In the US in general, the market has been slowing down. This is leading to a higher inventory — in March 2023, the number of homes for sale was 9% higher than in March 2022. But this isn’t the case in California. In fact, for-sale inventory in California’s largest metro areas was actually down 14% between the same two months. The difference is most stark in San Jose, where inventory dropped 32%.

However, this does have a couple of explanations. Available inventory is a raw number. It doesn’t take into account the number of buyers. Home sales volume is more indicative of the number of buyers, and that dropped significantly more than 14% between March 2022 and March 2023, by 33%. Thus, the ratio of homes available per buyer is actually higher than it was last year. In addition, California is still being affected by lower construction rates, while it has recovered in many other states. The major reason is pushback from local homeowners who don’t want additional construction in their neighborhood.

Are you planning to have kids soon and need ideas for names? The Social Security Administration (SSA) just released the list of the most popular baby names last year. If you want to be trendy, you can pick something from this list. Alternatively, you can take it as a list of names to avoid. Either way, it could be useful information, or could simply spark your creativity.

Liam and Olivia are the top choices for boys and girls respectively, and have been for several years now. Liam has been #1 for six years, and Olivia for four. The rest of the top ten list for boys are Noah, Oliver, James, Elijah, William, Henry, Lucas, Benjamin, and Theodore. For girls, they’re Emma, Charlotte, Amelia, Sophia, Isabella, Ava, Mia, Evelyn, and Luna. Of all twenty of these names, Luna is the only one that has never been in the top 10 before now.

The SSA also provided data on which names are growing fastest in popularity. None of these names are anywhere near the top 10, but they’re gaining the fastest. For boys, they’re Dutton, Kayce, Chosen, Khaza, and Eithan. For girls, they’re Wrenlee, Neriah, Arlet, Georgina, and Amiri.

Private Mortgage Insurance, or PMI, is a type of insurance that many lenders require for any mortgage with a down payment less than 20%. This is the main reason a minimum 20% down payment is so widely suggested. But if you aren’t able to put 20% down and are forced to take PMI, you needn’t worry too much. It’s also possible to get rid of existing PMI in certain circumstances.

One method that doesn’t require any specific action on your part is to simply wait until automatic termination of PMI, which occurs when you reach 22% equity and are current on your mortgage payments. However, it’s possible to request to terminate it earlier as long as your equity is at least 20%. There are a few ways to do this faster. The simplest option is to pay more than the required mortgage payment. This allows you to reach 20% equity faster while also reducing your PMI costs along the way. Another way you could potentially reduce payments to speed up equity gain is to refinance to a lower interest rate. Depending on your circumstances, this may or may not increase your total mortgage cost excluding PMI, but could eliminate PMI faster. There’s one more possibility: Reappraising your home. It’s possible that your home has accrued enough value that determining the new value of your home reveals that you actually do have at least 20% equity. If you do, you can request to remove PMI.

At the start of May, the Federal Housing Finance Agency (FHFA) modified the fee structure for loans guaranteed by Fannie Mae or Freddie Mac. The goal of the change was to increase the accessibility of homeownership to disadvantaged groups. In order to achieve this, fees were reduced for low-income borrowers, first-time homebuyers, and those with credit scores below 680.

However, reducing some fees meant needing to increase fees elsewhere. Fees increased significantly for middle income earners, those making larger down payments, cash-out refinance applicants, and second-home buyers. Critics argue this is a bad idea, since middle-income earners are more ready to buy and less risky to lend to. But despite the fee increases for middle-income earners, fees are still lower the higher your credit score — that hasn’t changed. If the changes push middle-income earners away, the effect is probably psychological, not necessarily financial.

Real estate is almost always a solid investment. The two major barriers are the high initial investment required and the necessity to manage the property. The former can’t really be fixed, but there are things you can do about the latter. While there is always the option to hire a property manager, this increases the investment required and can make the profits less attractive. Fortunately, there are some other options for real estate investment without being involved in management, which is termed passive real estate investment.

The other options are real estate investment trusts (REITs), real estate crowdfunding, private real estate funds, and exchange-traded funds (ETFs). In all of these cases, you are investing only a portion of the funds. This also reduces the barrier to entry, but at the cost of lower profits. REITs are trusts that own and manage income properties. Investors can purchase shares of REITs that pay dividends. Similar to REITs, ETFs are publicly traded; however, ETFs are traded on the stock market rather than purchased as shares of a company. Real estate crowdfunding and private real estate funds both involve a group of investors pooling money for an investment project. Crowdfunding gives each investor more choice about which projects they’re interested in, which is better for an investor who knows what they’re doing while still not putting the onus of management on them. Private real estate funds are the option for investors who just want to throw money at an investment and not be involved at all, as they are managed by professionals that choose the projects.

A bridge loan is a type of loan that uses equity in your current home to finance the purchase of a new home. Like nearly any loan, a bridge loan has interest and is paid off in installments. Unlike a traditional loan, though, the balance is paid off when your current home is sold. While you don’t technically need to sell your current home to pay off a bridge loan, it’s most useful in situations in which you want to both buy and sell.

Some seller-buyers will sell first, then use the sale proceeds to purchase a new home. However, this comes with potential uncertainties about how long you will be left without a home, especially if you make offers and aren’t successful. You may be staying in hotels or renting for longer than anticipated. Another option is to buy a home first using a traditional loan, then sell. If bridge loans weren’t a thing, there wouldn’t be anything inherently wrong with this. But they are a thing, and this is exactly the situation they’re designed for. While bridge loans do come with a higher interest rate than traditional loans, the length of the loan is typically much shorter. After all, most traditional loans are 15 or 30 years, and no one is going to be waiting that long for a sale to finalize. One caveat of bridge loans is that since they are based on the equity in your current home, if your equity is low, the loan amount will also be low.

This year has not been a good year for banks. City National Bank settled for millions early this year. In March, two major banks — Silicon Valley Bank (SVB) and Signature Bank — went bankrupt. These weren’t the only banks to fail, but they were the most well known. Now, First Republic, the largest bank to fail since Washington Mutual in 2008, has been added to list of failed banks. After First Republic failed, it was briefly taken under government control before being auctioned off. JPMorgan Chase, who had also purchased Washington Mutual when it failed, is the new owner of First Republic. The entire situation with First Republic has cost the Federal Deposit Insurance Corporation (FDIC) about $13 billion.

However, analysts and federal regulators emphasize that the banking crisis has calmed down, now. When SVB and Signature Bank failed, fears were warranted. But those failures sparked an inquiry into which banks were likely to fail, and First Republic was identified as a likely candidate early on. So, this wasn’t entirely unexpected, and regulators were able to act quickly. Additionally, the FDIC admits that SVB’s failure was partially their fault, as they had not been meticulous in their supervision. Analysts aren’t expecting any additional major bank failures in the near future.

If you want to make the most of a partial remodel, look no further than the kitchen. Unless no one in the family knows how to cook, people will spend quite a bit of time there. Kitchen remodels are a great investment if you know what’s trending. Right now, that means terrazzo floors, soapstone, and quartz. Marble and granite are old standbys that won’t generate additional interest. Additionally, more avid chefs are definitely looking for less common kitchen amenities. These include steam ovens, pizza ovens, and professional-grade appliances.

Getting all new furniture may not seem like a solid investment, but it certainly can be. You probably do want to if your current furniture is noticeably old or beaten up. And while you’re at it, you should choose the leading trend, which remains the modern farmhouse style. This style is typified by comfort, neutral color schemes, reclaimed materials, and vintage accessories, while at the same time using modern clean lines. Nearly all modern farmhouse style homes use reclaimed wood and have large, comfortable furniture. Many display rustic-looking, but still modern, wrought iron accents as well as antiques.

Having a shed somewhere on the property will also bring in more money. In addition, accessory dwelling units (ADUs) are still popular. Combining the two also works great. Buyers are paying more for properties with sheds converted into living space. Notably, this actually doesn’t translate to a quicker sale – for one reason or another, homes with sheds stay on the market longer, despite selling for more. If you do want to sell quickly, some inexpensive upgrades that will accomplish just that are doorbell cameras, heat pumps, and fenced backyards.

While construction rates have been low overall since the pandemic, construction rates can potentially vary significantly depending on the type of building you’re looking at. This can be the result of different levels of demand or zoning regulations. Recent zoning reforms have tried to push construction more towards multi-family residences, believing that zoning is the primary obstacle.

However, if recent numbers are any indicator, there simply isn’t much demand for multi-family residences. Construction starts on buildings with five or more units dropped by 6.7% in March. Permits for such buildings also fell sharply, by 24.3%. At the same time, construction of single-family residences (SFRs) increased by 2.7%, and SFR construction permits increased by 4.1%. Overall, construction starts dipped down 0.8% and permits decreased by 8.8%.

Even though this wasn’t the goal of the zoning reforms, not everyone sees this as a bad thing. SFRs being in higher demand could signal that more people are ready to buy as opposed to rent. However, since it’s not renters but potential landlords that would create demand for multi-family residences, it’s also possible that homeowners simply aren’t seeing the value in renting the units out, leaving potential tenants in the dust.

When comparing loans, buyers frequently only look at the interest rate. However, that’s not the entire story. There’s another number that lenders are required to supply, but that lendees rarely pay attention to. That number is the annual percentage rate, or APR. This shows an estimate of the actual percentage of the loan amount that you pay each installment period. It takes into account the interest rate, principal loan amount, and loan length, as well as any lending fees or closing costs.

Even though the APR gives you a better idea of how much you’re actually paying, the interest rate by itself is still important. This is because APR doesn’t take into account compound interest. If the interest rate is high, the amount you pay each installment period could increase significantly over time. This means a loan with a lower APR could potentially cost more over time if it has low lending fees. If two loans look very close and you’re concerned about exact numbers, you may also want to look into the APY, which is the annual percentage yield. This value does take into account compound interest. As such, it’s going to be slightly different each year, but knowing the APYs across multiple years will give you the best idea of how much you are actually paying.

When people think of a lien, what most people think of is a mortgage lien, whereby the mortgage lender retakes possession of a property in the event of missed mortgage payments. Most don’t realize that the lien is actually created as soon as you get the mortgage loan; it merely doesn’t have any effect unless the contract is breached. Lien is a rather general term that applies to any situation in which one party has the right to possess another’s property until a debt is paid or waived. One type of lien is a mechanic’s lien, which is the type a contractor can place to use your property as collateral for their work.

There are two broad categories of liens, consensual and nonconsensual. Mortgage liens are consensual because they are initiated by the property owner when they get a loan. On the other hand, mechanic’s liens are nonconsensual, and can’t be placed unless the contractor is legally able to. This means that while a mortgage loan is always in effect in case of a breach of contract, a mechanic’s lien that occurs as a result of the breach of contract can’t be placed until the breach occurs. Breach of contract is only one reason for a mechanic’s lien, though. It can also be placed in the event of nonpayment, unpaid property taxes or fees, deceptive practices by the property owner, or disputes over the work performed.

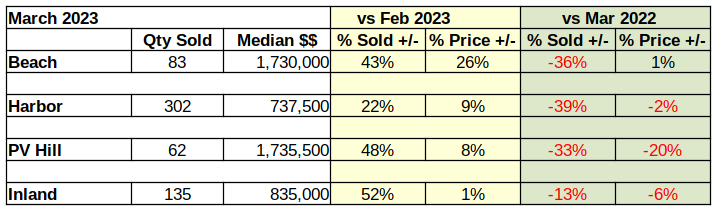

A glance at the table below confirms that year over year statistics are overwhelming the monthly numbers. Buyers were out there buying in March, and they were buying more than they did in February, which was up from January. That’s to be expected. We report actual numbers, as opposed to “seasonally adjusted,” so coming from the depths of winter into spring always increases real estate activity.

Because of that simple fact, the year over year statistics are far more important as an indicator of where the market may be headed. The big increase in March sales doesn’t offset how far down sales volume has gone since last year. Nor does it hint at the level to which median prices are taking a hit.

Compared to last year, sales volume is off by a third in nearly all areas of the Los Angeles South Bay. Median prices haven’t dropped nearly as large a percentage, but we can clearly see the direction. The Federal Reserve System (Fed) comment in the April “Beige Book” said it all: “Residential and commercial real estate activity fell, and lending activity declined substantially.”

Beach Cities Median Still Rising

As the over-all real estate market begins a dive into the depths of a Fed-induced recession, we find the Beach Cities as the only remaining local market with year-over-year positive median price growth. It’s not much. A mere 1% growth over March of 2022 is hardly an investment recommendation, especially with inflation running around 6%. And, the rest of the Los Angeles South Bay is already negative compared to this time last year.

This is the second time in 2023 buyers at the Beach have nudged the median price up while the rest of the residential market fell. January showed a 6% increase which collapsed February in a 17% free fall. February’s dismal numbers contributed to what looks like a good March in the month to month measurement.

Staying positive in March appears to be predominately the result of a single sale in Hermosa Beach. At nearly 5000 sq ft, with stunning ocean views, the property was bid up from its $5M dollar list price to just over $6M, closing with a cash offer in only 12 days. Without that transaction the Beach Cities marketplace would have stood at 0% growth.

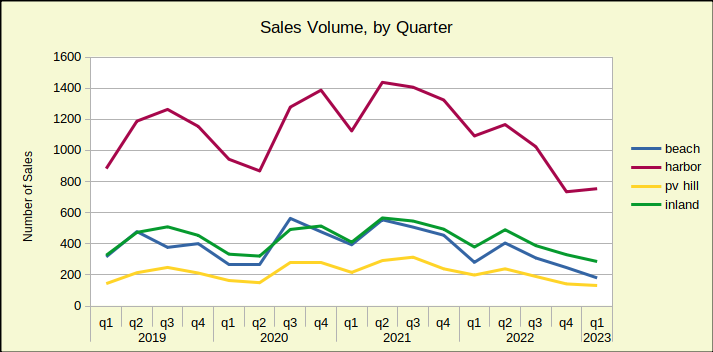

The big story at the Beach is the sales volume versus the most recent “normal” year of real estate business. The chart below shows the number of homes sold in each of the South Bay areas, with seasonal shifts.

Notice that 2019, the last normal year, begins low, with few sales in the winter months. Sales peak in quarter three, in the heat of summer, then decline back down to about where they started.

Compare that to what happened in 2022, when everything seemed to head down.

Only 83 homes were sold in March of this year, and only 181 homes sold across the first quarter of 2023. In 2019 the area averaged monthly sales of over 100 units; approximately 425 homes per quarter. That amounts to a 43% decline in the number of sales compared to pre-pandemic levels.

As this is written there are 152 homes available in the Beach Cities with an average of 62 days on market. Both, the level of inventory and the time on market are increasing daily. Those factors, especially working together, will cause price decreases. With a constantly increasing mortgage interest rate, there’s little doubt the valuation gains of the pandemic era will not hold up to the recession in the world of real estate.

Harbor Area Sales Volume Plummets 39%

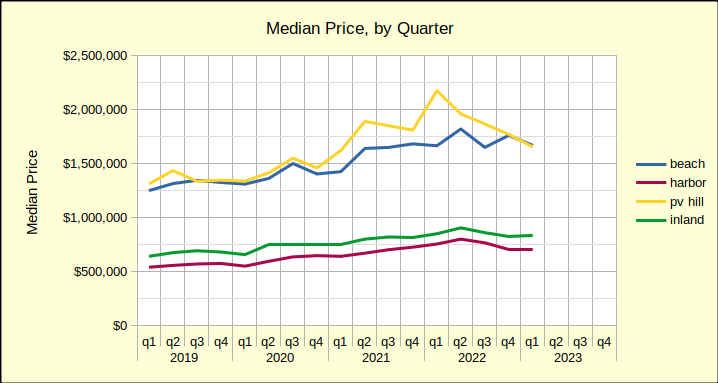

The Sales Volume, by Quarter chart above shows relatively synchronous movement across time by three of the four areas. The fourth area, the Harbor, floats at the top of the sales volume chart. Similarly, the Harbor area sinks to the bottom of the median price chart.

Homes in the Harbor area are typically what’s known as “entry level.” They are small homes, often condominiums, and are priced at the bottom of the scale. These are the homes newly wed couples buy, and the homes that house growing families. They are the type of properties occupied by most Angelenos, whether they be homeowners or tenants.

None of that explains the huge swings, though. What does is family economics—cash flow. When both prices and interest rates are low, the entry level market sings. When the cost of home ownership rises, this is the first area to fall and it usually falls the deepest. March sales across the Harbor dropped by 39% from March of 2022. At the same time median pricing at the Harbor dropped 2%–not nearly enough to offset interest rates that are running in the 6%-7% range. Until the mortgage interest rate goes down, or the asking price drops, or both, this market is going to be slow.

Inventory is currently 336 homes on the market, with time on the market averaging 60 days.

Median Down 20% for Homes on the PV Hill

Even more volatile than the Beach, homes on the Palos Verdes Peninsula dropped over a half million dollars in median price from the first quarter of 2022 to the first quarter of 2023. That steep yellow line on the chart below shows the downward direction of home prices in the area. Interestingly, the Beach Cities and the PV Hill declines have been almost exactly the same for the past 90 days.

As noted above, the Peninsula, with its large lots and relatively few homes, invariably shows a lot of volatility. The 20% drop in year over year median price is matched by a 33% drop in sales volume since March of 2022. Much of the median price increase seen last year resulted from a series of new construction sales. Those newly built homes came in at top dollar and helped elevate the median price nicely.

Builders are now anticipating a long, slow recession/recovery, so the PV market is not likely to see that benefit come back for a few years.

This newsletter focuses on residential, but it should be noted the Palos Verdes commercial marketplace has also taken a significant hit since the pandemic. Retail lease prices are at rock bottom and lots of space is available. It would not be surprising to see some of the older commercial space re-configured to meet residential needs. Such a transition could help the cities on the Hill meet their obligation to the State for additional residential construction to alleviate the housing shortage.

Inventory today shows 83 homes available, with an average time of 80 days on the market.

Stability Marks the Inland Area

The “family friendly” Inland Area is surrounded on three sides by the Beach Cities, PV Hill and the Harbor Area. It’s a quiet environment, usually without the drama and speculation found in the more upscale Beach and Hill areas. Anchored by Torrance, the market direction is normally the same as the rest of the South Bay, without the more radical ups and downs. March real estate activity reflected that nature in price and sales volume compared to March of last year.

The “Median Price by Quarter” chart above shows a year over year decrease of 6%, in keeping with annual results from the Hill and Harbor areas. The chart also shows a long, steady green line that doesn’t offer surprises, or dramatic movements in any direction. The current recession is expected to bring prices down somewhat, making the Inland area an excellent target for home buyers, or investors during the coming months.

Available as of this writing, are 130 homes. In keeping with the Inland image of slow and steady, the statistics still show only an average of 47 days on the market. Compare that to 80 on the Hill and 62 at the Beach. Buyers are more abundant here, as long as mortgage interest rates are affordable.

Footnotes

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Dylanfest is an 8-hour celebration of the music of Bob Dylan. Local favorites, Andy Hill and Renee Safier started it in 1991 and have been holding the event ever since. The show started with their band and a few friends doing an evening of songs by Bob Dylan, and it has grown to an 8-hour event with over 40 musicians performing over 60 Dylan songs. This year the festival will be held on Saturday, May 27th, from roughly noon until 8pm.

Food and drinks (including beer and wine) will be available on site during the event. Music is continuous with breaks only as entertainers move on and off the stage.

The band, Hard Rain, is the “house band”, and is joined by solo artists, full bands, and instrumentalists throughout the course of the day. The show is held at the Torrance Cultural Arts Center in the Torino Plaza. Bring a jacket for later. In case of rain, the event will go on, and we will move inside.

General Admission Tickets ($35-4/2-5/26; $40 at the Door). VIP tickets are $110 and come with some extra goodies (Entry fee, Event T-Shirt, Dylanfest Tote Bag, Dylanfest Mug, Post-Dylanfest VIP Party, VIP Hanging Tag). Kids ages 7-14 years are $10. Tickets at https://andyandrenee.com/tickets-tips-merch

Torino Plaza, Torrance Cultural Arts Center, 3300 Civic Center Drive, Torrance, CA 90503

The Grand Annex Music Hall is a rare neighborhood gem, a 150-seat cabaret venue run by Grand Vision in the heart of San Pedro’s thriving arts district. This May they are presenting three fabulous concerts of original music.

Small Glories – Saturday, May 13 / 8PM

Multi-award-winners Cara Luft and JD Edwards are taking the North American folk scene by storm. Cara Luft is an original member of the Canadian folk trio, The Wailin’ Jennys.

Wine Tasting 7PM led by sommelier JP Molinari.

Bella & Rudy – Friday, May 19 / 8PM

Born and raised in San Pedro, this incredibly talented duo is rapidly gaining attention for their acoustic and indie-inspired music. Hear their insightful originals and beloved covers.

Patrick Landeza & Sons – Saturday, May 20 / 8:30PM

A night of guitar, Hawaiian style featuring Two-time Nā Hōkū Hanohano Hawaiian Grammy Award winner and master slack key guitarist Patrick Landeza with PJ Landeza (bass guitar) and Justin Firmeza (steel guitar).

“Slack Key & Steel” Workshop at 7PM led by Patrick Landeza and Justin Firmeza.

The Grand Annex Music Hall is located at 434 W 6th Street, San Pedro Ca 90731.For more information about the performances and the venue go to their website https://grandvision.org/grand-annex/.

Grand Vision Foundation The Grand Annex Music Hall | Meet the Music | Friend’s Group to the Warner Grand Theatre 434 W. 6th St., San Pedro, CA 90731310.833.4813 | www.GrandVision.org

Real estate agents and experts will frequently declare that the market is either a seller’s market or a buyer’s market. There isn’t some esoteric industry secret formula, though. Figuring out whether it’s a buyer’s or seller’s market is actually fairly straightforward, as long as you have access to relevant data. There are three indicators of a seller’s market: low inventory, high demand, and low construction.

Of course, these statistics are interrelated. If construction has been consistently low, there will be fewer homes on the market. If inventory is low, buyers will be more competitive, driving up demand. But it’s actually low demand and high inventory that reduces construction rates in the first place, resulting in a cyclical effect. Moreover, each of them are affected differently by factors external to the cycle. So, in order for there to be a seller’s market, all three factors are probably true.

So what should you do if you find yourself under the conditions of a seller’s market? Well, if you’re a seller, everything is great — you’ll probably find a buyer, and be able to sell at a high price, as well. However, even if you’re a buyer, you can work the seller’s market to your advantage. Be aware that prices will be higher in a seller’s market, so a home that looks overpriced may actually be perfectly priced in a seller’s market. If you see something that fits the criteria you’re looking for, be ready to make an offer. It’s likely that multiple buyers are looking at the same thing you are. Make sure to get a pre-approval so that sellers know your offer is serious. In a high demand climate, sellers may get so many offers that they won’t even look at offers that don’t seem genuine.

For people who don’t necessarily have a lot of cash on hand but are willing to invest over longer periods, buying a home in need of repairs is often what they look to. This may be in to live in or to resell the home later, but in either case, you may need to finance the repairs, the purchase itself, or even both if you’re low on ready cash. Fortunately, there are loans that are designed specifically for this situation. One such loan is the FHA 203(k) rehab loan.

The FHA 203(k) rehab loan can be used to finance both a purchase and repairs simultaneously, preventing the need for multiple loans, credit usage, or a line of credit. This can definitely save you money in the long run, especially if you are able to qualify for a low interest rate. There are two types of FHA 203(k) rehab loans: a standard loan and a streamline loan. The standard loan is designed for long-term, larger projects, such as renovating entire rooms. This type has no limit on the portion of the loan used for repairs, unlike the streamline loan, which has a limit of $35,000. It’s quicker and easier to access funds from a streamline loan, which makes it more suitable for smaller projects, like installing an HVAC or repairing plumbing.

With how much discussions of real estate tend to pit buyers and sellers against each other, it’s easy to forget they’re often actually the same people. Many sellers are also buyers, either planning to buy to replace the home they’re selling, or already bought another home. This isn’t always the case, of course — it’s entirely possible that someone could have never purchased anything, inherited two homes, and sold one of them. But this isn’t most sellers. What this means is that market conditions that are generally considered to primarily affect buyers will also affect sellers.

Such as right now, where it appears that the high interest rates that are holding buyers back are also making sellers hesitate. The majority of homeowners now have an interest rate lower than the current rates, especially if they took advantage of ultra-low rates such as the rates during the pandemic. If these homeowners were to sell and buy a new home, they would be losing their low interest rate and gaining a high interest rate. For 82% of them, that may not be worth it. Over half of those considering selling right now are deciding to wait until interest rates drop.

Transitioning from renting to buying a home can be exciting. However, make sure not to get too excited too early before you’ve terminated the lease. It’s not at all uncommon for a renter to not want to deal with their landlord any longer than they have to, and simply leave. But that could actually be costing you money or leaving you open for a lawsuit.

Lease agreements will always have an early termination policy. It may look like ignoring the policy and ditching is just a way to skip the fees, but it’s actually not. You’re still on the hook for rent payments until the lease is actually terminated, and the early termination fee could be significantly lower. There may not even be a termination fee — the rules vary widely by region and by property manager. Don’t be afraid to talk to your landlord, either. They’re much more likely to be sympathetic to your situation if they’re aware of it. If you tell your landlord you’re terminating the lease early, the worst they can legally do is charge a termination fee.

There was a time that smaller homes and multi-family living were common in Long Beach. Over the decades, that has transitioned to condos and then to single-family residences. But in 2020, Long Beach municipal codes were revised, reducing the minimum square footage requirement to just 220 square feet. The original aim was probably not co-living, which wasn’t on the radar given that it occurred around the start of the pandemic. Nevertheless, builders now are seeing the opportunity to build apartment buildings consisting of small units with shared common area.

Derek Burnham is a former Long Beach city planner and now works at a development firm, and is excited about the idea. Burnham has already planned about 48 units, which are going to be roughly the same size as hotel rooms, around 350 to 500 square feet. The target audience for this project is people who want to be near jobs and transportation, but can’t afford the typical apartment or condo unit. But builders don’t yet know how receptive people will be to it — after all, the transition away from shared living towards single-family residences was cultural and not pragmatic. Because of this, the plans are flexible, allowing anything from private units to shared units to miniature family units.

Two measures went into effect this spring, Measure GS in Santa Monica on March 1st and Measure ULA in Los Angeles on April 1st, both of which enact an additional transfer tax on the sale of very expensive homes, dubbed the Mansion Tax. Measure GS affects properties sold at over $8 million and Measure ULA has two tiers, one affecting properties sold at over $5 million and another affecting properties sold at over $10 million.

Prior to these measures, the transfer tax in both cities was a small dollar value per $1000 of purchase price regardless of property value. Including county taxes, this value is $5.60 in Los Angeles, and Santa Monica has two tiers, one at $4.10 per $1000 and another at $7.10 per $1000. Measure GS added a third tier to the Santa Monica system, which is a significantly higher $56 per $1000 value for homes over $8 million. Los Angeles still only has one base value of $5.60 per $1000, but with an additional tax of 4% for homes between $5 million and $10 million, and 5.5% for homes over $10 million.