The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

Two months after reopening, the California economy is recovering unevenly, but recovering nonetheless. The housing market is a strong leader in the recovery process, with low interest rates contributing to a surge in activity after the last two months’ lull. The recovery will take time, though. The UCLA Anderson Forecast predicts a GDP decline of 42% in this quarter before easing back up 11% and then 7.6% in the next two quarters of this year. The total change from last year is expected to be a decline of 8.6%.

May was probably the trough for home sales, and they will pick up in the coming months. The extension of the foreclosure and eviction moratorium coupled with all-time low interest rates should allow buyers to regain their bearings quickly, and thus demand hasn’t suffered. Low supply and and a smaller than expected decrease in unemployment claims could point to a slower pace, but shouldn’t prevent recovery.

Call or email us if you want more information or are ready to buy or sell. Also, if you live in the South Bay or are interested in data about the area, stay tuned for a special South Bay update in early July.

Don Sabatini, a real estate agent in Willow Glen, CA, relates his true story of his client becoming the victim of a digital real estate scam. The COVID-19 outbreak meant that Sabatini had to conduct much of his business via email, though he and his client agreed to present the cashier’s check in person, while following social distancing guidelines. Despite this agreement, a scammer had been looking in on the email exchange. The client received several emails posing as the title agent, lender, and even Sabatini himself, increasingly threatening in tone. The scammer told the client that the offices will likely be closed, so she should simply wire the money. Feeling pressured by the barrage of threatening emails, she did so. The client and Sabatini realized she’d been scammed the next afternoon, but by then some of the money was irreparably lost. Fortunately, she was able to recover most of it, losing only $2000, and complete the transaction.

This story isn’t an isolated incident. The most recent data is from 2018, with the FBI estimating 11,300 people became victims of an online real estate scam in that year alone. It was an increase of 17% from 2017. Even without data from this year, you can imagine that with current pandemic increasing the rate of online real estate transactions, the rate of scam attempts is also increasing.

We are still conducting business, so don’t hesitate to call or email us if you are looking to buy or sell, but do be careful of scams.

According to a Gallup poll of favorite investment options, real estate remains at the top where it’s been since 2013, currently at 35%. It has been over 33% since 2016. After dropping by 6% since last year, the popularity of stocks and mutual funds is down to 21%, its lowest since 2012. While the percentage favoring savings accounts and CDs, gold, or bonds has increased slightly, their numbers remain low at 17%, 16%, and 8% respectively.

Even stockowners are now less likely to favor stocks as the best investment, but that doesn’t mean stocks are going away. Stock ownership is still stable at 55%, and hasn’t veered too much from that number since it started falling off during the Great Recession. It may not be the best option, but the number that think stock investment is a good option remains nearly identical to the number that think it’s a bad option.

If you’re interested in investing in real estate, we can help! Call or email us about buying or selling investment property.

As a result of the COVID-19 outbreak, the Federal Housing Finance Agency (FHFA), which regulates Fannie Mae and Freddie Mac (the Enterprises), had instituted a moratorium on foreclosures and evictions for Enterprise-backed single-family mortgages. The moratorium was scheduled to end on June 30th, but on June 17th, the FHFA announced that the date will be extended to August 31st. The FHFA plans to continue to monitor the situation and make further adjustments as needed.

The California Association of Realtors (CAR) released their May sales and price report on June 16th, and the numbers are showing a definite slowdown. Existing single family home sales totalled 238,740 in May, down 13.9% from April and down 41.4% from last May. The median home price was $588,070, a drop of 3% from April and 3.7% from last year. May also saw a year-to-date statewide home sale decrease of 12.9%. The Bay Area seems to have been hit the hardest. The impact of the COVID-19 pandemic was California home sales falling to the lowest level since the Great Depression.

The good news is that May was probably the worst of it. The market shows signs of recovering, especially buyer demand shooting up from record lows. One county, Del Norte, even reported a year-over-year increase in sales, and 31 reported a year-over-year increase in prices. Interest rates are also down from last year.

It’s no secret that California has a problem with rent prices and rental availability. Which solution to pick remains controversial. Rent control is the most immediate solution, but is a stopgap measure that can potentially do more harm than good over long periods. Building more affordable housing is a more permanent solution, but is a long-term plan with vocal opponents.

Currently, rent control is governed by the Costa-Hawkins Rental Housing Act, which prohibits rent control for housing units with a single title or that were first occupied on or after February 1, 1995. Proposition 10 appeared on the ballot just two years ago, seeking to repeal Costa-Hawkins and give more control to individual cities. The measure didn’t pass. Seeing the response to Prop 10, a new initiative, the Rental Affordability Act, decided to meet opponents halfway. Rather than entirely repeal Costa-Hawkins, this new measure seeks to amend it with a sliding timescale of 15 years, rather than a fixed year of 1995, to prevent the number of homes qualifying for rent control from remaining static.

Increasing the number of available rental units is a more appealing solution. It takes time and effort, though. California’s legislature has already adjusted laws regarding zoning, parking and landlord conduct, but it hasn’t been enough. Builders also need to do their part to make these plans a reality, and residents often oppose plans to build large, multi-family residences that could potentially decrease average home value in the area.

If you have any questions about rent control or finding a rental property or tenant, call or email us. We’d be happy to help!

As of June 10, while the California housing market has started to recover, it appears that recovery is slowing, not speeding up. California officially entered the recession in February, and we’ve come a long way since then, but there’s still plenty more to go.

Average home sales per day decreased in the second week of June following a modest increase in the first week, and the overall trend has been downward. Pending listings are still going up, but by less than 3% in 3 of the prior 4 weeks before June 10. New listings have been mostly flat. Two-thirds of buyers are expecting to get lower prices than they’re getting, and more of them are backing out because of financial considerations, despite high demand.

On the bright side, sellers are more optimistic. 40% of sellers believe it is a good time to sell, up from 29% in May, though still far below the pre-crisis level of 60% or more. Sellers recognize that while buyers may not have the funds they wanted, they’re still looking to buy. More buyers are applying for mortgages while mortgage forbearance has dropped from almost 1.1 million in mid-April to only 34 thousand in early June, and home showings are finally above the levels in 2019 and still going up.

Recovery has certainly slowed, but we’re going in the right direction. Now is a good time for both buyers and sellers. Call or email us and we’ll discuss business.

As I’m sure you already know, the lockdowns from COVID-19 have resulted in many workers needing to resort to working from home — potentially as many as 40%. This means that workers want a space in their home to work comfortably, something many homeowners and especially renters don’t have. Spaces not designed to be a home office can be inefficient or distracting, leading to lower productivity, so extra space for a home office is increasingly becoming a priority for buyers’ next purchases.

A survey by Zillow asked people working from home what their current configuration is and how it would affect future purchasing decisions. The survey found that only a third of those working from home have a dedicated home office space, and two-thirds needed to reconfigure existing rooms. Respondents’ top reasons to consider buying a new home were either a dedicated office space or just more space in general, letting other historically popular considerations like location and price fall by the wayside. Even after the pandemic ends, buyers are are looking to make their next purchase futureproof. Sellers and construction companies are also noticing the trend.

Are you also looking for dedicated office space or extra rooms for your next home? Does your own home fit the bill, and you want to sell? Whether you’re buying or selling, we can find a match for you. Call or email us!

According to a recent poll of readers of the Real Estate journal First Tuesday, the most optimistic recovery date from the current recession is late 2020, with 30% of respondents hopeful for a quick rebound. A quarter of respondents believe that recovery will be tied to a COVID-19 vaccine, which is predicted to arrive no earlier than mid-2021. 45% don’t expect recovery until 2022.

Benjamin Smith of First Tuesday agrees that a COVID-19 vaccine is important to recovery, but warns that there are other aspects at play. Real Estate as a business does depend heavily on in-person interactions, even though much of the work can certainly be done online or via email, and lockdowns have, without a doubt, slowed down business. Smith is careful to note, however, that the market was already on a downturn before COVID-19 hit, merely speeding up and exacerbating an impending recession. Two important factors in the downturn were falling inventory and insufficient construction.

While a vaccine can help open up agents, buyers, and sellers to safely meet up and discuss business, the underlying causes still need to be addressed, and people will need time and government intervention to recover their finances. This places recovery almost certainly later than mid-2021, and very likely further out. Fortunately, low interest rates mean buyer purchasing power will be relatively high once they regain their financial stability, meaning home prices aren’t likely to suffer as long as interest rates remain low.

Any time your credit report is reviewed, a credit inquiry is automatically added to your report. Your personal credit report lists all these inquiries for two years. There are two main types of credit inquiries: a hard inquiry, also called a hard pull, and a soft inquiry or soft pull. There are also personal credit inquiries.

Applying for credit or doing something that requires a credit check, such as applying for phone service, renting, or possibly taking a job, triggers a hard pull. Establishing business credit for the first time will do this. A hard inquiry reduces your credit score by up to five points, albeit usually for a short time. Sometimes multiple inquiries within a short period, such as looking for the best rates for auto insurance or a mortgage over 30 days, counts as only a single hard inquiry. Be cautious about multiple hard pulls in a short time, though. Lenders can see hard inquiries on your report and tend to interpret this behavior as high risk.

When you receive a pre-approved credit offer, chances are there was a soft inquiry on your credit report. Businesses use these to know your credit score for promotional information, as do banks and lenders to review your account to see if you qualify for new offers. These usually happen without your knowledge, though you can see them on your personal credit score. Fortunately, others cannot see them and they have no effect on your credit score. In addition, although applying for rent usually triggers a hard pull, renters can sometimes request a soft pull themselves to be sent to their landlord to avoid a hard pull. You can call us for more information about requesting a soft pull as a renter.

A personal credit inquiry is how you see all the information about your credit report. Your credit score and all inquiries, hard and soft, are visible to you at any time, and you can request your report for free once per 12 months at https://www.annualcreditreport.com/index.action. This is a good idea before applying for credit and also periodically to make sure it’s accurate and up to date. Visit the credit reporting agency’s website if you encounter an error.

As we recover from COVID-19, experts are saying it may benefit the rural real estate market. California Association of Realtors deputy chief economist Jordan Levine explains why. Levine notes that rural housing is generally more affordable, which may become one of the most important decision factors as people are recovering from temporary unemployment and business losses. In addition, more and more businesses are looking at a work-from-home model, which will enable employees to live away from urban commercial centers and not have to commute long distance to work.

Real estate personnel working in rural areas seem to agree. Cindy Young, president of Shasta Association of Realtors, predicted an increase in business since their first virtual meeting after the stay-at-home order. Real estate agent Sandy Dole, who works in Shasta County, didn’t experience any drop at all and is actually on pace to surpass last year.

Despite all this, the outbreak did mean California’s market overall experienced its worst month-to-month decline in over forty years. The crisis isn’t over, even in rural areas like Shasta County. The overall market is expected to be sluggish for the next couple of months, with no solid predictions beyond then. Market declines invariably mean lower prices, at least in some areas, while others perform better.

If you’re thinking of buying or selling, and are looking for a good price on a comfortable rural home, send us a note on our contact form, or give us a call. We are active agents throughout California. At the moment, we are seeing some very attractive properties in Ventura and San Diego counties.

The

Federal Reserve Bank (the Fed) moved to lower the federal funds rate

by a half-point to a range of 1% to 1.25% March 3 in response to the

“evolving risks” of the COVID-19 corona virus outbreak. The Fed

doesn’t directly impact housing loans, but they generally move in

tandem.

Mortgage

rates in the U.S. roughly track the yield on the 10-year Treasury

note which has been dropping as the corona virus epidemic expanded.

As the yield on the 10-year note drops, there is typically a drop in

mortgage interest rates.

Yesterday,

purchasers and refinance borrowers were looking at rates of about

3.7%. Today that’s about 3.5%. Some lenders are forecasting that

rates could drop as low as 3% before COVID-19 is controlled.

Some

analysts report that the stock market anticipates a least a

quarter-point rate cut at the Fed’s meeting in April.

Around

the world some other central banks have dropped rates as well. Since

consumer spending is a large measure of our economys, there is reason

to press for more cuts.

In

the words of the President, @realDonaldTrump, “The Federal Reserve

is cutting but … more easing and cutting!”

My favorite meal is a fresh salad, transformed to a main course with the addition of a grilled, or roasted, or sauteed piece of meat or seafood. This recipe is a more sophisticated version, with colorful and tasty endive taking the place of standard greens.

Salmon is a great go-to for this dish. If you’re not fond of the taste, or it isn’t readily available, there are several delicious options. Mahi-mahi or rockfish work well, as will chicken breast, or even scallops. The goal is the freshness of the salad combined with the hearty flavor of your meat, poultry or seafood.

Ingredients

3 heads red Belgian endive 3 heads Belgian endive 2 crisp and juicy apples Juice of 1/2 Meyer lemon 2 cups (2-3 oz.) of frisée and/or arugula greens, torn to bite-size 1/2 cup walnut halves or pieces, toasted 6 tbsp. white vinaigrette dressing (recipe below) 1 tsp. finely cut chives 4 fillets of a firm fish, e.g., salmon, mahi mahi, or rockfish

White vinaigrette dressing 1/4 cup white balsamic vinegar or fresh lemon juice 1 tbsp Dijon mustard 1/4 shallot, peeled and minced 2 tsp. honey (optional) 1 pinch finely chopped garlic 3/4 cup extra virgin olive oil Salt and pepper, to taste

Instructions

Salad Wash and dry endive and apples. Cut endives lengthwise into julienne strips. Slice apples and cut into julienne strips. (If made in advance, you can preserve the color of the apple with a spritz of lemon juice.) Tear the frisée and/or arugula greens into bite-size pieces. Set aside.

White balsamic vinaigrette dressing In a bowl or large measuring cup, whisk together all the vinaigrette ingredients and set aside.

Salmon: Heat olive oil in a sauté pan over medium-high heat. Score skin and season fish with salt and pepper. Place skin-side down in hot oil. Cook until skin is crispy, shaking pan to prevent fish from sticking. Turn fish over and continue cooking until medium rare. Remove and keep warm. (Alternatively, salmon may be grilled or baked.)

In a large bowl, combine endives, apples, greens, walnuts and vinaigrette, tossing gently. Season to taste and center on plate. Top the salad serving with one fillet each and sprinkle with chopped chives.

Usually this time of year I stick my neck out and make some forecasts about the local market in the coming year. What I’ve discovered is my quotes are boring by comparison to those made by the pundits. So, this year I decided to publish some of the more exciting projections by people who claim to know what’s going on.

Let’s set the stage by noting that the real estate market has been notoriously stable for the past few years. Stable, and on a very slight decline. The charts have shown volume and prices all within the normal range, with tiny losses increasing as time goes on. Several pundits have pointed to these stats and projected a recession on the horizon.

At the same time, as I point out in another article, this is a presidential election year. Can anyone remember an election year when the economy failed? It doesn’t happen very often. Let’s look at some quotes.

“Were we to have a recession, I’d argue housing would provide a cushion because the shortage of supply at the entry-level suggests builders could actually continue to build.”

Doug Duncan, Fannie Mae’s chief economist

Well now, I know quite a few builders and developers. But, I don’t know any who will start a project when prices start dropping. As a theory it sounds great, but I think it needs further study.

“While the housing crisis is still fresh on the minds of many, and was the catalyst of the Great Recession, the U.S. housing market has weathered all other recessions since 1980.”

Odeta Kushi, deputy chief economist at First American

Kushi says, “…since 1980.” So he had to look back 40 years to find good news?!?!

“Housing people are the most optimistic people, but it takes a lot of optimism to buy a house and tie up your income for 30 years.”

Nela Richardson, investment strategist at Edward Jones.

He’s right, at least as far as purchasers would go. Most tenants wouldn’t be very optimistic after renting for 30 years.

“The vast majority of housing economists project that mortgage rates will remain below 4% in 2020.”

Jacob Passy, personal-finance reporter for MarketWatch

Ha! Like we’re going to see the Fed argue with President Trump! He tweeted and they gave. It’s an election year!

“In the Los Angeles metropolitan area (which includes Orange County), the share of homes that sold for more than the listed price dropped from nearly 35 percent in 2018 to 28 percent in 2019.”

Elijah Chiland, reporter for Curbed, Los Angeles

There is a large difference between our little corner of the world here in 90277 and Los Angeles County in general, and it extends to the LA Metro and to California and to the nation as a whole. In 2019 only 17% of homes sold in 90277 sold for over asking. It is different here. Many brokers/agents have found that the statistics generated by state and national pundits are simply not applicable in the Beach Cities.

Here’s CAR betting on a positive market for the year! It’s an election year, and I can see this happening!

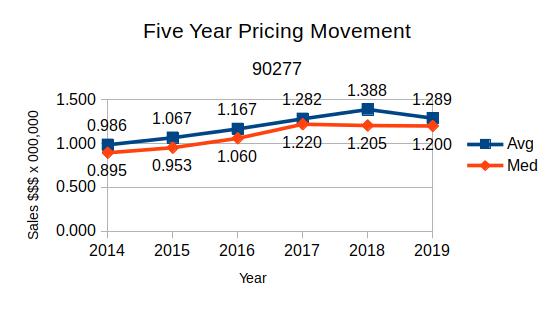

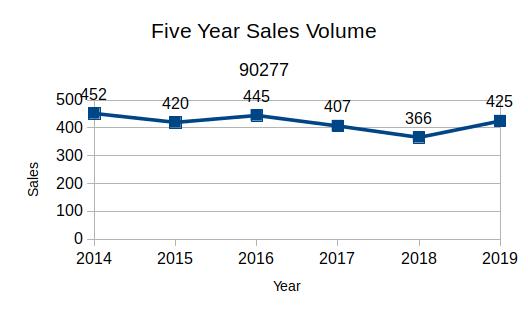

Last year saw property prices in 90277 drift down a little. Looking at a five year picture of shifting prices we see that from 2014 to 2018 there was a clear upward trajectory. By the end of 2019 the average price had dropped and the median price followed.

The final numbers for 2019 show the decline continuing and even growing. The median was only down .4%, but the average was down 7.1%, an even larger drop than projected for the fourth quarter of the year.

On a

more positive note, 2019 showed a 16% increase in sales volume for

90277.

The

downward shift in prices and upward trend in volume of sales are

consistent with the overall greater South Bay area. The upper end of

the local market is showing signs of having reached an apex in

prices, which has stimulated more listings and more sales.

At the same time, the moderate and lower priced neighborhoods have maintained price increases. Prices of lower priced homes are still climbing, but at a slower rate. Sales on the other hand, declined from 2018, or were unchanged.

So

what’s the outlook for 2020? To get an early look, we compared

January 2019 to January 2020. The statistics show both prices and

sales climbing. Sales for the month were 22% greater than January

last year. Average prices increased by 14.7%, while median prices

were up 5.9%.

All right, so things are looking pretty good, at least in the Beach Cities/South Bay area. But, let’s face it. This is an election year. The status of everything is subject to change in mere seconds, based on the latest poll/post/tweet hitting the internet. There’s not much we can do about the politics, but if you’re looking for a quick update on the real estate market, give us a call. Better yet, take out a free subscription to BeachChatter and we’ll send you a note to keep you abreast of the latest news. There should be a subscription form in the side column. And, we don’t sell your data!

This summer I saw an amazing example of how effective staging a vacant home can be. If you’re debating the merits of staging your property, whether currently on the market or still in planning, consider this example.

The property in question had been listed for lease in February at $3800 per month. It languished on the market for six months, dropping in price to $3650 in the meantime.

In August the seller listed with a different agent asking $3900 per month. It leased for $3750 in less than 30 days!

After sitting vacant for six months, at a loss of $22,500, what changed? Besides the new agent, the whole look of the property changed! The new listing agent brought in a professional stager, who added furniture, and hired a top-rated photographer who showcased the new decorating gorgeously.

The cost? At over $1000, was it steep, or cheap?. Compare that to the $22,500 lost while seeking a tenant and it comes out looking like a bargain.

This is only one example, and could easily be an anomaly. However, having watched this process repeat over and over, I’m firmly convinced that the cost of a highly professional stager, photographer and broker will be vastly offset by the increased purchase price and/or the rapidity of the sale.

After all, would you rather sell in 30 days, or six months? And would you prefer more money, or less?

First, how does one pronounce that impossible looking name? “Bœuf,” French for “beef,” sounds like a cross between “bif” and “buff.” Say it quickly and you’ll be close enough. “Bourguignon” is bu̇r-gēn-ˈyȯn. Just remember that the letters “g-n” are pronounced in French as though they were “n-y.”

But, you don’t need to pronounce it to love it. This is the dish Julia Child described as”…certainly one of the most delicious beef dishes concocted by man.” This version is considerably simpler than that in Julia’s landmark book, “Mastering the Art of French Cooking.”

Remember to use a good wine—a bad wine doesn’t improve with cooking.

This recipe can be adapted for a slow-cooker. Before loading up the pot, be sure to brown the ingredients as noted here. All ingredients can be added at the beginning except the mushrooms, which should be added at the end.

Ingredients

3 tablespoons olive oil

3 pounds boneless beef rump roast, cut into 1-inch pieces

12 ounces button mushrooms (trimmed), halved or quartered if large

Coarse salt and ground pepper

5 strips bacon, cut into 1/2-inch pieces

1 white onion, coarsely chopped

1 tablespoon tomato paste

2 tablespoons all-purpose flour

3 cups dry red wine

2 cups beef stock

2 bay leaves

4 garlic cloves, smashed and peeled

4 carrots, peeled and cut into 1-inch pieces

10 ounces pearl onions, peeled

1 tablespoon butter, cut into pieces

2 tablespoons fresh parsley, chopped (optional)

Process

Preheat oven to 350 degrees.

In a large Dutch oven or oven-safe pot with a tight fitting lid, heat 2 tablespoons oil over medium-high. Add mushrooms and pearl onions. Cook until browned, about 10 minutes, then set aside.

Season beef generously with salt and pepper and add to pot. In batches, brown beef on all sides, 2 to 3 minutes per batch (adding up to 1 tablespoon oil per batch, if needed); transfer to plate.

Pour off all but 1 tablespoon fat from pot. Add bacon and chopped onion. Cook over medium heat until brown, about 5 minutes.

Add tomato paste; cook, stirring, for about 30 seconds.

Add flour and cook, stirring, 30 seconds.

Return beef to pot; add wine, broth, bay leaf, and garlic. Bring to a boil, cover, and transfer pot to oven; cook 1 1/2 hours.

Add carrots and cook until meat is very tender, 1 to 1 1/2 hours more, adding mushrooms 15 minutes before end of cooking.

Stir butter into stew and serve topped with parsley.

Serve spooned over noodles,

rice or mashed potatoes, or even a baguette.

Adapted from Martha Stewart’ version of Julia Child’s quintessential recipe. Wine photo by Lefteris kallergis on Unsplash. Food photo by unknown.

We had a call recently asking

how California’s new statewide rent cap laws impact homeowners who

are supplementing their income by renting out an Accessory Dwelling

Unit (ADU). The primary concern was, “Is the owner forced to keep

a tenant or pay relocation if they decide to quit renting?”

The question stems from what is

called the “just cause requirements” of the new rent control law.

Our client was concerned about a decision to evict the current

tenant and allow a grandchild to occupy the ADU while attending

school locally. If “just cause” applied, it would require they

provide relocation assistance to their current tenant.

Renting a part of your home, whether a single room or an entire “guest cottage” may be excluded from the law.

To answer the question, we

reviewed the rent cap legislation with an eye to what terms would

control should a homeowner need to evict tenants from an ADU.

Applicability of “just cause”

relocation assistance, and the rent cap of 5% plus the local Consumer

Price Index (CPI) both rely on the same tests.

The first of those tests is the

type of property. Multi-family dwellings, i.e., everything from

apartment buildings down to duplexes are included in the scope of the

law. SFRs though, are excluded, and most importantly, an SFR with an

ADU qualifies as an SFR and may be excluded if the second test is

also met.

The second test relates to the

owner of the property. The following owner types are always included

within the scope of the law: —

A real estate investment trust, as defined in Section 856 of the

Internal Revenue Code. —

A corporation. —

A limited liability company in which at least one member is a

corporation.

The bottom line is that “mom and pop” operations do not fall under the rent cap or the just cause eviction sections of the new laws. There is a caveat! You must notify your tenants!

At the time the lease is signed, tenants should be provided written notice that the residential real property is exempt from this section using the following statement: “This property is not subject to the rent limits imposed by Section 1947.12 of the Civil Code and is not subject to the just cause requirements of Section 1946.2 of the Civil Code. This property meets the requirements of Sections 1947.12 (c)(5) and 1946.2 (e)(7) of the Civil Code and the owner is not any of the following: (1) a real estate investment trust, as defined by Section 856 of the Internal Revenue Code; (2) a corporation; or (3) a limited liability company in which at least one member is a corporation.”

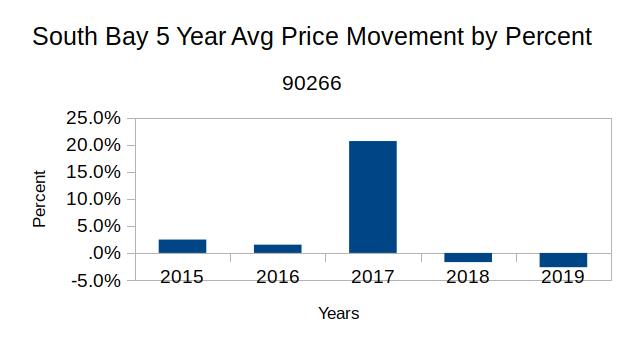

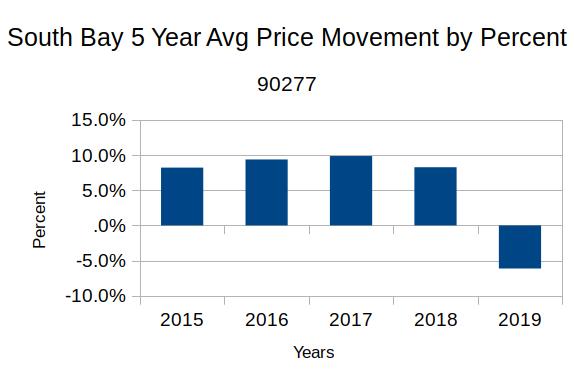

Here we wrap up 2019 and prepare for 2020, with a tumultuous election at hand and threats of an economic slowdown rearing in the local news. Our first thought is to look for a baseline from which to measure all the changes. So we did some research and assembled actual sales data from the last few years here in LA’s South Bay. Let’s walk, quickly, past some history.

Through 2015 nearly all real estate only became more expensive. Regardless of where you were in the country, or what kind of property you were considering, prices were only going one direction–up. Then, in 2016 the real estate world started changing. Our little corner of the the west coast is no exception. While some areas stand out as successes, others are showing signs of stress.

Torrance prices in the selected zip codes were varied, ranging from a low of 0% in 90505 for 2018 up to a high of 10.2% in 90503 for 2017. You read that correctly–Torrance prices have not gone negative yet! North Redondo Beach has also run positive every year, though 2019 looks like it will end with a mere .7% increase for the current year.

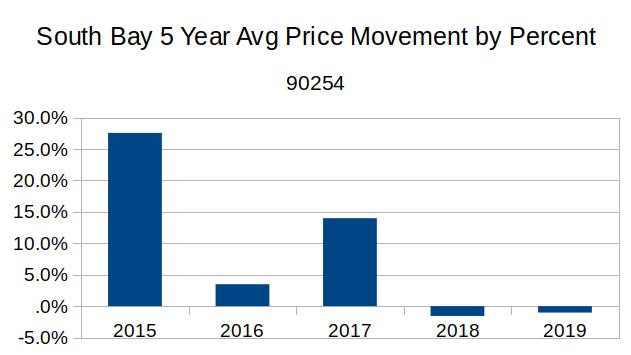

Hermosa Beach dropped a bit of value last year and is projected to lose again this year.

Manhattan Beach is a star performer, with average sales prices consistently above $2,000,000. Surprisingly, the city with the largest average increases is Hermosa Beach, with a price increase of 27.6% in 2015 and another huge price jump 0f 14% in 2017. Both cities declined in 2018 and 2019. Manhattan Beach was down by -1.7% and -2.6%, respectively. Hermosa Beach dropped by -1.6% and -1.0%, respectively.

Manhattan Beach showed exceptionally strong sales only in 2017, with 7 sales on The Strand. In 2018, prices declined slightly, and are projected to decline slightly in 2019.

While Manhattan and Hermosa were making one or two big jumps, south Redondo plugged away with annual increases between 8% and 10% until 2019. Unless something big happens in the final quarter of the year, 90277 will drop by about -6% this year.

After 4 years of increases, south Redondo Beach is slated to lose ~6% this year.

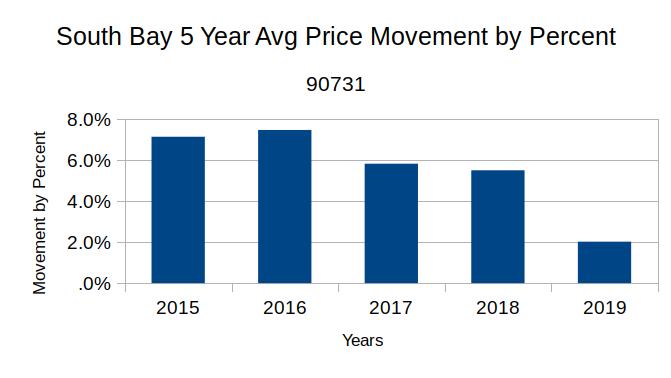

San Pedro has turned in a solidly positive set of numbers, too. The 90731 zip code is poised to show a 2.0% increase for 2019, down from a high of 7.5% in 2015. The 90732 zip code has slipped into negative territory with a forecast drop of -1.5% this year. Prior years have been over 8% increases, demonstrating the desirability of those harbor and ocean views.

San Pedro‘s 90731 has remained in positive increases to date.

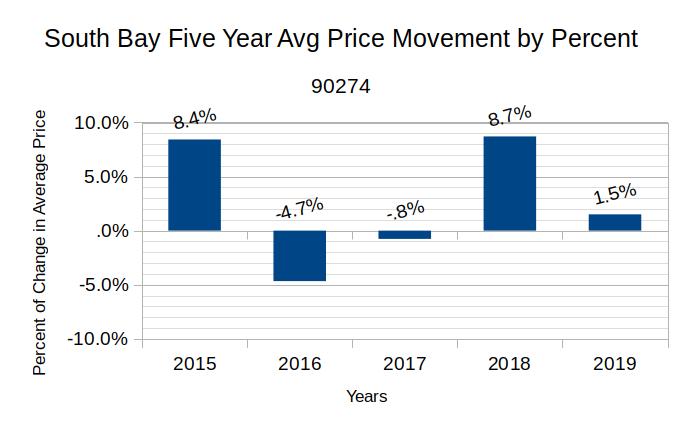

The Palos Verdes Peninsula has proven to be quite a “mixed bag” of ups and downs in average sales prices. Rancho Palos Verdes followed a predictable path of gradual increases up to 6.2% in 2018, with a projected decrease of -2.0% this year. The 90274 zip code was all over the map though. It started with an 8.4% increase in 2015, dropped into negative territory the following year with a -4.7%, then dropped another -.8% in 2017, only to jump up by 8.7% in 2018. We’re currently forecasting a 1.5% increase in those prices for 2019.

The ups and downs of 90274

If you live in the 90274 zip, and are interested in values, give us a call. We are working on a more detailed analysis of where and why distinct PV neighborhoods are seeing values shift on a differing pace. It’s very possible the age of homes in parts of the 90274 zip has pushed them into a “sweet spot” for upgrade or redevelopment. Alternatively, there could pockets not impacted by the economics of the greater community.

Check your city on the chart above. Are your property values still climbing? Or have they already hit the top and started back down?

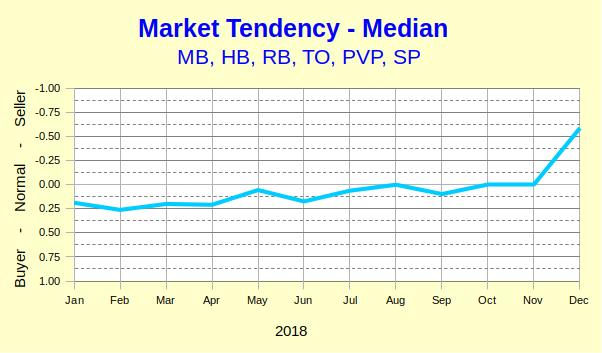

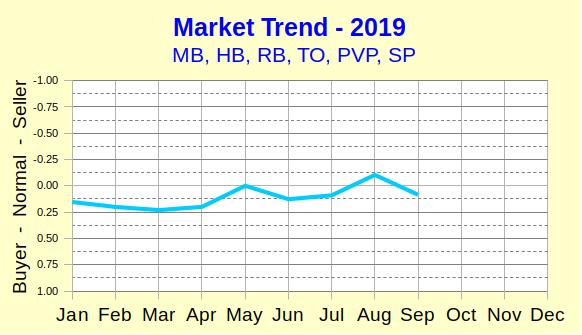

We’re here in the final quarter of 2019, looking back and comparing this year to 2018. It’s amazing how similar they have been so far in the year. Let’s take a look at the charts and numbers for the South Bay. Keep in mind these are very small movements, in a market that is about as normal and “middle of the road” as we’ve seen in a long time. I’ve shown the charts in large format, specifically so you can see the monthly movement.

Here we see the movement in listings and sales for the year of 2018. Notice the year starts off just below the center line, showing that overall activity is just barely leaning toward favoring buyers. Activity bumps up once in May, again in July and again a bit higher in August.

Note the chart shows a big jump in activity in December. These numbers are not seasonally adjusted, so these properties did actually move off the market. However, they didn’t sell. At the end of nearly every year the local market drops a big piece of the inventory. Listings that have been sitting for months without selling, and similar year-end cleanups, inflate the number of homes leaving the inventory.

Compared to last year, 2019 took off the same, running essentially flat until May, when there is a bump up that matches almost identically the May increase from 2018. Slowing down again in June and ramping up a bit for July then August repeats the activity from last year. As fall comes along, sales slow again for September, just like 2018.

It’s important to remember trend data is designed to point in a direction, as opposed to reporting history. I’ve removed the red trend line from these charts so you can more easily see the individual month changes. If you have questions, or would like to know specifics, don’t hesitate to call.