The aftershocks of the Great Recession are already here. We’re currently in the midst of a second, undeclared recession, albeit a less severe one. The lower severity doesn’t necessarily mean lower impact, though. Government assistance is what pushed us through the Great Recession, and that’s unlikely to occur again.

A recession doesn’t have to mean a market crash, but it’s a very real possibility. Some areas are at higher risk of a crash than others. The highest risk metros are those with high loan-to-value ratios, home flipping, new residents, and rapid home price growth. In California, these metros are Riverside, Sacramento, Bakersfield, San Diego, Stockton, and Fresno. Those aren’t the only areas that may be affected, though. Market problems in any one area will also cascade to other regions.

As a result of the Federal Reserve’s decision to increase benchmark rates, both fixed and adjustable rate mortgages have been increasing. Rates are now beginning to reach a stable point. Of course, the rates are in constant flux, but the fluctuations are starting to level out. This doesn’t mean a reversal of the recent increases; the 30-year FRM rate is levelling at somewhere around 5.5%, which is still relatively high in comparison to recent years.

What it does mean is that the uncertainty regarding rates is decreasing. With this, the popularity of ARMs will drop, as uncertainty is their primary drawback. They had experienced a surge of popularity while FRM rates were similarly unstable, since FRM rates tend to be higher than ARM rates during the same time period. This is despite the fact that ARM rates also drastically increased between July 2021 and July 2022, from 2.48% to 4.30%.

In heated markets, it’s difficult for buyers to negotiate prices down, since their competition will likely be offering more. Now that the market has begun to cool, buyers are looking for ways to pay less. The answer is greater scrutiny of home defects — not to avoid purchasing defective homes, but to reduce the home’s value so they can offer less for it.

Sellers are always required to disclose any significant defects or malfunctions they are aware of in a large range of categories. These categories are walls, windows, ceilings, doors, floor, foundation, insulation, driveways, roof, sidewalks, fences, electrical systems, plumbing, and sewer or septic systems. While it can be difficult to prove that a seller was aware of a defect and the notion that it’s significant is subjective, it’s good advice for the seller to disclose anything they know. Since there’s a high chance something will have to be disclosed, buyers are jumping on the chance to leverage this to negotiate a lower sale price.

When a homeowner sells the home they live in, their most common move is to use the proceeds to buy a replacement property, if they haven’t already done so. While it seems like homeowners would always remain homeowners, it does happen that people transition from homeownership to renting. But in most cases, the seller has decided to sell high and then rent for a short time while waiting for prices to bottom out. This is called timing the market.

This is not what’s happening now. Home prices and mortgage rates are both high, which is pricing homeowners out of their current home — and pricing 80% of them out of the market entirely. They aren’t waiting for a better time to buy; they’re simply no longer able to afford ownership. They become renters by necessity. Fortunately for people in such a predicament, it may not last too horribly long, though certainly longer than they would have wanted. It’s expected that prices will reach bottom around 2025.

Most of the time, vacations don’t last that long — a few days or maybe a few weeks. Homeowners are generally okay with leaving their homes unattended for that length of time. But what if you’re vacationing for the entire summer or winter? It’s simply not practical to leave your home vacant for three months or longer. You may want to rent out for home for the length of your vacation.

A three-month rental contract may not seem like a long time, but is actually considered a long-term contract, not a short-term contract. So it’s not any more complex of a process than any other standard rental contract. The most obvious benefit is the income generation, but there are less obvious reasons to want to keep your home occupied. Vacant homes are the primary target for burglaries, so if you have tenants in your house, you’re less likely to be a victim of crime. Tenants can notify you of any problems that arise, and also take care of regular maintenance such as mowing the lawn, though you should make sure to include this in the contract.

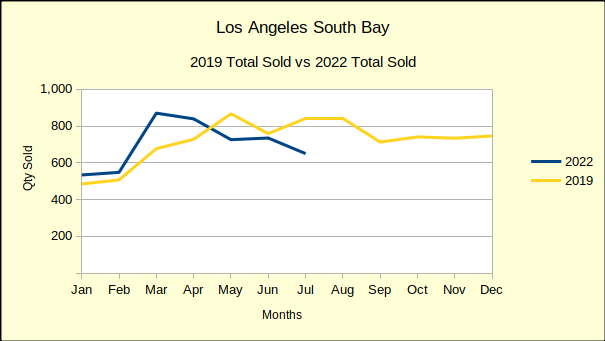

The 2022 recession appears to be coming in stronger and faster than predicted. Year to date home sales in the South Bay have dropped -17% compared to 2021 sales through July. Month to month, the change from June to July was -12%. The July drop followed a lackluster June performance of only 1% over May which was itself down -13% from April.

Money was cheap and readily available in 2021, and the Federal Reserve Bank (Fed) was fore warning everyone that the mortgage interest rates were going to rise. The number of homes sold sky-rocketed, purchased both by owner-occupants and by investors hoping to snag interest rates at the absolute lowest in decades. Along with that came the bidding wars and the escalating prices. Looking back, one can readily see a correction in the making. At the time most experts were considering 2021 a trade-off for all the transactions lost during the 2020 lockdowns.

The last year we could consider normal was 2019. Compared to 2019, the number of homes sold during the first seven months of 2022 is nearly identical, hinting at a return to normalcy. However, a deeper look shows recent months dipping as much as -25% below 2019 sales volume. If sales volume continues to drop at this pace, we can anticipate starkly lower prices before the end of the year.

Steeply climbing interest rates have cost today’s buyers over 25% of their purchasing power so far in 2022. Some of those potential buyers will simply buy a less expensive home. Some of them will wait and save longer for the down payment. Some of them will become permanent renters. On the other hand, sellers have fewer options. They can decide not to sell, if that’s possible for them, or they can lower the price until a buyer can afford the home.

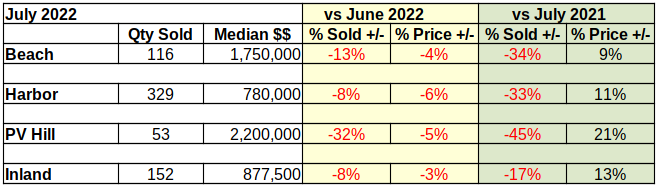

Median prices fell in all four market areas for July versus June of the current year. The overall drop was approximately -5%. (See chart below for detail.) So far in 2022, median prices have remained higher than those from last year. But, since April of this year median prices have consistently fallen on the year over year comparison. As noted earlier, we anticipate the median price dropping below last year sometime this fall or early winter.

“Should we wait to purchase?”

We hear this question a lot, and the answer is an unequivocal “No.” In the end result, chasing the elusive “bottom of the market” is a fool’s quest. By definition, when one recognizes the bottom of the market, it‘s already gone. We recommend that when you find a home that meets most of your needs and is within your budget, you should move on it.There are several reasons.

First, because the Fed is already projecting future interest rate changes which could easily eclipse the savings to be found in a correction. Alternatively, those future rates will prevent some potential purchasers from qualifying for a loan.

Second, because economics today is a web that reaches around the world. As we have seen just in the first few days of August; allowing grain movement on the other side of the world will affect our stock market, and available interest rates overnight. We live in a very volatile world and a perfect deal today may not exist tomorrow.

Sales Volume Down, Inventory Up

In March of this year there was essentially no inventory of homes for sale in the South Bay. Sellers were reporting literally dozens of competing offers on the few homes available. Today, in August, there is easily two months of inventory and homes are sitting on the market for increasingly long periods of time.

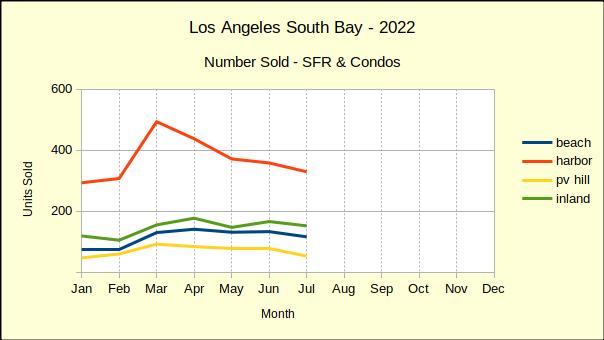

Sales in July fell in all four sectors. The Harbor area has now shown declining sales in four consecutive months. PV Hill sales have been off three of the last four months.

The Average Days On Market (ADOM) for the homes sold in July was 17, meaning it took 17 days from the time it was listed on the MLS until an offer was accepted. The ADOM for the homes currently active on the MLS is 46 days, a full month longer than those closing escrow in July.

A lesser known indicator of market condition is the number of homes that don’t sell before leaving the MLS. In July alone, 194 homes fell off the MLS. Of those, 41 Expired never having received an acceptable offer. The remaining 153 were removed because buyers were not showing interest at the listed price. Some of those sellers truly need to sell and will come back at an improved price. Most of them were hoping for a financial windfall and have set aside their plans.

Median Price Falling for South Bay Homes

The median price fell in July for all areas. The hardest hit was the Harbor area with a -6% drop in the median. The Hill was next, with a -5% loss, followed by the Beach and the Inland areas with -4% and -3% respectively.

Of the 116 homes sold at the Beach, 22 (19%) required a price reduction before getting an offer. The Harbor required 59 out of 329 (18%), the PV Hill 9 of 53 (17%), and the Inland area 17 of 153 (11%). Those were price reductions necessary to get an offer on the property, followed by a successful sale. Let’s look at properties active on the market, still trying to get an offer.

As this is written, the Inland area, shows 211 properties available with 77 having taken one or more price reductions already, without receiving an offer. That represents 35% of the currently available Inland homes. Homes at the Beach show 96 reduced of 228 (42%), on the Hill 53 reduced of 140 (38%), Harbor 215 reduced of 547 (39%).

So we see that nearly 20% of the homes sold in July needed a price reduction to get an offer. We also see that roughly 40% of the homes currently on the market have had one price reduction and may need further changes to stimulate offers.

Total Sales Revenue

The decrease in the number of homes sold in July, combined with the decline in median price for those homes pretty much guaranteed that the total sales value would drop as well. Across the South Bay revenue fell from last month by -16%. This will not make our tax assessor happy. Interestingly enough, Los Angeles County Tax Assessor Jeff Prang recently announced with pride a $122 billion growth in County property tax assessments as of January 1, 2022.

The Beach area fared the best, dropping only -2% in value. We noted quite a number of homes being sold as furnished rentals in July, like this one in Hermosa Beach. The Beach Cities are noted for their short stay vacation rentals (often referred to generically as AirBnBs) whether approved by the various cities, or not. Unfortunately there is no official accounting system for these properties. Even if one existed, many of the operators would be very resistant to a governmental accounting which could cause them taxation issues.

For the moment, Beach values seem to be the strongest of the South Bay. The Inland area followed with a -9% decline in total sales dollars. The Harbor area was next, off by -17%.

On the surface homes on the Palos Verdes Peninsula took the worst beating with a -41% decline in value from June sales. We remind our readers that the PV Hill is small by comparison to the other areas. As such, statistical measurements often appear distorted because many of the homes are unique and generate significant sales prices. Having said that, this month was a relatively mundane one for PV. Of the 53 sales, the low was an attached two bedroom, two bath condo which sold at $557K. The high sale was a six bedroom, 8 bathroom house in Rolling Hills which sold at $8 million. (For your valuation purposes, click here to see photographs and descriptions of the two homes.)

Lots of Red Ink

The table below shows the percentage of change in the number of homes sold and the median price of those homes two ways. The yellow shows change for the current month versus the prior month. The green shows change for the current month versus the same month last year.

From a seller’s perspective, these numbers would ideally all be black/positive. When any of them become red it shows a retrenchment in the South Bay real estate market.

From a buyer’s perspective the red ink is a good sign. It means purchasers can get more home for their money. For them, the real savings will come when that last column turns red.

August 16, 2022 will be an epic soul/blues show at Project Barley Brewery & Pizzeria with Preston Smith, Brophy Dale, Mike Malone and organizer; Jodi Siegel. Put it on your calendar–it’s gonna be rocking!

Preston Smith

Guitarist Preston Smith is a multifaceted talent that has enabled him, both with his band and solo acoustic, to have worked with legends like: Robert Cray, Albert Collins, Foreigner, Salt-N-Pepa, The Red Hot Chili Peppers, Bonnie Raitt, Social Distortion, Wall of Voodoo, Concrete Blonde, Savoy Brown, Charlie Sexton, k.d. lang, John Mayall, Tower of Power, Joe Satriani, The Ventures, Dick Dale & the Deltones, Eric Burden & the Animals, Delbert McClinton, Paul Butterfield, Poco, Santana and many more!! His one man band performances are mind blowing!!

Brophy Dale

Guitar player Brophy Dale, originally from Texas, has worked with The Stray Cats bassman Lee Rocker, as well as Robert Lucas of Canned Heat, Smokey Wilson, Joe Houston, & King Ernest to name a few, on the Southern California blues scene. He’s also had the opportunity to work with some of his heroes, which include Dave Edmunds, Delbert McClinton and a few tours with Scotty Moore.

Mike Malone

Keyboard/vibe player, Mike Malone has shared the stage/ recorded/ worked with Eddie “Cleanhead” Vinson, Mick Taylor, Jimmy Vaughn, Mark Ford, Top Jimmy, Papa John Creach, Pee Wee Crayton, Guitar Shorty, Joe Houston, Deacon Jones and Big Joe Turner.

He plays with many Southern California bands including the Broughams, The Mighty Mojo Prophets to name a few and his jazz trio; an instrumental band featuring his fine vibe playing!! Mike recently released a solo album called “Just Passin Thru.”

Jodi Siegel

Host, guitarist, singer/songwriter Jodi Siegel has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and more.

She can go from funky bluesy grooves to folk, to jazz and back again with ease. She’s an old soul with a fresh sound.

Patrick Simmons (Doobie Brothers), Walter Trout, Maria Muldaur and more, give her new CD, “Wild Hearts,” rave reviews!

Wild Hearts is produced by Steve Postell (Immediate Family, David Crosby) is filled with great songs, cool grooves, intimate, smart lyrics and some of the best of the best musicians in Los Angeles today.

Conventional wisdom is that it’s more financially sound to buy a house than rent, if you can afford to do so. However, this may not be entirely true anymore. While house prices and rent prices are both increasing, house prices are increasing at a much higher rate. The gap between mortgage payments and rental payments increased from $25 in April 2021 to over $800 a year later. This difference is the highest in over 20 years. Unless you’re planning to live there for over thirty years, you’re probably better off renting. Importantly, this is based on a down payment of 5%, which is significantly lower than the commonly recommended 20%, but many buyers may not be able to afford a 20% down payment.

This won’t be permanent, but it could last several years. Home price growth has already started to lessen, but interest rates are high right now. Prices aren’t expected to be at a low until around 2025. Increased construction could aid in further reducing home prices. Given that we’re seeing the the beginnings of another recession, though, that probably won’t happen until a couple years after prices bottom out. Even after a return to normality, California is still going to have a lot of renters. With many lower-income workers permanently priced out of buying, the state has consistently had the first or second lowest homeownership rate of any state, frequently swapping places with New York.

In most cases, getting a mortgage loan requires a home appraisal. Usually, this is a rather long process that involves extensive analysis of a home by an appraiser, inside and out. But sometimes the process can be expedited by using a drive-by appraisal, in which the appraiser only looks at the home’s exterior. The other advantage, besides the speed, is that it’s much less invasive for any current occupants, especially if they are tenants. Of course, this is at the cost of a much less in-depth evaluation.

Also, it’s not always possible to get a drive-by appraisal. It’s essentially at the discretion of the lender whether a drive-by appraisal is allowed. If the lender wants a full investigation, they simply won’t approve the loan. That said, more and more lenders are permitting them as a result of COVID, since evaluating the interior can be risky. Lenders are also more likely to allow a drive-by appraisal for a refinance as opposed to a new loan.

The Biden administration recognizes that the best way out of the current housing crisis is to bolster supply through additional construction. In order to meet this goal, the new Housing Supply Action Plan was recently unveiled in a White House press release. The five-part plan is expected to solve the crisis within five years, and mostly addresses issues of financing.

The first part of the plan is aimed at directly assisting builders with increased resources and new programs. The plan also modifies federal grant prioritizations based on a new system of scoring for zoning and land use reform. Additional financing options will be provided for manufactured housing, ADUs, and smaller multifamily properties. In addition to new financing options, the plan expands existing Fannie Mae financing programs. The last part of the plan is unrelated to financing or construction; it prevents institutional investors from purchasing REO properties in favor of allowing them to be purchased by owners intending to occupy the property.

When getting a mortgage loan, that money generally comes from a bank. But it’s important to realize that a bank isn’t just an impersonal repository of money. Banks are businesses, and as such, they’re always looking for profit. This extends to deciding your interest rate, which is nearly always not the best rate you could get.

One of the ways banks pull a profit is by looking to the future of interest rates. They will frequently take an expected future average rate rather than the current average rate if they expect rates will rise soon. They get slightly ahead of the game this way. The other reason rates are often higher is not entirely within the bank’s control, although it is partially a result of their actions. A common method of reducing risk is for a bank to sell debt to an investor. This also frees up capital for the bank. But it introduces an additional party also looking for a profit, and the bank may need to make concessions for the deal to go through. Increasing interest rates is a way to recoup these losses.

Renovations can be expensive. Even if you can afford it, lowering the costs may end up being a better return on investment, even if the renovation is less extensive or lower quality than you wanted. Of course, if you can do the renovations yourself, that is by far the cheapest — though most time-consuming — option. But even hiring contractors has the potential to be much cheaper than you’d think.

When performing home renovations, the immediate assumption is that all the additions are going to be brand new. That doesn’t have to be the case. Gently used products may still be better quality than what you have now. The contractors you’re hiring may even have just taken some cabinets from a previous client — ask if they have anything suitable on hand that they would need to get rid of somehow anyway. You may even be able to do everything through one contractor. Though you’re still paying for every renovation, you may avoid repeated fees by not being charged by multiple companies. Of course, you may have to scale back your renovation plans to do this. Not every company is willing or able to perform every renovation.

One smart home feature you may not have heard of is smart windows. There are a couple reasons for that. First, they’re rather expensive and therefore not widely available except for industrial applications. Second, they’re actually a much older concept than what in modern days is called a smart feature. Smart windows originated in the 1980s and are a type of window that can be darkened or lightened by application of either electricity or heat, depending on the type of window, termed electrochromic or thermochromic.

Electrochromic windows are actually already in use, though generally not in houses — they are used on privacy screens, display panels, and vehicle windows or sunroofs. Thermochromic windows, while equally old in concept, haven’t been seriously produced until recently, with advances in two-way thermochromic glass. Old generations of thermochromic windows used a substance called vanadium dioxide, and a newer model uses a combination of water and hydrogel. Both are viable and have their own pros and cons. Cheaper models may be commercially available in about ten years, though they will still be more expensive than standard windows.

One of the most sought-after pieces of information to learn about a potential new neighborhood is the crime rate. No one wants to move to an unsafe area if they can avoid it. Even if you are required to move there because of a situation outside your control, you’ll want to know what you should be on the lookout for and how prepared you need to be. There are a few different websites to help you learn more about crime in your new neighborhood.

SpotCrime and CrimeReports are very similar. Both allow you to enter an address and gain an instant report of recent crimes in the neighborhood. They also both allow you to sign up for alerts. SpotCrime additionally lets you provide information to help others anonymously. Neighborhood Scout provides per capita crime rates in any neighborhood you select, not just your own, and also has a comparison feature that allows you to find other neighborhoods with similar crime rates. Family Watchdog has a more narrow purpose. It specifically looks for the locations of registered sex offenders and informs you if one is living in the area.

With high interest rates, more and more buyers are beginning to realize they can no longer afford to buy, or would prefer to buy something less expensive. Sometimes this moment of realization hits them after they’ve already signed a purchase agreement, and now they want to back out. This is entirely legal, but does come with some potential costs.

When prices are increasing, breach of contract isn’t a huge deal, but can annoy sellers who have to delay their home’s sale. But when prices are decreasing, as is beginning to happen now, sellers have more to lose. Which is why they have a few different options to remedy the situation: they can enforce the purchase agreement, relist their property, or just withdraw the listing and wait for a better time. If the seller chooses to relist, they may be entitled to compensation from the buyer who breached contract. If the profit from the sale after relisting is less than what it would be given the original contract amount, the amount of the buyer’s deposit that would be returned to them is decreased by the amount of the seller’s losses. There may be cases in which there was an agreed-upon limit to this amount, in which case the agreed-upon limit is used, plus an interest rate of 10%.

There’s a lot of talk about first-time buyers, from their impact on the housing market to advice to help them secure the home they want. Not as many people talk about first-time sellers. Of course, many first-time sellers already have some experience with the real estate process. They probably bought the house they’re trying to sell, though it’s possible they inherited it. But that doesn’t mean they have experience with selling, and they could still make mistakes.

First-time sellers are often thinking about how much money they can get, rather than whether or not they even can sell successfully. While getting too little money for the sale is a bad idea, you won’t get any money at all if your house doesn’t sell. Instead the primary focus should be on making sure you get offers, then you can enter negotiations. Don’t try to cut corners by selling without an agent. It is an extra expense, for sure, but most prospective buyers won’t even know your property exists without the help of an agent. The agent can also help you set a realistic listing price. If it’s too high, you won’t generate interest, and if it’s too low, people will assume there’s something wrong with the property. Even once you get offers, don’t just pick whichever offer is highest. Take a look at the terms of the offer. The buyer could be asking you to pay for certain costs, which could make a slightly lower offer actually a better deal. In addition, a slightly lower full cash offer avoids financing headaches and possibly some closing costs.

We’ve said for years that land on the Palos Verdes peninsula is undervalued. We may not be able to say that much longer. Last month property on the Hill took another big jump upward in median price. That’s the second time in six months. When that yellow line peaked in February we found several new construction homes closed escrow in the same month boosting the median price dramatically.

PV Median Up $364K while Beach falls by $80K

This time we found two homes, selling in the same month, at over $10,000,000. To put that in perspective, during the past 12 months only four properties on the Hill have reached the $10M mark. So what are these rarefied houses that bring in over-the-top median prices? Let’s take a closer look. (Photos at link.)

The listing agent described 2005 Paseo del Mar as a single level with 5 bedrooms, 4 1/2 baths, formal living and dining rooms, 2 family rooms, pool, 4 car garage with gated entry and circular driveway. So what makes it worth $12.4M instead of $2M?

It seems 4582 square feet of house sitting on over an acre of land on the bluffs above the Pacific Ocean is worth about $10M more than if it had an inland address.

Similarly, 1417 Lower Paseo la Cresta is a grand estate offering over 15,000 square feet of lavish living space spread over 3 levels, with 9 bedrooms,13 bathrooms and two full kitchens. Additional highlights include the custom 15-seat theater, Italian Fantini mosaic pool, elevator, generator and an extensive home automation system.

Beach Cities Sales Down -34% From 2021

The Inland cities clearly leap-frogged the other three areas in volume of sales for June. Sales in the Inland area out-paced the rest of South Bay, erasing a -17% decline from May of this year and adding a +13% increase for June .

The next closest monthly sales volume was a +2% at the Beach. Harbor area sales showed the poorest comparable performance, dropping by -4% for the month, continuing a three month slide. Monthly sales volume in the Harbor area has declined 135 units just since March.

Let’s focus on the Harbor and that red line on the chart for just a moment. Remember this is an entry level market, where a little rise in the mortgage interest rate can quickly price a new buyer out of the running. Notice that sales in the Harbor area were at about 300 homes per month in January. By February a few buyers had noticed the interest rates climbing and took the leap.

Then March became the proverbial “last chance” to buy in the fast moving current market. Sales volume shot through the ceiling with a 61% increase in homes sold. Since then we have watched a classic collapse with prospective buyers melting into the woodwork, waiting for another opportunity.

Annual statistics are still reflecting the impact of two plus years of pandemic. Compared to June of last year, sales were down dramatically. The Inland area fared the best, coming in with a drop 0f -6% from 2021. Sales in the Beach cities and the Harbor area fell the farthest with a -34% and a -29% respectively.

Total Dollars Sold Up 71% In Just Two Years

Back in 2020, the first six months of the year had netted slightly over $3.1B in South Bay home sales. Fast forward to the first six months of 2022 and total sales is slightly over $5.3B. Restated, that’s a 71% increase in dollars spent on real estate in just two years.

Much of that increase was the result of the phenomenally low interest rates created by the Federal Reserve Bank (Fed) to offset the financial impact of the pandemic. It was good for all those people who wanted homes and had down payment money. Investors did especially well, though we saw another big expansion of the inequality gap.

Coming out of the pandemic, we’re seeing the four areas moving erratically. The steep climbs of 2020 and 2021 seem to be leveling off, as the Fed tries desperately to slow what is viewed as a runaway real estate market.

Total sales dollars in 2019 were $7.9B, in 2020 up to $8.7B, and in 2021 up again to $12.1B. Since mortgage rates are still climbing, it’s a little early for forecasting, but we anticipate 2022 total sales to come in at about $11.3B.

Where Are We Going?

Comparing last year’s market to 2022 shows a continuing decline in sales, while simultaneously a continuing increase in median prices. That may still change before the end of the year.

In May we saw the quantity sold drop into the red numbers across the South Bay. For June the sales volume is only off in the Harbor area, but the Hill and the Beach are both marginal. We expect sales to gradually slow as the year closes. Indications are the Fed will ratchet up the mortgage interest rate another 2% which should bring transaction volume down substantially.

May also saw the median price drop at the Harbor. Then in June the median fell for the Beach cities and the Inland areas, while the Harbor bounced back. We expect both the median and the sales volume to fall back into the red zone by the end of the year.

Sales volume should move first. Then as sales slow and buyers become more selective, sellers will begin retrenching on price. We don’t anticipate major price reductions until 2023. However, there are a lot of moving parts to this years economy. Events on the other side of the world may still make big changes here.

If you’re in a situation in which you think you’ve settled on an area for your new home, but aren’t getting your offers accepted, you may need to think a bit creatively. Chances are you’re only looking at homes that are currently listed for sale. This may seem obvious, but it’s not the only possibility. Though it most commonly only happens between people who already know each other, it’s not illegal to make offers on off-market homes.

A good way to skirt the opposition is to look for recently expired listings rather than active listings. Your agent can easily set up this search for you. If a listing expired recently, it means the seller probably did want to sell, but wasn’t getting offers. It could also mean the seller wasn’t very serious about selling, but you won’t know which unless you contact them yourself. There’s also another option that’s less likely to work, but more likely to get you what you want if it does work. If you see what you think is your dream home, but it wasn’t on the market at all, you can still try contacting the owner. For the right price, they may be willing to sell even if they weren’t trying to. There are certainly some homeowners who aren’t listing their home only because they think they won’t get a buyer.

Project Barley’s is located in Lomita (south of Torrance/Redondo on PCH). They have great food,(Gourmet pizza, sandwiches, gluten free/vegan options and of course wine and beer! ! For more information check out their website https://projectbarley.com/

At about 7pm on the third Tuesday of every month, we indulge our taste for live music. Jodi Siegel created the Songwriter Showcase as a means to bring original songs, performed by the original songwriters, to local people. There isn’t a bad seat in the house, and by 7pm every seat is filled with music lovers. Come on down and check it out! Here’s this month’s program.

Tracy Newman : Tracy is founding member of The Groundlings Improv Theatre, which is one of the main farm companies for SNL. She was a TV writer/producer for 16 years, starting as a staff writer on Cheers. In 1997, she won an Emmy and Peabody Award for co-writing the groundbreaking “coming out” episode of Ellen. In 2001 she co-created the ABC comedy, According to Jim. Tracy has been playing guitar since she was 14 and is now a full-time singer/songwriter, doing shows for both adults and children. She has a new company called Run Along Home, focusing on age-appropriate lyrics for very young kids. Tracy’s CDs for adults: A Place in the Sun, I Just See You,and That’s What LoveCan Do to Your Heart. Her CDs for children: I Can Swing Forever, Shoebox Town, and Sing With Me. Websites: www.tracynewman.com and www.runalonghome.com.

David Plenn: Singer-songwriter-guitarist, Plenn has developed a career as a in demand sideman, a producer as well as a professional songwriter. His “Easy Driver” was a 1978 chart entry for Kenny Loggins, while “The Forecast (Calls for Pain)” — produced by another important musical mentor, writer-producer Dennis Walker — appeared on Robert Cray’s 1990 album “Midnight Stroll.” His tunes were heard on such hit TV shows as Beverly Hills 90210, Melrose Place and Touched By an Angel.

David’s new album, produced by Plenn and Lloyd Moffitt and comprising 10 beautifully crafted, emotionally affecting original songs, finds the veteran Southern California performer backed by a group of longtime colleagues who rank among the region’s best-known players: legendary singer-songwriter-arranger Van Dyke Parks (architect of the Beach Boys’ Smile), drummer Jay Bellarose (Elton John, Bonnie Raitt, Aimee Mann, etc.), bassists Jenny Condos (Bruce Springsteen, Jackson Browne, Stevie Nicks, etc.) and James “Hutch” Hutchinson (Willie Nelson, B.B King, Linda Ronstadt, etc.). Several other contributors — Moffitt, vocalists Tara Austin and Llory McDonald, bassist David Jenkins, drummer David Goodstein — backed the late singer- songwriter Jerry Riopelle during Plenn’s decades-long association with the musician. For more about David, go to his website https://davidplenn.com/

Michael McNevin: Michael’s songs read like short stories, full of heart, humor, and a keen eye for detail. Winner of the Kerrville New-Folk award in Texas, Performing Songwriter Magazine “DIY Artist Of The Year”, 7-time grand finals “Song Of The Year” winner for West Coast Songwriters. Accomplished guitar work and seasoned vocals underscore the characters and places he comes across in his travels. He grew up in the train town of Niles, CA, in the east bay hills the San Francisco Bay Area. He started out playing underage in East Bay bars, mixed in a six-month stint busking the streets and subways in New York and has has since logged 25 years on the U.S. songwriter circuit.

He’s shared hall stages with Johnny Cash & The Carter Family, Donovan, Shawn Colvin, Richie Havens, Iris Dement, Greg Brown, Christine Lavin, Robert Earl Keen, and many of others. He’s been a main-stager at Strawberry, High Sierra, Kerrville, Redwood Ramble, American River, SummerFolk in Canada, and the Philadelphia Folk Fest. He’s also been a 3rd place finalist at both the Rocky Mountain Folks and Telluride Troubadour Competitions in Colorado, and was nominated Artist Of The Year by the National Academy of Songwriters. He tours as a solo act in the US and parts of Europe, and occasionally gets a band together as McNevin & The Spokes. In addition, Michael is an Etch A Sketch artist of some renown, delighting and dumbfounding audiences. Not kidding, he illustrates his songs on the little red toy. Michael has been a guest on CBS “Evening Magazine”, plus segments on NBC, ABC, and dozens of cable music shows.

When he’s not on the road, Michael also owns and operates the Mudpuddle Shop, in downtown Niles, a former barber shop. Now in it’s 14th year, it is a 15’x15′ creative hive for showcases, workshops, song swaps and jams. His Etch A Sketch drawings hang on the walls, waiting for an earthquake.. https://michaelmcnevin.com/

Jodi Siegel: Jodi was born in Chicago, IL. The Home of the Blues! She eventually relocated to California and began playing and singing in countless blues, R & B, pop and original music bands throughout Orange County, San Diego and Los Angeles. Over the years Jodi has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and countless others. Her songs have been recorded by Maria Muldaur (“So Many Rivers To Cross,”-cowritten with Daniel Moore and “If I Were You”-cowritten with Danny Timms) Marcia Ball (“So Many Rivers To Cross.”) and Teresa James (“Come Up and See Me Sometime”-cowritten with Danny Timms)

MEET OUR NEW SONGWRITER’S SHOWCASE SPONSORS I adore these two wonderful folks! Everybody’s cheerleaders in the music community!