Although it was undeclared, we’ve been in a recession, which is usually indicated by two consecutive quarters of gross domestic product (GDP) loss. GDP has been going down, but now suddenly GDP is going back up. So does that mean we are out of the recession? Well, if it had ever been declared, it would be declared over — but that doesn’t mean it actually is, especially since it was never declared to begin with.

GDP is ultimately based on consumer spending. When consumers spend more, GDP goes up. This is indeed what happened. However, that isn’t necessarily a good thing. You may have read one of my posts from a few days ago about plummeting savings rates. As stated in that post, savings rates have recently dropped dramatically, which is normally an indicator of consumer confidence, but in this situation is actually a result of necessity due to increasing costs of living. In other words, inflation occurs, consumers must spend more to buy the products they need, therefore GDP goes up. We tend to think of GDP increases as good, but the reality is that it’s simply a mathematical value that can shift as a result of a variety of different factors, both positive and negative.

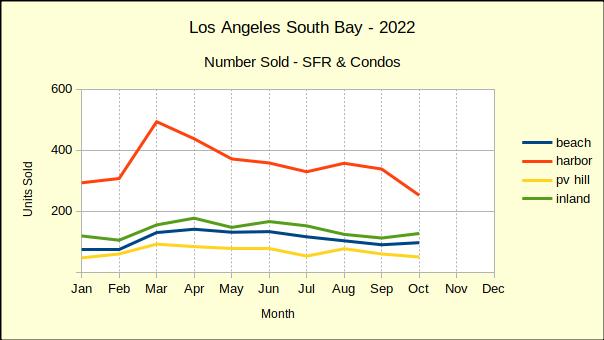

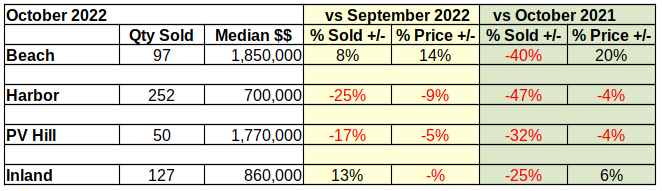

Compared to October of last year, home sales in the Los Angeles South Bay have dropped by 40%. Hardest hit was the Harbor area which fell 47% from last year’s October numbers. The Beach Cities were down 40%, while the PV Hill and the Inland area fell 32% and 25% respectively.

Month to month sales across the South Bay were down another 12% compared to a 9% drop in September. Looking at the different communities found mixed results. The Beach and Inland areas improved sales over September statistics, while the Harbor area and PV Hill continued downward. Harbor area sales plummeted another 20%, falling from -5% last month to -25% in October.

The pandemic created a wild roller-coaster ride for Harbor area real estate. Being the least expensive of the four areas, Harbor area homes are the most affordable and attracted the most attention when interest rates were ultra-low and entry level buyers were able to qualify for purchase loans. Now, with the interest rate already double the 3.5% of 2021, many potential buyers no longer have the cash flow to purchase.

Note that 476 Harbor area homes sold last October versus 252 this October. Looking back to 2019, the most recent “normal” year we find there were 397 homes sold in the Harbor area. This demonstrates how artificially inflated sales figures were in 2021 and how far sales have already fallen in just seven months from the peak.

In mid-November, following another .75% increase by the Federal Reserve System, the Mortgage Bankers Association is reporting a drop of 46% in mortgage applications to purchase a home compared to last year. That decline is accompanied by an 88% decline in applications to refinance a home loan. That amounts to a lot of money out of circulation in the economy.

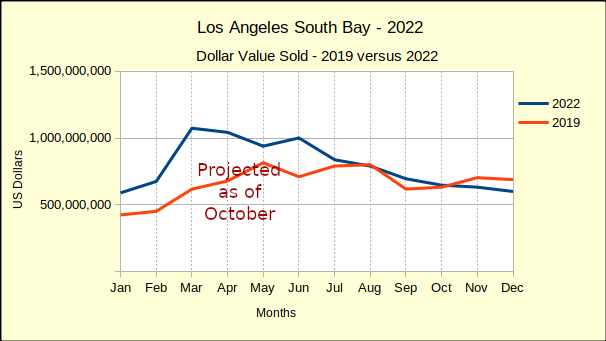

Total Dollars in Sales Declines $1.8 Billion

As of the end of October South Bay home sales for 2022 total $8.3 billion. That compares to $10.1 billion for the same time frame in 2021. Already this year the gross sales revenue has fallen by $1.8 billion, or 5%. As the market slips deeper into recession, we expect the monthly sales revenue will continue to decline, shrinking the total even more.

The graph above shows the downturn starting in March and generally trending down for the balance of the year. It’s important to remember that home sales are a major driver in the economy. Every home sold results in a miniature boost to the economy as new homeowners relocate, acquire new furniture & appliances, repair and update their new home. Most experts estimate an additional 15%-20% for ancillary economic activity stimulated by real estate sales.

Using 2019 as a baseline, we can trace the rise and fall of the South Bay real estate market through the pandemic. In 2019 the total cumuilative sales was $7.9 billion. In 2020, when the pandemic hit and the government began piling on financial assistance and incentives, the annual sales reached $8.7 billion. When 2021 rolled around the ultra low interest rate alone was enough to drive annual sales to $12.1 billion, an increase of 53% over the 2019 sales figures. Looking now at 2022, we are forecasting a year end total of approximately $9.5 billion, a decline of 22% from 2021.

An additional concern this year is the reduction in local and state tax revenues. The pandemic forced significant governmental expenditures to mitigate harm to citizens. A recession, coming on the heels of Covid-19, threatens to up-end the economy. California’s budget reserves haven’t yet recovered from the pandemic and state revenues are already slipping.

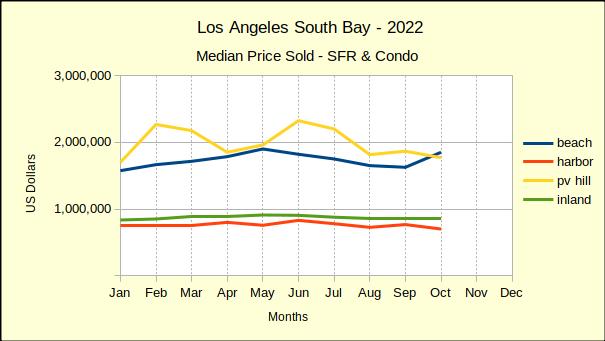

Median Price Shifting Down

Wealth is often measured by the value of owned real estate. For most families their real estate is the home they live in, which is valued per the median price of comparable homes. Thus, nearly everyone is interested in the median price for the area.

Year over year, comparing 2021 to 2022 for the same month, the median price continued to rise until August of this year. Since then results have been “choppy” with median prices down August, September and October for PV Hill sales, down two months out of three at the Beach, down one month in the Harbor area and up all three months in the Inland area. (How the areas are defined may be found at the end.)

Looking month over month, comparing each month to the one prior, shows a clearer picture. January started the year with declines compared to December, both at the Beach and in the Inland area. By July and August all four areas were showing declines compared to the prior month. The repeated monthly decreases in the median prices built up to the annual decreases which began showing up in August and have continued through October.

When Is It a Recession?

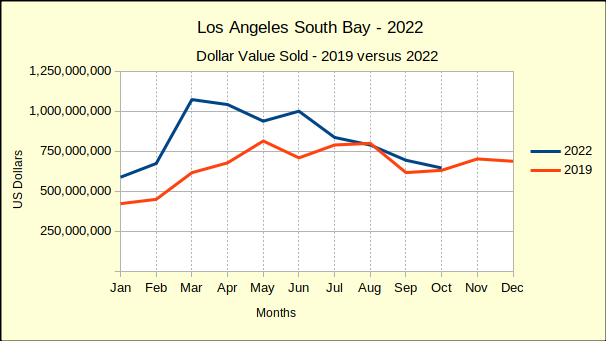

Since June of this year the total dollar value of South Bay sales has been declining. Combined, the precipitous drop in number of homes sold and the gradual decline in median price are driving the revenue below that of 2019 on a monthly basis. The chart below shows August as the first occasion where the total dollar value of homes sold in 2022 fell below the monthly sales in 2019. October sales for this year ended just shy of the same month sales in 2019.

Our projections (shown below) for the 2022 year end indicate the total sales for the year will fall below the 2019 total sales dollars. While this isn’t an official definition, or designation, it matches our understanding of a recession. Any time our financial situation is headed backwards in time we think of it as a recession.

The challenge now is to consider how this recession will play out in time. The Federal Reserve System (Fed) has changed the game rules since the Great Recession. A prominent change has been the speed with which the Fed raised the prime rates for member banks. In response to the Great Recession, the Fed gradually raised rates over a period of years. This gradually slowed home sales. This time, the Fed has raised rates much faster, resulting in much more immediate impact on the real estate market.

At the moment, all expectations are for another rate increase in December, despite indications the economy is crashing. A seriously disappointing Black Friday might convince the Fed to ease up, but we’re anticipating that relief. If history and the immediate data proceed along the current path we should see a lot of price reductions in 2023.

For those who must sell, it’s an unfortunate time. There are ways to ameliorate the negatives, but it will probably still be negative. Those who are in a postion to purchase have the benefit of reduced prices, combined with the negative impact of higher interest rates. Generally speaking, very few are happy with a recession, though we have talking to a group of buyers who think pooling cash and buying as a consortium/collective is a masterful idea right now.

At a Glance

In addition to being relatively self explanatory, our At-a-Glance table is discussed throughout the above paragraphs. We won’t bore you with any more chatter about it, but we find it immensely useful as a quick reference. Some of our readers have even said they immediately go to the bottom of the article to see how much red ink there is. (Sorry. It is getting redder, but there are some delightful opportunities out there.)

Disclosures:

The areas are: Beach: comprises the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: comprises the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: comprises the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: comprises the cities of Torrance, Gardena and Lomita.

Landlords tend to have a lot of leeway in determining what kinds of pets their tenants can have. Many don’t allow pets at all, and those that do often have breed restrictions and/or additional fees. This has led many pet-owning low-income earners to give up their pets in order to secure housing. In order to combat this issue, California has decided to standardize some pet restrictions for low-income rentals.

What landlords will no longer be able to do is ban pets outright, prohibit certain breeds, impose pet weight limitations, or collect additional monthly fees for pets. Landlords can still require a security deposit for pet owners or ban specific individual pets that are vicious or dangerous. The new law also sets forth a list of some reasonable restrictions. These include policies regarding nuisance behavior, leashing, liability insurance, and number of pets. The latter should be based on the unit’s size and not personal factors.

The personal savings rate tends to hover around 8-10% during normal economic conditions, though it fluctuates constantly. These fluctuations tend to be inversely proportional to consumer confidence. If people think they can buy, they will. If they are hesitant, they will save their money instead. Across the last several decades, the record low was 2%, at the height of the Millennium Boom in 2005 when consumers felt they were in a stable economic position. By contrast, it hit a whopping 34% in April of 2020, just after pandemic stimulus payments began, most of which went directly to savings.

Now, the rate has dropped precipitously down to 3.8%. Unfortunately, that can’t be attributed to the inverse relationship with consumer confidence. Instead, the rate has dropped purely out of necessity. People aren’t saving money because they simply aren’t able to. The cost of living, proportional to wages, is incredibly high. Home and rent prices as well have accelerated at a rate far exceeding wage growth. The widening of the gap between cost of living increase and wage growth has been going on steadily for quite some time, but it’s more noticeable now with recent sharp increases in home and rent prices.

Despite all the uncertainty and chaos of fluctuating home prices, it’s possible to establish some trends. One such trend is the historical norm, which is the mean value of homes in a normal economy. It’s important to note that the historical norm is not a single value but rather a steadily increasing trendline, and is not a prediction itself, but can be used to form predictions. But it’s not increasing because home prices have been increasing — it’s actually based on homebuyer annual income, in other words, the annual earnings of people who are able and willing to purchase a home.

Boom and bust cycles affect the prices of homes, but not their long-term value according to the historical norm. This makes it significantly easier to tell when home prices seem too high or too low, and can be used to predict major economic events. The historical norm does suggest that home prices will continually increase, but what a 200% price-to-value ratio means is that prices are 200% of what they should be, even after accounting for this upward trend. It does not mean they have doubled from some prior value, rather from a hypothetical expected value. The last time the price-to-value ratio reached these numbers is in the mid-2000s, shortly before the crash of 2008-2009.

The Internal Revenue Service (IRS) has announced its new income tax brackets for 2023. There are some shifts designed to address the issue of bracket creep, which is when people move into a higher tax bracket despite no increase in income after accounting for inflation. The new tax brackets won’t completely solve the problem, and don’t address root causes of heavy inflation, but can provide some relief.

The IRS has done away with the 37% bracket entirely, so the most you’ll pay is 35%. For that, you’ll need a joint income of over $462,500, which is about 6.5 times the median household income in the US. Not only that, the minimum threshold has increased for every bracket, except the lowest 10% bracket which always has a minimum of $0.

Because of rising housing costs, even starter homes are becoming more and more inaccessible. Recent legislation aimed at streamlining processes for accessory dwelling units (ADUs) has turned ADUs into the new starter home. ADUs typically need to be permanent structures to qualify. Some cities and counties are trying to change that.

Mobile homes are often put into the category of tiny homes rather than ADUs. There is no restriction on whether or not tiny homes need to be permanent, or whether anything else needs to be on the lot. They just need to be 400 square feet or less. However, the definition of a tiny home varies, so they can be considered ADUs in some jurisdictions. And now, seven cities and three counties have decided that any tiny home that is on wheels is considered a permanent dwelling, and therefore can also qualify as an ADU. These seven cities are Fresno, San Luis Obispo, California City, Los Angeles, Richmond, San Diego, and San Jose. The three counties are Placer County, Humboldt County, and Santa Clara County.

There are a few different categories of costs involved in selling a house, some more expensive than others. Certain expenses may not apply to every sale, but you should still be aware of them in case they do come up. If you account for every possible situation in your budget, you may even end up with more profit than expected, since they aren’t likely to all occur in a single sale. These costs could come up at any time during the process, so be ready.

Before even deciding to sell, take a look at whether you need to repair or make any upgrades. Houses do sometimes sell as-is, but remodels can be more valuable than their cost, and major repairs may be necessary to sell for anything beyond the value of the bare plot of land. You may want to get a home inspection, though there’s a possibility you could get a buyer to pay for this later. Once your home is listed, you’ll want to help buyers feel welcomed. There could be costs involved with getting the home ready for open houses, though your agent may be responsible for some of these costs. When it comes time to complete the sale, there could be any number of costs, such as taxes, commissions, paying off mortgage, or other fees. And don’t forget about costs that occur after the sale. Many sellers are selling their primary residence and are also moving. That incurs moving expenses, which can get expensive for large, bulky furniture items or traveling long distances.

Some of the most significant closing costs are related to loans. During a cash sale, loans aren’t a factor, so you may be thinking closing costs are no longer relevant. However, there are certainly closing costs unrelated to loans. And the rules for who pays don’t change; it’s still negotiated between the buyer and seller.

The costs related to loans include origination fees, processing fees, and credit checks. These are all generally paid by the buyer, but you don’t have to worry about these at all for a cash sale. That doesn’t mean everything else is automatically paid by the seller. Closing costs also include earnest money, property inspections, appraisals, title insurance, and a title search. It may also include attorney’s fees, notary expenses, and some escrow fees, if applicable. Earnest money is always paid by the buyer, and in most cases, all or nearly all closing costs are. However, there’s always room to negotiate. Particularly in the case of a cash buyer, the buyer may have more negotiating power because the seller is less likely to want to lose a cash buyer.

The Rent Stabilization Ordinance (RSO) is a section of the municipal code for the City of Los Angeles and regulates a few different aspects of renting out properties. In addition to setting the maximum allowable rent increase per year, it also requires landlords to submit proper documentation to collect rent, provides just cause evictions, and provides relocation assistance for no-fault evictions. RSO doesn’t apply to all properties. The property must have been built prior to 10/1/1978, or 7/16/2007 if it’s a replacement under the Ellis Act. If you don’t know for sure, you can enter the property’s address at www.zimas.lacity.org. There will be an RSO field under the Housing tab, which will say Yes or No. You can also text “RSO” to 855-880-7368.

Note that RSO applies exclusively to the City of Los Angeles and does not apply to commercial properties. There are a couple easy ways to tell if your property is legally within the City of Los Angeles. If your water and power company is the Los Angeles Department of Water & Power (LADWP), you are in the City of Los Angeles. If it’s a different company, you are not. If your area is served by the Los Angeles Police Department (LAPD), you are in the City of Los Angeles. If you’re still unsure, you can look up the property at neighborhoodinfo.lacity.org. If your property is not found, it’s not in the City of Los Angeles. For properties not in the City of Los Angeles but in Los Angeles County, you can visit rent.lacounty.gov, email rent@dcba.lacounty.gov, or call 833-233-RENT.

Once you’ve confirmed that your property falls under RSO, your regulations are currently governed by Covid-19 protections, until February 1, 2024. Rent increases are not allowed until that date for RSO units, nor are retroactive rent increases allowed. If your tenant was negatively impacted by Covid-19, you also can’t charge interest or late fees on missed payments. After this date, the allowable increase is expected to be 7%, but this could change. In order to collect rent, you will need to complete a Rent Registry Form and pay your Annual Bill. The form is sent out in January of each year and is due by February 28th. Your Annual Bill consists of an RSO fee of $38.75 per unit and and a SCEP fee of $67.94 per unit. Part of this cost can be surcharged to your tenants, at a rate of $1.61 per month for the RSO fee and $2.83 per month for the SCEP fee. This comes out to 50% of the annual cost of each fee over 12 months.

Before you get a mortgage loan, ask yourself whether you want a qualified mortgage (QM) or non-qualified mortgage (Non-QM). You may be wondering under what circumstances you’d want your mortgage to not be qualified. Well, there are advantages and disadvantages to both. Non-QMs don’t conform to the regulations set forth by the Consumer Financial Protection Bureau (CFPB), but they’re actually entirely legal — the government simply can’t guarantee consumer protections.

So what are these protections, and why might you want to risk going without them? A QM loan cannot last longer than 30 years, cannot have prepayment penalties, cannot be a balloon loan, and should not have negative amortization. It requires a process for verifying several sources of information, including but not limited to bank statements and income. Because of this, it’s often more difficult to qualify for a QM loan. Therefore, someone who can’t qualify for a QM, such as many gig workers, may risk a non-QM loan. Investors, especially foreign investors, also frequently opt for non-QM loans that only require payments on interest. It’s also possible that you want to go for a longer-term loan, which would come with smaller payments, albeit a higher total amount paid once the loan is fully paid off. In any case, you probably want to ask a professional to explain the terms and risks of any loan you are considering taking, whether qualified or not.

Two more bills aimed at increasing multi-family construction go into effect July 1, 2023 after Governor Newsom signed them into law in September. These are AB 2011, called the Affordable Housing and High Road Jobs Act of 2022, and SB 6, the Middle Class Housing Act of 2022. Both laws sunset nine and a half years later, on January 1, 2033.

AB 2011 adds a secondary review pathway for some multi-family construction projects. If the project meets affordability standards and site criteria, the review will not take into account conditional use permits or environmental impact reports. The site must be primarily commercial, and unless it’s a commercial corridor, 100% of the units must be below market rate. Even if it is on a commercial corridor, 15% of the units must be below market rate. AB 2011 also includes provisions for fair pay and additional training for construction workers. SB 6 expands the types of buildings that can be constructed in areas zoned for office, retail or parking. These buildings may be residential if they meet certain other criteria, many of which are similar to the requirements set forth in AB 2011.

The State of California sets housing goals for every city in the state. Many cities, particularly more affluent ones, frequently decide to simply not meet these goals, as it doesn’t really benefit them to do so. Their only incentive to follow through has been what is termed the “builder’s remedy, ” which requires cities with no plan submitted, or that fail to meet their goal, to permit any and all housing as long as at least 20% of it is affordable housing.

This law has actually been in place for about a decade, but it hasn’t been easily enforceable. Recent changes have made it more enforceable, so now cities have to start thinking about it. Not all cities have the same deadline for submitting plans, but there are already 124 cities in Southern California that are out of compliance. Northern California has until January to submit plans.

Opendoor is an online real estate business based in Arizona that buys directly from sellers instead of going through the market process. While nothing about skipping the open market is illegal, the problem comes from Opendoor’s claim that its service saves sellers money. As it turns out, this claim is entirely false.

Opendoor claimed that those who use their service save money because they will be selling at market value with reduced transaction costs. There’s no evidence whatsoever that these claims are true. In fact, there is evidence that many sellers who go through Opendoor actually net thousands of dollars less than they would on the open market, despite cutting out the middleman. As such, the Federal Trade Commission voted unanimously, 4-0, to approve a final order against Opendoor. The final order requires Opendoor to pay $62 million in consumer redress, prohibits them from making deceptive, false, or unsubstantiated claims, and requires them to provide evidence of their claims.

Construction has had multiple ups and downs in recent years as a result of the pandemic and surrounding economic factors. Throughout it all, multi-family construction has actually done pretty well. In fact, it’s currently at its highest rate in the last fifty years in terms of total number of new multi-family constructions. Unfortunately, that doesn’t mean it’s high — construction has been in a slump for the past thirty years, and meanwhile the population has been increasing.

Los Angeles has it the worst of any US metro, underproducing by about 400,000 homes. This is despite the fact that it’s also one of the top metros for multi-family construction. In large part, this can be attributed to the fact that it is the second most populated metro in the US. But the real issue is restrictive zoning laws, which are only recently being changed in California. The vast majority of homes in the Los Angeles metro are single-family residences because that’s what the lot’s zoning allows.

After the pandemic forced many employees to work remotely, it was initially unclear how long the remote work trend would last. Some thought everyone would return to the office after the pandemic was over. Some saw that remote work was actually working surprisingly well, and expected fully remote jobs to rise in popularity. The latter has definitely happened, however, employers’ attempts at a gradual return to office work have caused another trend to emerge: the hybrid work model.

It turns out an office has benefits and so does remote work. And this is true regardless of an individual’s preference, if they had to choose just one. So why not get the best of both worlds, and just go into the office sometimes? This will be great for workers — though not for owners of office buildings. Those who held onto the office space they owned may have expected a full return to office work, which would result in a return to normalcy for the office building market. What is happening in reality is a gradual reduction in office space. Office space isn’t being eliminated completely, since it’s required for a hybrid work model. But companies won’t need nearly as much office space, and are already making plans to repurpose the space they already have.

One of the offerings of the Department of Veterans Affairs is mortgage loans. Of course, this is limited to current or past members of the US military. With this restriction comes a few significant benefits if you qualify. VA loans have perks for both low-income and high-income homebuyers.

If you have the money to buy a more expensive home as long as you can get a loan, VA loans may have you covered. There are jumbo loans available which can even exceed $1 million. This may be a good bet even if you are not currently a high-income earner, as long as you are purchasing investment property. This is because there is no minimum down payment for VA loans; you can borrow up to 100% of the home’s value. You don’t even need to worry about private mortgage insurance (PMI), which is required for conventional loans with a down payment under 20%, but not for VA loans regardless of your down payment amount. If your investments pay off, or you start earning more money, you can also pay off the loan faster. VA loans have no penalty for accelerating payments.

Insuring your home against natural disasters can save you quite a bit of money in the event such a disaster occurs. Frequency of different types of natural disasters varies by region. While this is also true of floods, floods can occur pretty much anywhere, so flood insurance may be worthwhile regardless of whether you are in a flood zone or not. So what do you need to know about flood insurance?

Flood insurance is not legally required. However, some mortgage lenders may require it, especially if the property is in a flood zone. As can be expected, flood insurance premiums are higher in flood zones, since there is more risk. That also means it can be relatively inexpensive if your area is not flood-prone. Since floods still occur at a significant rate in such areas, it’s probably a good deal even if the lender doesn’t require it. If you do get flood insurance, whether you chose to or your lender asked for it, make sure to compare plans. Premiums vary by company, and most companies have more than one insurance policy. Most policies cover damage to both the building and the contents of the home, but you should check to make sure. Some plans also include replacement expenses.

If you’re selling your home, or getting ready to do so, you may have thought about some of your prospective buyers’ potential questions and what the answers would be. Many of these probably relate to the home itself or the neighborhood, and can be expected questions. However, some not so uncommon buyer questions are decidedly more bizarre.

Perhaps not entirely unexpected is the question of whether or not there have been infestations, and it’s a common one. This would obviously be a major concern for a buyers, but be prepared for buyers to be overly concerned about certain unlikely infestations. Buyers may ask about pests that don’t even live in your area. Another very common question that may seem a bit silly to some people is whether or not someone has died in the home. Certain superstitious buyers may think this means the home could be haunted, which would be a major turn off. You may not even know yourself whether someone died there or not if it happened a long time ago, but buyers like this will still want to know. A less common death-related question, though perhaps one grounded more in observable reality, is whether anything was buried in the home’s yard. It’s not uncommon for people to bury their pets in the backyard, but buyers or their own pets may not want to unearth something like that.