of time. First-time homebuyers expecting children soon, or even who already have children, will instead tend to purchase a larger home that their kids can grow up in. But kids aren’t the only reason to skip the starter home, if you are able to afford something better.

While it’s true that any home you live in will build equity, this is mostly proportional to the value of the home and time owned, barring dramatic shifts in neighborhood desirability. Therefore, a cheaper home that you live in for only a few years will build less equity than a more expensive home that you live in for decades. In fact, if your time spent there is unusually short, it may not even cover the costs of selling the property. There are also less tangible benefits to going straight for your forever home. Getting settled in a community can take a number of years, especially in high-density areas where there is typically a larger percentage of low-income housing than in medium-density areas. If you’re moving out in a few years, you may never feel established as part of the community or be able to form lasting connections.

It’s common for sellers to perform a few upgrades to their home just prior to selling, in the hopes of fetching a higher price. But there are some upgrades that simply aren’t worth it. Of course, if you’re planning to stay living there, you can go through with these upgrades for yourself. You shouldn’t expect them to help you get a profit, though.

Bathroom remodels are tricky. While remodeled bathrooms are appealing to buyers, they’re also rather expensive. The return on investment usually isn’t very high. Also, if any problems arise, it could result in a much larger amount of time and money spent than expected. This could delay the sale significantly and reduce your profit, even if the end result does bring in interested parties. Living room updates are neither in high demand nor quick. Moreover, if it’s not done in a way potential buyers would want, it could actually reduce interest. While many people nowadays want home offices, unless you need one for yourself, don’t break down walls to convert existing bedrooms. Bedrooms are far more versatile, as they can be used as offices without any structural renovations, or used for their intended purpose. A home with 3 bedrooms and no office is worth more than a home with 2 bedrooms and an office.

Wood floors are in high demand and significantly increase the value of your home. Unless buyers are specifically looking for the softness of carpeted flooring, even false wood is more appealing than carpet. Of course, hardwood is always going to bring the highest increase in value. Because of this, you may think that if you already have hardwood floors, you don’t need to change anything. But you should still consider replacing it, since new hardwood is even a significant improvement over old hardwood.

It’s fairly simple for buyers to tell if your flooring is old. Hardwood gets scratched and its color dulls. Heavy use and oversanding are easy to spot. Some of these issues can be fixed by simply refinishing it, but if the damage is more than simple wear and tear, such as nails sticking out or boards coming apart, you absolutely want to replace it. Your buyer is going to anyway, so you may as well get more value for your home while improving buyer interest. Even more importantly, old flooring can pose structural issues. This can be spotted anywhere the floor seems to move too much when walking on it.

A certain element of the homebuying process that sometimes crops up, especially in competitive markets, is the homebuyer love letter. This isn’t actually a declaration of love, except possibly for the home they’re trying to buy. A love letter is simply a personalized note included with an offer in an attempt to connect to the seller on an emotional level. Sellers respond to this variously, and may simply ignore them if they’re receiving them constantly.

But the major issue with love letters isn’t the question of their effectiveness. The problem is why they have the ability to be effective. If a seller has a reaction to a love letter — whether positive or negative — and uses this in their decision of which offer to select, it means they’re biased based on some personal detail of the buyer. Most of the information a buyer would provide doesn’t have protected status, but if it does, the seller could be sued for discrimination. Of course, it’s very difficult to prove exactly why the seller accepted one offer over another, so this rarely actually happens even if the buyer suspects discrimination. But this is exactly why some states have banned love letters, or, in the case of Oregon, are trying to ban them.

You may already be aware of the value of staging your home to attract buyers. Just knowing that you should consider it doesn’t actually tell you how to accomplish that, though. It’s important to note that people spend a lot of time in their bedroom, even when they aren’t sleeping. It’s a place for a multitude of forms of relaxation. So, you want it to look relaxing. If you’re having trouble making your bedrooms look appealing to buyers, maybe these tips will help.

Be careful not to make the place look too much like you, specifically, live there. While staging does involve decorations of some sort, otherwise the place will simply look bland, the decor needs to be somewhat more generic. This allows buyers to imagine themselves living there. On a related note, you should choose neutral colors. You don’t know what colors the buyers will like. They may repaint anyway, but you don’t want to turn them off from even trying. White bed coverings and curtains are best, as they amplify lighting. The position of the furniture is also important. As one would expect, the bed is generally the focal point of a bedroom. It should be situated such that it provides a sense of balance. If possible, put it across from windows or doors. Try to make sure there is space to move around the bed. If none of this is possible, at least place the bed against the room’s longest wall.

When renters are faced with rental price increases, as they are now, it’s typical for them to look for a cheaper place to rent. They don’t always find one, of course. But with the current inventory, it’s riskier to even look for one than to simply accept renewing their lease at a higher rent value.

Between April 2021 and April 2022, the share of renters renting at market value who chose to renew their lease increased from 53% to 57%. This is despite an 11% increase in rent prices during the same period. The problem is that there simply isn’t anywhere more suitable to go, partly because of low construction rates. Without renter movement, the number and type of vacant units doesn’t change very much, which further stagnates the market because what few vacancies exist are already deemed to be undesirable.

It is currently believed by experts that the US is heading towards another recession. It’s not a guarantee, and it won’t be for around six months if it does happen. So what exactly is a recession, and why is another being predicted? Many people are only aware of a recession as being a period of economic struggle. But it has a technical definition, which is two consecutive quarters of shrinking GDP. GDP is definitely not the entirety of the economic picture, but the conditions for a recession almost certainly indicate job loss and lower wages. What’s being predicted is simply a prolonged reduction in overall consumption, and this is mostly because interest rates are going up.

The Fed is purposefully raising interest rates in an attempt to reduce inflation. But a reduction in inflation doesn’t necessarily translate to no recession. If interest rates rise too quickly, it could actually cause a recession during a period of high inflation, which is called stagflation. This is what happened in 1981. Currently, experts believe the Fed is increasing interest rates too quickly. And it’s possible that they shouldn’t increase the rates at all; the prospect of increasing rates to reduce inflation is based on the outdated concept that high inflation is triggered by high wages. It’s true that businesses often like to take advantage of increased wages by raising prices without a significant decrease in demand, but this is calculated corporate greed, not an economic law. Perpetuating this idea only further lines the pockets of the already wealthy.

You’re likely aware that having a pool will probably increase the value of your property. But if that’s your only reason to get one, you may want to rethink your plans. It may or may not be a good idea, depending on the circumstances. Of course, if you want a pool anyway for your own use, you may be less inclined to care about the numbers. However, regardless of why you want a pool, there are several factors to consider.

A pool is expensive. It’s not like some small upgrades that can have a major impact over time for a low cost. Unlike energy upgrades, pools don’t generate more value as time goes on; their value changes only with buyer demand. In fact, a pool will actually cost you more money over time, in addition to the large up-front cost. Cleaning and filtering costs add up over time, and having a pool increases your insurance costs. If your plans don’t include using the pool, it may not be a good return on investment. In addition, depending on the area, you may not actually want to increase your home value. Pools are ultimately a luxury feature. If you live in a low-cost area, it’s unlikely that prospective buyers searching in that area have large amounts of money to spend. Conversely, if you live in a high-cost area but don’t have a pool, adding one could help bring your home some more appeal.

In order to figure out how best to organize your closet, there are two major questions that need to be answered: What can it store, and what do you want to store? The first question may seem obvious, but many people don’t actually properly measure their closet. You’ll want to know exact dimensions and also account for storage aids such as rods, dividers, and shelving. Figure out how to get the most out limited space. You can even hang hangers on other hangers, if you need to.

The second question is rarely considered at all. Any leftover space is generally occupied by anything that can be shoved in there with the clothes. This isn’t optimal, and you should really plan ahead what exactly you want to go in your closet. For example, snow clothes probably don’t need to be there. You’ll only wear them in winter, so you don’t need easy access to them most of the year. Think about what you use each item for, and group the items by function. Also, clothing doesn’t even have to be what it’s used for at all. Maybe all or most of your clothing can be put in a dresser, leaving room in the closet for things like sheets or towels.

Hard Rain, featuring Andy & Renee is a perennial favorite in the South Bay, taking the title of Best Original Music Band nearly every year. While Andy & Renee perform as a duo at several different venues each week, the whole band gets together about once a week for an outdoor performance. Below are the next few weeks of gigs for Hard Rain with Andy & Renee. For more information about the band or the duo, tickets when required, and the full calendar, go to https://andyandrenee.com/

South Bay Festival of the Arts, Torrance

Saturday, June 25, 1:00pm — 2:30pm Torino Plaza, Torrance Cultural Arts Center, 3330 Civic Center Drive, Torrance, CA 90503. Event runs 11a-5p. Our set time is 1-2:30pm.

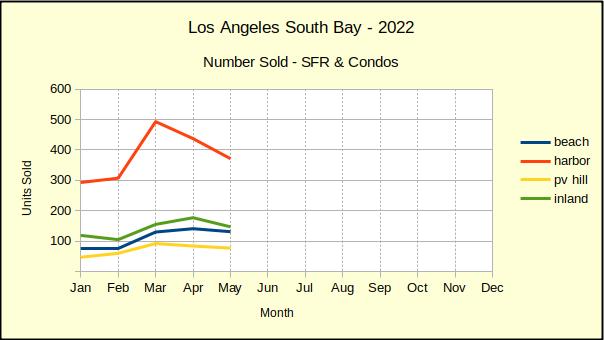

The number of homes sold in the South Bay has declined from last month, and has declined from last year. The quantities are actually rather dramatic given that May is typically a time of increasing sales. The drops range from -7% to -17% lower than April sales of this year, and from -17% to -25% below May of last year.

With over half the year remaining, mortgage interest rates have doubled, currently sitting around 6%. The hike in interest rates has so far reduced the average buying power by about -25%. Coupled with home price increases estimated to have risen 38% since the start of the pandemic, the immediate future of real estate looks dismal.

Inflated consumer prices are also blocking potential home buyers as the Consumer Price Index (CPI) climbs toward a 10% annual hike. There’s little chance of saving for a down payment when the price of everything on the shopping list is going up..

Retirement accounts are often a source of down payment funds. As of this writing the major stock market indices are all down: Dow Jones Industrial Average, -16%; S&P 500, -22%; Nasdaq Composite, -31%. Forecasts are growing for a Fed-induced recession that may begin as soon as this fall. Some potential buyers may see borrowing from their retirement fund to purchase a property as a means to preserve the capital during a recession. Others may not be in a position to do that.

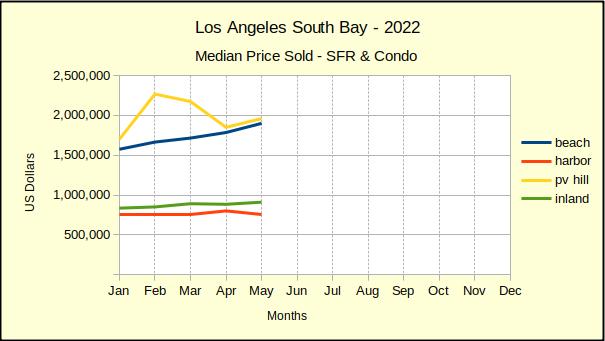

Median Price Sold

May prices delivered a mixed message. The Palos Verdes Peninsula, which had seen two months of decline from a temporarily high median price, headed back up again. The Beach cities continued a steady climb, and the Inland area showed a modest price increase after having dropped 1% in April.

However, the Harbor area, which is as large as the other three areas combined, took a -6% hit to prices. We anticipate the Harbor and Inland areas, which comprise the bulk of the traditional middle class family homes in South Bay, to be the first to react to the economic stress.

Typically, the recession cycle starts with a slowing of sales. As properties languish on the market, sellers begin to reduce prices. One after another, median sales prices will drop until the price reduction offsets the impact to buyers. At that point, buyers will begin to support the reduced purchase prices and we can see growth in the market.

Experts differ in their estimates of how long this cycle will take, and when we can expect the market bottom. There are some predicting a rapid fall based on the speed with which the Federal Reserve Bank (Fed) is reacting. The June meeting of the Fed ended with a .75% hike in the prime rate, and a promise to raise it at least another .75% before the end of the year. While that could slow the economy as early as the beginning of 2023, more conservative minds suggest the end of 2023 for a turn-around.

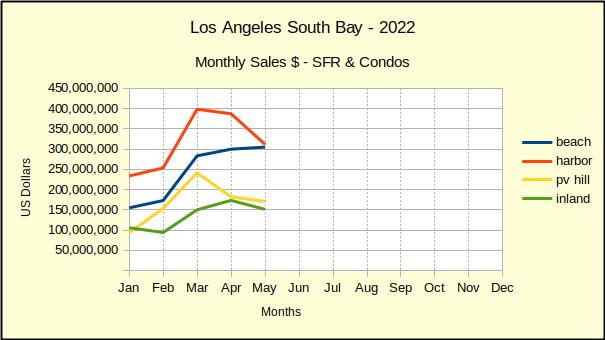

Area Sales Dollars

The total sales dollars tell the truest story. While sales are slowing and median prices are beginning to slow, the combination shows up here.

Everywhere except the Beach is showing reductions in total sales on a month to month basis, and on a year over year basis. The declines are small to date, with year over year ranging from -1% to -10% in May. Month to month changes ranged from +2% at the Beach to -19% in the Harbor area.

These early numbers follow the general pattern we’ve seen in recent recessions, whereby entry level homes are the first impacted and the last to recover. We anticipate the Harbor area to lead the charge down, followed by the Inland area. Recent years have shown the Beach to be the strongest growth area, so we expect the recession to hit there last, following declines on the Hill.

The nature of the impending recession is still uncertain. Some pundits are saying that at least initially we should expect “stagflation,” that odd environment we first encountered back in the 1990s when prices of everything continued to climb, along with job layoffs and massive unemployment. Other forecasters suggest that because the international economy is roiling with continuing high tariffs (courtesy of the last administration) and new monetary sanctions daily (courtesy of the current administration), this particular recession may last much longer than normal.

In Summary

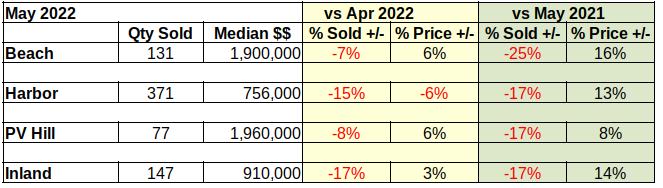

As the table below shows, the majority of the negative impact for May happened in the quantity of housing units sold. With one exception, prices continued to escalate. We believe this is temporary and likely to change before the end of the year. The -6% drop in median price at the Harbor presages the direction of home pricing as inventory grows and listings stagnate.

Approximately 3 out of 4 listings coming across our desk recently have been either Price Reduction or Back On Market. That means property is staying on the market longer. The Average Days On Market (DOM) for May ranged from 10 days on the PV Hill to 14 days in the Harbor area. As recently as this winter we were still seeing multiple offers on the first day the property was available.

Another measure of the market condition is how far the average sales price declines in the first 30 days on market. We did a quick look for May and came up with these statistics. Thirty days after the original listing, the price had dropped from the original: at the Beach, -9%; the Harbor -6%; PV Hill -18%; Inland -5%. As of May, we’re also seeing property that has been on the market for several months, with several price reductions.

Notable Properties

The high and low sales for May were not terribly dramatic. A Manhattan Hill section home and a downtown Long Beach condominium. Thay are simply very big, and very small.

High Sale

Located at 812 5th St, this Manhattan Beach hill section home was originally listed at $10.5M and sold for $8,980,000 after 34 days active on the market. The home offers six bedrooms and seven full bathrooms in 5576 sq ft. Amenities included ocean view, pool, spa, custom waterfall & fire features, a full basement with recreation/media room, home theater, storage, a temperature-controlled wine cellar, and private guest quarters.

Low Sale

Measuring barely 381 sq ft, the studio condo at 819 E 4th St #25 sold for $215,000 in one day. Located in the vibrant East Village of Downtown Long Beach this tiny home offers a remodelled kitchen and bathroom. The unit sits on the second floor, overlooking the intersection of 4th and Alimitos and within walking distance of many downtown shops, clubs and eateries.

Born out of the Covid pandemic, Jodi Siegel’s Songwriters’ Showcase is an exceptional opportunity to hear original music played by the same people who created the songs. Jodi’s been making music for a while, and claims many of LA’s most notable musicians as close friends.

The folks that stop by the Project Barley Brewery on the third Tuesday of every month for Jodi’s show are not your typical beer pub crowd. Many of them are musicians in their own right, and many are songwriters who have, or will, perform in a show. Indeed, audience members have been known to step up and fill in on a keyboard or with a guitar when a song called for another instrument.

Below we’ve included a pitch for the June Songwriters’ Showcase. We go every month and are delighted every month!

Songwriters’ Showcase – June 21, 2022

It’s nearly summer and the music community is also warming up with gigs galore and music fun to be had everywhere you turn! I’m grateful to be working a bunch of local gigs too…but first check out the new songwriter’s night coming up in less than two weeks!! June 21, 2022 I’m proud to host three good friends and killer songwriters: Harold Payne (Bobby Womack, Snoop Dogg), https://haroldpaynemusic.com/Alfred Johnson (Rickie Lee Jones) https://www.facebook.com/alfredjohnsonmusic/https://www.facebook.com/alfredjohnsonmusic/and the one and only Chauncey Bowers (new CD now available!) https://chaunceybowers.com/https://chaunceybowers.com/It’s also my Birthday on that night so it’s gonna be a party!! As always come early to grab a table. This is a free event, donations go to the musicians.Project Barley’s is located in Lomita (south of Torrance/Redondo on PCH). They have great food, wine and beer! ! For more information check out their website https://projectbarley.com/MEET OUR NEW SONGWRITER’S SHOWCASE SPONSORSI adore these two wonderful folks! Everybody’s cheerleaders in the music community! For all your real estate needs give them a call or check out their website :https://carl-and-arda.beachcitybrokers.net/TO CHECK OUT WHO IS COMING IN THE NEXT FEW MONTHS GO TO https://jodisiegel.com/songwriter-show

Commute times in California, and indeed across the country, have increased in recent years, as people have moved away from job centers. The theory was that this was mainly due to work-from-home options. For some, that may be true, but many of these people aren’t working from home, they’re just commuting longer to work. Surely long commutes aren’t desirable, so what are they getting in return?

The missing factor is lower housing costs. Job centers tend to be larger urban areas with higher prices. By moving to more out-of-the-way areas, workers have reduced their mortgage and property tax at the cost of longer commutes. With gas prices on the rise, it’s not entirely clear whether this is a good financial choice. But more importantly, the people who are making this choice are the ones who have the financial means for it to be a choice. Over three quarters of higher wage workers work somewhere they can afford to live, whether they live where they work or not. Lower-wage workers don’t have an option. Only 4% can afford to live where they work, so they’re forced into longer commutes to find affordable housing.

With the current market’s low inventory and high prices, buyers are struggling to find entry-level or starter homes. There is one type of home they can afford to buy, though: fixers. These also aren’t in high demand, so competition isn’t as fierce. The problem is, first-time homebuyers typically don’t want to spend extra or can’t afford the additional cost of fixing up their homes. But that can be resolved with home renovation loans.

Two common home renovation loans are the FHA 203k loan and the Fannie Mae HomeStyle loan. Both require a minimum credit score of 620 and a minimum down payment of 3%. They cover most home improvements, including both structural and cosmetic. However, keep in mind that the FHA 203k loan can only be used for primary residences, while the HomeStyle loan can be used for both primary residences and investment property.

An increasing number of people are seeking ways to contribute to the environment. While a single person isn’t going to suddenly solve the climate crisis, every little bit can help. Planting gardens improves air quality and also gives you access to fresh fruits, vegetables, or herbs, while also slightly improving your energy efficiency. Some other energy efficiency upgrades can also significantly reduce your annual costs.

Everyone knows about solar panels, and you may even have already upgraded to solar energy. But there are other solar energy upgrades you may not be aware of. There are solar attic fans and solar water heaters as well. If you haven’t upgraded to LED lighting yet, you definitely should. LEDs are massively more energy efficient than regular lightbulbs, which translates to much lower utility bills. They also last longer, so you won’t need to spend money on replacements as often. Even windows have gotten energy efficiency upgrades. Energy efficient windows combined with good insulation reduces the workload of heating and cooling units.

The idea of open concept living used to be pretty hot, but it’s started to cool down recently. Shifting trends in usage have made open concepts less useful to most families. That doesn’t mean the advantages have disappeared; they’re just not in high demand right now. This is mainly a result of COVID-19, which has made the advantages less appealing and the disadvantages more salient. Ultimately, though, it’s a personal choice.

But what are these pros and cons? The biggest con is noise. Open concept floorplans have fewer walls and doors to muffle sounds from other rooms. With more people transitioning to work-from-home, the added noise is distracting people from their work. In addition, having lots of empty space is just not a priority for most people. Yes, people want larger homes, but that’s to accommodate more usable space, not empty space. The biggest benefit of open concept living, and the reason it rose to popularity, is that the wide open spaces with good natural light allow for excellent entertainment spaces. However, the pandemic had drastically reduced the appeal of hosting indoor events. What it does still accomplish is creating a feeling of togetherness, even when family members are in different rooms.

Project Barley’s is located in Lomita (south of Torrance/Redondo on PCH). They have great food, wine and beer! ! For more information check out their website

Project Barley’s is located in Lomita (south of Torrance/Redondo on PCH). They have great food, wine and beer! ! For more information check out their website