Covid-19 has kept the South Bay real estate market in disarray for a solid year now. So when we try to compare sales activity from 2020 to 2021 we find huge swings in the data that only tell us we’ve been living in a pandemic. We’re here to try to tease some intelligence out of that data and to guide our clients through buying and selling in these tempestuous times.

Month to Month

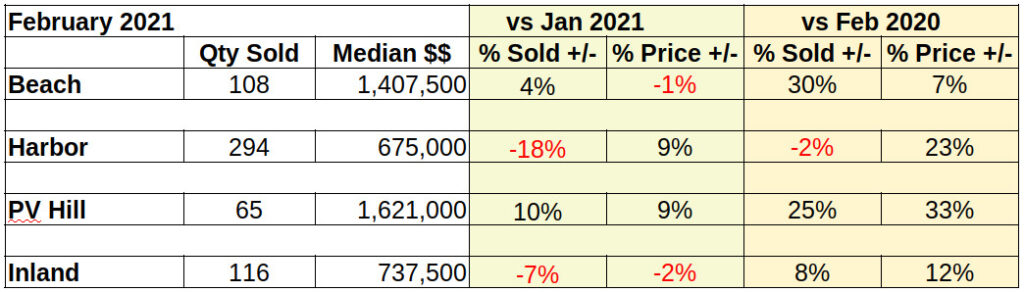

Let’s start by looking at the number of homes sold in the South Bay for February 2021. At the macro level sales volume is down -10% below January. Of course, that ignores the fact the number of sales last month (January) was down -30% compared to December, the prior month.

That’s the macro level. We start to see the range in sales volume when we step down to an area level. Looking more closely, the number of homes closing escrow in February versus January sales ranged from a decline of -18% in the Harbor area to an increase of 10% on the Palos Verdes peninsula. Comparing sales volume for the first two months of the year very much demonstrated the old maxim about the importance of location .

February against January for median price: Dollar-wise, the Beach dropped again, but by only 1% of the median price paid in January. However, note that this follows a 12% monthly drop in January from December 2020. From that scenario we can’t tell if prices are heading up, or still coming down. In other areas, the prices increased a robust 9% each for the Harbor and PV areas. Inland cities were down by -2%.

In total dollar sales, the South Bay was off by -1% from January activity. Once again, the detail was scattered with the high at 14% for Palos Verdes and the low -16% for the Harbor.

Compared to pre-Covid, these numbers are simply freakish.

Outrageously high! Compared to pre-Covid, these numbers are simply freakish. Back in 2019 any of the percentage statistics we look at on a monthly basis would have been in the range of +/-1%, occasionally a tad more. So, instead of Harbor area prices going up 9% in a month, we would normally be talking about .9%, one tenth the amount of increase.

Year to Year

Clearly the pent up demand from the past 12 months has had some impact. That, combined with the limited supply because so few people want to move during the pandemic. There’s always the question of what percentage of the buyers are home owners as opposed to investors. From speaking to other brokers in the area, we find a large number of the transactions are all cash.”

As always, one should note that ultra-local sales numbers are small in terms of mathematical models. As such, a single sale, high or low dollar, may make percentile statistics jump into outlier ranges. Similarly, a seasonal burst, or dearth of sales can seriously skew the numbers. Based on 25+ years of local real estate experience, I can assure you this is closer to a bubble than to a season burst.

Looking at it on a year over year basis doesn’t improve the image. Still the increases in every corner of South Bay, both in the number of sales and the median price increases, are beyond rational.

The year 2020 was very nearly the least predictable time in local real estate history. Seriously, what other time have we experienced massive unemployment and rising home prices simultaneously? All indications suggest 2021 will be a tad more conventional.

Home Values Grew in 2020

Despite “turmoil” being the watchword of 2020, the year produced some remarkable results in the Los Angeles South Bay. The Beach cities recorded a 28% increase in median price for December compared to December 2019. The cost of building didn’t rise at that rate, so clearly there was a heavy investment in anticipated value. As the chart below shows, Even with all the up and down motion, during the final half of the year buyers & investors were betting heavily that things were headed for calmer, more profitable waters.

That activity was spread across the spectrum of prices, as you can see tracing the community lines shown above.

Note that May reflects the sudden market contraction from the Covid announcement the beginning of March. This is a rare moment when the chart shows how much delay there is between signing a purchase agreement, and closing escrow. In April, 30 days after the announcement of a Covid pandemic, escrows were starting to drop off and were at or slightly down from March closings. By May, 60 days later, the number of closed sales had fallen by ~50K units in each of the four market areas. It took the classic 45 day escrow period to show that the pandemic took away nearly 30% of the business in the local real estate market.

How Many Sales? Where? Why?

While the Beach and the Harbor areas fought it out for the highest total sales dollars throughout the year, the Harbor clearly enjoyed the highest number of units sold every month as we see in the chart below. While the number of sales climbed across the South Bay, at the end of the year it was the Harbor with the largest increase in sales. Starting 2020 with 315 sales in January, the number climbed consistently through the year to a strong finish with 476 in December.

Two factors play into the volume of Harbor area sales. Part is the sheer number of homes in what is physically a larger area. The more interesting aspect of Harbor area sales increasing while the rest are relatively flat is the reason.

Homes in the Harbor cities are lowest priced in the South Bay by about $100K. Interest rates are currently running below 3%, and it’s in the lowest price points of the market where low interest rates are most effective. The low rates mean more buyers can afford to purchase at the same price point, on the same income stream. The larger number of buyers competing creates multiple offers and drives the price higher, which is a major factor pushing the market today. If we are to believe the Federal Reserve Bank, current interest rates are expected to remain historically low for the foreseeable future. The demand should hang around for just about as long.

Different Strokes for Different Folks

In the chart below, it’s interesting to note that the Inland and Harbor cities progress across the months with stability and only a slight change from beginning to end. At the same time, the Beach and PV cities gyrate through the year, sometimes with $200K jumps from one month to the next. One is tempted to say it’s the comparative size of the market area, but the Inland cities have very nearly the same number of homes as the Beach cities.

This difference is often thought of as reflecting the nature of the home buyer in these communities. Looking at stereotypes, it’s easy to imagine an owner in Torrance or Long Beach, for example, who buys in their early twenties and doesn’t move again until retirement–very stable. In the Beach and PV price ranges, where a home is often considered more as an investment vehicle than a residence, it’s easy to see where market forces can result in sudden changes to where one lives.

Moving From 2020 to 2021

The beginning of 2021 marked the end of some of the more impactful aspects of 2020. A ferocious political battle is ended, and a new Federal administration looks inclined to use “all the available tools” to bring our collapsed economy back on line quickly. Time will tell how much that helps us here in the South Bay.

The ever-changing story of the international pandemic may be coming to an end with the approval of multiple vaccines for Covid-19. Rumors still abound as to the actual efficacy of the drugs, and rates of infection are still climbing dramatically, especially here in Los Angeles county. It will end, whether sooner or later. The big question today is if the price increases we’ve seen as a result of bidding wars will sustain as the pandemic eases and government assistance is strengthened.

Looking at December activity, we see big increases in sales volume for Month over Month (M-M) and Year over Year (Y-Y) statistics. A continuance of this trend could make 2021 an exceptional year for real estate in the South Bay.

Median prices show a large variation from area to area, and importantly show a slowdown in the climbing prices. Y-Y price growth was strong in December, reflecting the high demand at current interest rates. However, M-M prices predominantly showed a reversal in price growth. Some of the slowdown could be seasonal, but if you’ve been reading our blog posts you already know there’s a growing backlog of homes poised on the edge of foreclosure. The only thing preventing a mass of short sale and foreclosure properties on the market is the forbearance rules put in place to prevent a sudden jump in homelessness during the pandemic.

Beach

December activity in Beach cities showed insane growth for M-M and Y-Y sales, both in the the number of sales, and especially in the prices of sold homes.

As if annual growth of 28% in median price wasn’t crazy enough, look at that monthly increase of 18.2%! Annualized, that would be over 114% growth! Statistics with this much reach can only be attributed to a profound belief that prices will continue to increase at a similar rate. Or, continue until the property can be flipped, that is.

Palos Verdes

Palos Verdes in December was almost a reverse image of the Beach cities. The explosive growth in PV came in the number of home sales which shot up 18%, bringing the annual number to a phenomenal 42% growth in volume for the year.

Median prices in PV showed modest increases, ending the year only slightly higher than the Fed’s target growth rate. The shift from positive growth to shrinkage in December hints at an overall market trending toward lower median sales prices.

A side note: Homes on the hill have not maintained the “investment quality” image of those on the Beach. PV was once considered the place to buy a home from a prestige angle and from an investment perspective. New money moving into the Beach cities has diminished that role in recent years. I predict a rebirth of property values in the Palos Verdes cities over the next few years, which will make having a home on the peninsula key in local business and society.

Inland

For the most part, Inland homes are family homes. They are the places with hoops in the driveway and lemonade stands at the sidewalk. Investment here is a long term concept.

So, when we see over 20% M-M growth in number of homes sold accompanied by nearly 30% Y-Y, we’re seeing market movement rather than shifts in investment strategy. As it is throughout South Bay, the cause of that movement appears to be the sub-3% interest rate which enlarged the entry level market segment. More buyers flooding in created bidding wars and drove sales and prices higher.

Compared to last December, median prices in the Inland cities were up 5.5%, peaking at $733K. That’s a good healthy increase, only slightly above the expected Consumer Price Index (CPI) numbers. Caution though–the M-M median is down 2.3%. It could be a momentary blip; a result of the holiday season, or the Covid surge. That year end drop may also indicate that the $750K median from November is the market ceiling.

Harbor

In addition to the largest home sales volume in the South Bay, the Harbor area boasts the most entry level homes. There’s a good deal of lifestyle overlap with the Inland cities, to be sure. The Harbor dramatically displays the same message we see across most of the South Bay. Everything was going strong until December, then buyers put the brakes on.

Today’s environment in the Harbor points the direction to the future. Sales here had a stronger growth than the Inland cities over the months leading up to December, and show a more pronounced decline in December.

Some of the slowdown will ultimately prove to be driven by the holiday, and some the election, and some by the pandemic. Even then, it’s hard to avoid the feeling that some of the decline is a recession held back by a thin wall of regulations temporarily preventing foreclosure and eviction.

We can certainly hope for better news from the new year, but as of the end of 2020 many of our indicators are calling for a deeper recession in coming months. It’s possible. Somewhere in the range of 20%-40% of homeowners are in forbearance now, and a roughly equivalent number of tenants are building up deferred rent payments. If adequate measures are taken to protect both sides of the debt, all of this will amount to footnote in history. Otherwise, it’ll be the second worldwide recession in this generation.

Quite a year! Soon we’ll have to do a wrap-up on 2020. But, for today it’s going to be November 2020 versus last year, (November 2019) and versus last month (September 2020).

Let’s start with the big numbers. Over all, total sales in the Los Angeles South Bay for November came in at just shy of $880M, 9% off from September. One could easily consider that drop a seasonal variation as we move into the cold months.

Compared to November 2019, total sales dollars for the combined areas of the South Bay were up 25%. Much of that is making up for sales that didn’t happen during the confusion of the first shutdown this year. Now that things are more stable, we’re seeing a lot more come on the market. Nearly everything coming on the market is selling, and at good prices.

Harbor

The star of the month is the Harbor area with a 42% year over year improvement in sales dollars. Units sold were up 26% Y-Y and median sales price was up 13%. This is a big boost for the San Pedro-Carson-Long Beach area. The increased action and the increased price, outpaced the rest of the South Bay by huge margins.

Generally speaking, the Harbor cities have entry level homes. Those are being bid up dramatically by buyers who newly qualify for purchase loans because mortgage interest rates are now down in the 2-3% range. I suspect there are more than a couple of investors are mixed in there, too.

Palos Verdes

The Palos Verdes peninsula presents an anomaly this month. November compared to October universally shows a seasonal decline in the 1-10% range, but PV dropped 27% in dollar volume. Looking deeper we see the M-M median sales price has dropped by 13%, while neighboring areas have remained within 1-2% of last month’s median price. Monthly sales volume also plummeted by 15% versus an average of 4% down for other areas.

Year over year values are all in line with the rest of the South Bay, by PV seems to be taking a beating from the pandemic.

Beaches

The Beach, by comparison to PV and the Harbor, had a boring November. Volume was down from October by 9% and median price off by 2%. Total dollar sales fell from October by 9%. The numbers are within seasonal expectations, but any time Beach prices fall off more than neighboring areas, it’s a cause of concern. The Beach tends to be a precursor to future changes in the South Bay.

Looking at 2020 over 2019, the number of sales was up 1% and median price was up 3%, leaving a tidy 11% increase in Y-Y total dollars sold. Despite the Covid-19 pandemic, those rock-bottom interest rates are making sales happen faster than last year.

Inland

Inland cities sales volume for November dropped off from last month by 3%. Median sales price declined a mere 1%, while total sales dollars were off by 3%. These are minor drops in light of seasonal impact, showing a strong market even as we go into the winter months.

Looking back to last year, the Torrance-Gardena-Lomita area showed more than respectable growth. Sales volume was up 12% over 2019. Median price was up 10%. Those increases created a total sales dollar increase of 25% above last year.

Not bad for being in a pandemic. Existence of a vaccine should relieve the fear keeping many people away from buying and selling during the coming months. The Federal Reserve Bank has indicated that interest rates will stay down for another 12-24 months. Everything points to a growing confidence over the winter and a booming market in the spring.

The High and the Low

The Los Angeles South Bay is a very diverse set of communities. To show you the breadth of that diversity, let’s take a quick look at the highest priced sale for November, versus the lowest priced sale.

On The Strand in Manhattan Beach a 6025 sq ft house on a double width lot of 6927sf sold for $17,750,000. The listing agent bills this property as a perfect opportunity to build a world class home of over 11,500sf of living space. The sold price per square foot of residence is $2,946.

On Ackerfield Ave in Long Beach a one bedroom one bathroom condo of 641sf sold for $205,000. Per the listing agent the home boasts a community pool and laundry facility, with one carport plus storage. The sold price represents a rate of $319 per square foot.

We’re looking at sales in the South Bay area of Los Angeles a little differently than usual this month. Typically we analyze the area as a single entity. This month we’ll divide the South Bay into four parts, allowing you to see a greater level of precision about those four areas.

Within each area the homes will be more similar, both in style and in pricing. We started by combining the four beach cities, El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach. Each of the cities has it’s own unique character, but they share many common traits. (If your home is in Hollywood Riviera, you can consider yourself one with the beach cities.)

The cities on the Palos Verdes Peninsula come together naturally, so we’ve combined Palos Verdes Estates, Rolling Hills Estates, Rolling Hills and Rancho Palos Verdes.

While Torrance does have it’s own beach, most of the city has more of an inland character, so we’ve combined it with Lomita and Gardena. One immediate benefit is the median prices are more representative of actual prices in those three communities.

Finally, we conjoined San Pedro, Long Beach, Harbor City, Wilmington and Carson, collecting the harbor area cities together.

Beach Cities

Prices have been trending up at a pretty rapid pace for most of the year, so it was a real surprise to find the median price in the Beach Cities had dropped by 6% from the September numbers. Last month the median price was $1.5M, while October only came in at $1.41M. Likewise, the number of sales dropped by a surprising 20%, from 209 sales in September, to 167 in October.

Year over year, beach prices increased by an impressive 17%, from $1.2M last October to $1.4M this October. Over the same time frame, sales volume went up by 45%, climbing from 115 units in October 2019, to 167 units in October of 2020.

On the Peninsula is where you really want to be in 2020. Prices and sales volume increased month to month and year to year. From last month to this month was on par with most of the South Bay, with the October median price of $1.68M coming in 5% above September’s median of $1.6M. The sales volume increase was a modest 3%, going from 95 units to 98.

The real treat for the PV cities is the 2020 over 2019 sales prices. October of last year showed a median price of $1.2M versus $1.68M this year. That’s a whopping 36% median price increase in 12 months. At the same time, October unit sales jumped 51% from 65 homes sold in 2019 to 98 sold in 2020.

Inland Cities

Going just a short distance away from the sandy shores of the beach, or from the bluffs of Palos Verdes, makes a huge difference in property prices. Like the coastal cities, the inland cities showed a 6% increase in prices from September to October. In contrast to the beach and the hill, the median price only went up $40K, from $719K to $759K. Like the beach cities, fewer inland homes were sold in October falling 11% from September. The drop wasn’t as great, going from 183 units in September to 163 in October of 2020.

October of 2020 versus October of 2019, the inland cities had median prices go up by 9%, from $600K to $656K. At the same time, the number of sales dropped by unit, from 164 homes sold, to 163 homes sold this October.

Median price in the harbor cities is typically lower than anywhere else in the South Bay. Similarly, price increases are slower. For example, while the rest of the areas saw 5-6% increases in month to month sales prices, the harbor came in at 3%. From September to October, the median increased from $636K to $656K. During the same time frame, the number of homes sold climbed 5%, from 435 to 457 units.

Comparing last October to this October, homes in the harbor area enjoyed a slightly more sustainable 9% rise in median price. The median for October 2019 was $600K compared to $656K this October. Sales volume jumped by 15%, from 397 units last year to 457 this year.

Why These Crazy Numbers?!

They are crazy, you know. There is no way prices can continue to climb at 5-6% per month. That’s more like what we would expect on a year over year increase.

October

2020

September

2020

Change

M-M

Med Sales $

Sales #

Med Sales $

Sales #

Med Sales $

Sales #

Beach

1,407,500

167

1,500,000

209

-6%

-2%

PV

1,682,750

98

1,600,000

95

+5%

+3%

Inland

759,000

163

719,000

183

+6%

-11%

Harbor

656,000

457

636,000

435

+3%

+5%

So Bay

820,000

885

799,500

922

+3%

-4%

It’s been a long time since we’ve seen Beach Cities prices decline. We’ll be watching November closely.

The answer lies in the interest rates. One the borrowing side, mortgage interest rates have been under 3% for some time now. With rates that low, many people who couldn’t afford to buy a home before, now qualify for a loan. Those who are still employed despite Covid-19 are buying homes if at all possible.

The demand created by that phenomenon has created a plethora of bidding wars. Homes with 20 offers on them are not uncommon. All those offers are pushing prices up at clearly unsustainable rates.

October

2020

October

2019

Change %

Y-Y

Med Sales $

Sales #

Med Sales $

Sales #

Med Sales $

Sales #

Beach

1,407,500

167

1,202,000

115

17%

45%

PV

1,682,750

98

1,233,000

65

36%

51%

Inland

759,000

163

680,000

164

12%

-1%

Harbor

656,000

457

600,000

397

9%

15%

So Bay

820,000

885

699,000

741

17%

19%

Adding to the entry level buyers who are driving the market at the low end, there is another group who have cash in the bank. Unfortunately, that cash is only earning 1%, or less. Those buyers are watching the price of real estate climb astronomically, and are hoping to cash in on a windfall profit. Some of them will.

The Crystal Ball

Watching the median price drop at the beach by 6% is a hint at what’s coming next. We can’t be sure when it will happen, but steeply escalating prices inevitably plummet in a subsequent correction. Current increases are reminiscent of the rapid run-up of prices in 2006-2007 which resulted in the Great Recession.

Further complicating matters, today we have government and consumer response to Covid-19 as a uncontrollable factor. The third quarter of 2020 looked really good compared to the second quarter, until we remember the coronavirus struck in March. Business during the second quarter was essentially nil.

We can’t forget the election. Fallout from the presidential election could push the economy in any one of several directions depending on who the President is, and the degree of polarization in the Federal government.

One would need a crystal ball to forecast this winter, but I predict a volatile ride for the real estate market.

It’s October 1, so it’s time to look at the changes in the local real estate market, both for the month and for the third quarter.

2020 has been a year for making and breaking records. Most of them have been records we truly didn’t want to even consider, like the number of pandemic deaths, and the number of unemployed. Until now, we had little reason to believe the real estate market might bring better news.

Through the first half of the year, the number of homes available on the market just kept climbing. At the same time, the number of homes selling remained stubbornly flat. Despite interest rates hovering just above zero, it seemed buyers had other things on their mind. Then in July the number of closed sales jumped 41%, while available inventory came up a tiny 7%.

Sales continued to climb in August and September, though nothing as dramatic as July. Overall, for the third quarter, unit sales were nearly double those of both, the first quarter of the year (+79%) and the second quarter (+76%).

For the first time this year, the inventory has dropped appreciably.

Comparing to last year, that huge spike in sales brought September in at 47% more sales than in September of 2019. On a quarter over quarter basis, Sales are up 23% over 2019. The red bars in the “Sold vs Available” chart above shows the climbing number of sales, with the blue bars showing the sudden drop of available inventory in September.

Not only were the number of sales climbing, but prices have continued to escalate year over year. September of 2020 showed median prices had increased 23% over September of 2019. Median prices rose 15% for the third quarter of 2020 versus the same time period in 2019.

Combined, the impact of the increased sales and increased prices brought the total dollar value of sales for September 2020 up 89% over that of September 2019. Quarter to quarter, the annual increase was 40%.

“South Bay residential sales for the third quarter of 2020 exceeded two billion dollars.”

How do we explain record sales and prices during a pandemic, with sky-high unemployment, and the threat of a recession coming from behind? It’ll be weeks before the pundits have sorted it all out. In the meantime, here are a couple of possible explanations.

Third quarter sales range from $285K to $10.5, so we know some of these have been entry level homes. Folks who have been priced out of the area, and because of the lower interest rate could suddenly qualify to purchase here, have jumped at it. Sales under $1M comprise 42% of the total.

At the opposite end, sales over $3M made up 9%. Once again, the interest rate makes it possible to leverage a mansion at a relatively affordable monthly payment. A lot has been said about the future worth of property compared to today’s dollar. Investing at a reduced interest rate usually contributes to a sizable profit at some future sale date.

In between, from $1M to $3M, we have 49% of the third quarter sales. That’s roughly the number of people we would expect to sell for one or another of the typical reasons people move. In fact it corresponds nicely with the rate of market activity for the first half of the year.

In summary, if the thought of making a move in the near future has crossed your mind, this may be the best moment to do so. Call and we’ll put together some numbers specific to your property and your situation. No problem–no obligation!