The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

Joseph G. Allen is an Assistant Professor of Public Health at Harvard and Director of their Healthy Buildings program. The New York Times has worked with him as well as several other professors to explain the process behind masks, to demonstrate that they do indeed work. In essence, particles get bounced around inside the fibers and trapped there. Interestingly, in the case of most masks, which are generally made of tightly woven cotton, the particles least likely to get trapped are medium size particles, as they’re big enough to be less influenced by surrounding air molecules yet small enough to not randomly make contact with the fibers as often. Large particles are most likely to get trapped, followed by small particles. Coronavirus particles are small and often get carried inside large particles, so they are in the two categories more likely to be caught by the fibers.

Los Angeles County and the City of Long Beach have been working with Project Homekey, a California state project designed to create more affordable housing by converting hotels into homeless housing. The project was started during the pandemic. The purchase of a Holiday Inn location in Long Beach had already been approved on October 13th, and on October 20th another location was approved in Los Angeles, the Motel 6 on 5665 E. Seventh St.

Long Beach is aiming to purchase another yet undisclosed location as well. The city has asked for up to $36 million from the Project Homekey fund, majority funding for which is from Coronavirus Aid Relief Funds. The city council isn’t expecting to be approved for the full amount, but is hoping to get at least $15 million to go toward acquisition and operating costs.

You’ve probably heard of a W-shaped recovery, even if you don’t know what it means. This refers to a false start in recovery, whereby the economy is improving in one sector, but doesn’t have the momentum to continue recovering, so it wobbles a bit. This has been what experts believed the current recovery would be like. Now, though, some people are wanting to call the recession and recovery K-shaped. What does this mean? It means that some sectors will recover and retain their momentum, while other sectors haven’t yet left the recession and continue downward. In other words, the recession has very clearly disproportionately affected various groups.

More specifically, this recession has had comparatively little impact on wealthy individuals. People with higher paying jobs are more likely to work in fields that can be done from home, so they haven’t been out of work during the pandemic. People who have the capital to invest in stocks as their primary means of income don’t have to worry so much about the pandemic, since stocks can’t get sick. They’ve actually been on an upward trend since before the lockdowns even began. Even those higher-income workers who did experience losses won’t have as much necessary expenditure proportional to income as those living paycheck to paycheck. This means that the recession has significantly widened the already large income inequality gap.

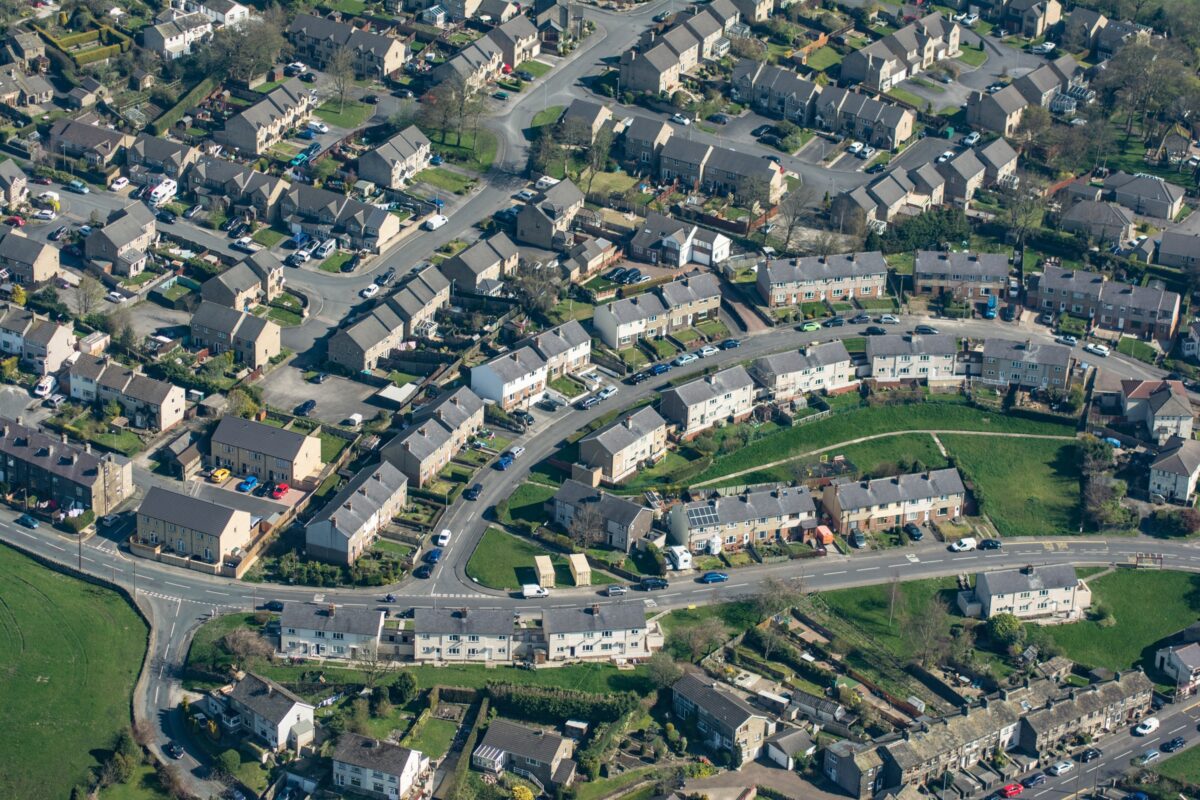

The trend of home offices is continuing to rise, and wasn’t just a result of the pandemic. In fact, it was already on the rise before the pandemic started. Some people already had spaces for a home office, others attempted to make do with what space they had. Now, builders and renovators are catching on and looking for ways to incorporate home offices into their plans.

The problem that designers are tackling is creating a space that works for everyone. Builders know that the space needs to be flexible, so they’re making flex spaces, usually on the main floor. But many people also want their home offices to be private. Sharing office space, even with someone who lives with you, can be loud or distracting. Combined with the fact that many homes don’t have a lot of space to work with, spaces for home offices must be large enough to do the work you need to do, yet small enough to be a separate space. It’s a difficult balance.

Some trends are already appearing in how COVID-19 has impacted real estate decisions. The economy is going to recover at some point, so some trends are likely to be temporary. However, there will certainly also be long-term impacts as experiencing the pandemic has altered people’s outlook on approaching real estate decisions, and even decisions made for the here and now could have lasting effects.

The less permanent changes include fiscal troubles at the state and local levels as revenue from commercial real estate taxes drops, retail vacancies, and a drop in urban desirability, expected to be temporary because of urban districts’ importance in certain industries once job recovery is underway. With this drop in urban desirability comes people wanting affordable suburban housing. This is being achieved now by many people moving to the Southern US, which already features low-cost suburban housing.

In the long term, however, we expect plenty of attention to enabling more affordable housing through government action and zoning changes, as well as programs to help traditionally low-income groups, such as minorities, get into the real estate game. These programs would be a direct response to COVID-19, but with lasting impacts. Another such change is greater attention to health and safety within the technological infrastructure of commercial buildings such as hotels and restaurants, which need not be eliminated post-pandemic. But there’s also a major change that was brought about by the pandemic, but addresses a different issue entirely, and that is office size. The prediction is that companies will want more, smaller offices, in more spread-out locations. This is because companies recognize both the feasibility of remote work and also the importance of office space for coworker cohesion and training. Their solution is small offices where a few coworkers can reliably meet up regardless of where they live while they aren’t working at home.

While confined to their homes during the pandemic, people have had plenty of time to take a good look at what their homes offer them — and what they don’t. Homeowners are reevaluating what’s important in a home purchase. Previously, many homebuyers were looking for a place close to everywhere they may want to go — likely in the city. Now, buyers don’t care too much about proximity to destinations if their own home offers them most everything they could want. That means single family residences with plenty of square footage and extra rooms.

Reshaping the home’s function is so important to people now that they don’t even want to wait until their next purchase. According to a survey by Porch.com, 78% of houseridden homeowners are increasingly looking at renovating their homes, commonly by adding a pool, home gym, or home office. A third are considering upgrading their home internet connection.

On October 19th, Compton Mayor Aja Brown announced a pilot program called the Compton Pledge. The Compton Pledge is a guarantee of monthly payments over a two-year period to some irregularly employed residents, immigrants, and formerly incarcerated persons, and is expected to reach 800 people. The exact amount of the monthly payments is not yet determined, but will be approximately a few hundred dollars.

The Compton Pledge is not the first guaranteed income program in California. Due to the success of the Stockton Economic Empowerment Demonstration, the Compton Pledge has received strong support. It currently has about $2.5 million in funding.

Free flu shots will be available at select LA County libraries while supplies last, and select Kaiser Permanente locations through at least November 14th. Insurance is not required and you do not need to be a Kaiser Permanente member. Flu shots are especially important for those with weakened immune systems or who regularly live with or care for someone who is at risk. This can be due to chronic conditions or age (both under 18 and over 65), but also remember that pregnancy can result in a temporarily weakened immune system.

[UPDATE] As of Oct 18, there is some additional guidance regarding holiday activities. Buying and carving of pumpkins is allowed, as long as the pumpkin patches follow safety guidelines. Some outside gatherings are now permitted, a change from the prior guidelines. These gatherings can have a maximum of 2 other households, can last no more than 2 hours, and require face coverings and social distancing across households. There are also new recommendations for Dia de los Muertos. These include displaying your altar outside or in a front window, utilizing virtual spaces such as email or social media, and limit cemetery visits to your own household with masks and social distancing.

LA County has issued its regulations regarding Halloween activities, if restrictions continue through October 31. Many traditional activities won’t be permitted, and others are allowed but not recommended. The activities not permitted include carnivals, festivals, haunted houses, live entertainment, gatherings, and parties with non-household members, whether or not it is outside. Of note, trick-or-treating is not listed as a non-permitted activity, but LA County Public Health does not recommend it.

The guidelines also provide a list of suggested activities that are safer. Drive-in movie theaters, outdoor dining, outdoor museums, and car parades are still allowed, subject to the normal regulations. Public Health Director Dr. Barbara Ferrer is hopeful that no more COVID-related regulations will be necessary by Thanksgiving or Christmas.

You may have heard the term MID in the context of purchasing a home or filing taxes. But what does this term mean? MID stands for mortgage interest deduction, and is a type of reduction in taxable income available to homeowners with a mortgage on their first or second home, or secured by their first or second home. When filing taxes, you can either take the standard deduction or itemize your expenditures. It’s common to simply take the standard deduction because many people aren’t sure how to itemize and may not even benefit from doing so. However, MID is one reason homeowners with a mortgage may want to itemize, since it is one of the itemizable deductions. The amount that the MID reduces your taxable income varies from 10% to 37% based on your homeowner’s tax bracket. It’s still possible that you would be better suited taking the standard deduction, depending on your expenditures and tax bracket.

By now you all should have received your ballots for the upcoming election. You may even have already voted, but if you haven’t and are struggling with understanding Prop 15, here’s an explanation.

Prop 15 aims to close a loophole created by Prop 13 that reduces property taxes for investors and businesses. Under Prop 13, property taxes are based on their purchase price rather than current market value, and caps increases at 2% per year. In California, property values increase at a rate higher than 2% per year, which means removing this limit and switching to assessments based on current market value would certainly increase property taxes. But if you’re struggling to pay property taxes on your home, have no fear — Prop 15 won’t remove the cap for everyone, only commercial and industrial properties. The measure also excludes properties zoned for commercial agriculture and small businesses whose properties are worth $3 million or less.

If Prop 15 passes, the changes will begin to be phased in in 2022, over three to four years. Reassessment for commercial and industrial properties would be required at least every three years. 40% of the estimated $6.5-11.5 billion in additional property tax revenue would go to schools and community colleges, with the remaining 60% going to cities, counties, and special districts.

What was previously known as San Pedro Public Market has been rebranded as West Harbor, and is expected to open in 2022 after delays due to COVID-19 that have pushed the date back from the previously expected 2021. The San Pedro Fish Market is definitely staying, and the U.S.S. Iowa may have a new location within West Harbor. Likely or confirmed new additions include AltaSea, Harbor Breeze Cruises, another Gladstone’s location, at least two other restaurants, a farmer’s market, and an amphitheater. Also in the works are plans for a brewery and beer garden, a barge, and possibly a beach. West Harbor is also getting a new nautical theme and color scheme.

The National Association of Home Builders (NAHB) now has data for Q2 of the year for its Housing Opportunity Index, which measures affordability of homes compared to median income. The US adjusted median income is currently $72,900. With these earnings, 59.6% of home sales were affordable in Q2 of 2020. This is down from 61.3% in Q1. This downward trend is largely expected, though, since the overall direction of movement has been down since NAHB introduced the Housing Opportunity Index in 2012, with occasional ups and downs. At its inception, the value was 78.8%.

What causes affordability to go down? The index looks at three factors: mortgage interest rates, median incomes, and home prices. Since interest rates are at historic lows right now, they’re not the culprit for falling affordability. Home prices are still rising more quickly than the median income, despite the rate of increase for home prices dropping in the last several years. Not to mention much of the recent boost to median income is not actually a result of increased wages, but rather job losses — since unemployed persons are not included in the median income figure, low-wage earners losing their jobs due to the recession and COVID-19 has artificially inflated the median income.

Residential construction of both single-family residences (SFRs) and multi-family housing has been on a downturn since the most recent peak in 2018. SFR construction in particular is a long way down from the 2005 numbers when they started to nosedive, while multi-family housing construction has been relatively stable since the 1980s, albeit much lower than it should be.

The number of SFR starts in 2020 is projected to be about 53,000, 10% lower than in 2019 and less than a third of the 2005 number of 154,700. Multi-family housing construction has rebounded from the 2009 trough, but at an expected 48,000, is still down 5% from last year. For multi-family housing, the 50,300 value in 2005 was actually lower than the 2017 and 2018 peak of 53,800 both years.

As with any recession, at some point the direction of prices is going to change. In most cases, real estate speculators purchase at low prices so they can later sell at a higher price. Currently, speculators are most likely to be sellers, not buyers, since home prices are already high, and are expected to decrease in 2021 as sales volume continues to drop. Once prices start dropping, as buyers are waiting for prices to bottom out, sellers are looking to sell as quickly as possible to get the most money. With more seller willingness, buyer speculators are also coming in 2021.

Given the current high buyer demand, a sudden increase in seller willingness is going to look like the beginning of a recovery. Don’t be fooled by this. Speculators are generally people who can afford to be wrong. This increase in activity is not going to be a result of a stabilizing economy, but of opportunists who were largely unaffected by the recession wanting quick sales. Speculators generally only constitute 20% of buyers. For an actual recovery, the rest of the populace needs a stable income. That means job recovery, which isn’t expected until 2023.

A 2015 Department of Housing and Urban Development (HUD) rule, called Affirmatively Further Fair Housing (AFFH), had presented guidelines for what constitutes barriers to fair housing and required recipients of HUD funding to reduce or eliminate these barriers. This rule was deemed to be an overstep of federal bounds, as matters of this nature should be determined at a local level. The HUD’s new rule, called Preserving Community and Neighborhood Choice, still requires funding recipients to affirm that they’ve furthered fair housing, but no longer offers any guidelines for what that means.

Of course, this is no longer federal overreach, but that’s because it doesn’t actually do anything. Barring any state or local laws, the definition of fair housing is now entirely up to the individual receiving the funds. With no need to report any plans or data, the recipient can simply affirm that they did further fair housing, without needing to change anything or provide any proof. In essence, the HUD has simply eliminated the AFFH while pretending it was a partial rollback.

The traditional dinner salad is most often an unexciting food. Ditch that classic iceberg lettuce studded with cherry tomatoes in favor of this taste treat. These flavors will burst in your mouth from the first bite to the last. Whether you serve it in the heat of summer, or as a year-round starter, this dish is a treat for the eyes and the taste buds.

Serves 6

Ingredients

2 (6-oz.) bags baby spinach 1 (16-oz.) container strawberries, quartered 1 (4-oz.) package crumbled blue cheese, feta cheese, or goat cheese 1/4 medium red onion, thinly sliced 1/2 cup sliced toasted almonds or halved candied pecans Balsamic vinaigrette (recipe follows or use bottled vinaigrette)*

Directions

Toss all the salad ingredients together and drizzle with dressing.

*Easy Balsamic Vinaigrette

1/4 cup balsamic vinegar 1 tsp prepared mustard 1/2 tsp salt 1/2 tsp freshly ground black pepper 3/4 cup olive oil

Directions

Place the vinegar and seasonings in a bowl and whisk to combine. Slowly add the olive oil and whisk until the dressing is emulsified.

It’s October 1, so it’s time to look at the changes in the local real estate market, both for the month and for the third quarter.

2020 has been a year for making and breaking records. Most of them have been records we truly didn’t want to even consider, like the number of pandemic deaths, and the number of unemployed. Until now, we had little reason to believe the real estate market might bring better news.

Through the first half of the year, the number of homes available on the market just kept climbing. At the same time, the number of homes selling remained stubbornly flat. Despite interest rates hovering just above zero, it seemed buyers had other things on their mind. Then in July the number of closed sales jumped 41%, while available inventory came up a tiny 7%.

Sales continued to climb in August and September, though nothing as dramatic as July. Overall, for the third quarter, unit sales were nearly double those of both, the first quarter of the year (+79%) and the second quarter (+76%).

For the first time this year, the inventory has dropped appreciably.

Comparing to last year, that huge spike in sales brought September in at 47% more sales than in September of 2019. On a quarter over quarter basis, Sales are up 23% over 2019. The red bars in the “Sold vs Available” chart above shows the climbing number of sales, with the blue bars showing the sudden drop of available inventory in September.

Not only were the number of sales climbing, but prices have continued to escalate year over year. September of 2020 showed median prices had increased 23% over September of 2019. Median prices rose 15% for the third quarter of 2020 versus the same time period in 2019.

Combined, the impact of the increased sales and increased prices brought the total dollar value of sales for September 2020 up 89% over that of September 2019. Quarter to quarter, the annual increase was 40%.

“South Bay residential sales for the third quarter of 2020 exceeded two billion dollars.”

How do we explain record sales and prices during a pandemic, with sky-high unemployment, and the threat of a recession coming from behind? It’ll be weeks before the pundits have sorted it all out. In the meantime, here are a couple of possible explanations.

Third quarter sales range from $285K to $10.5, so we know some of these have been entry level homes. Folks who have been priced out of the area, and because of the lower interest rate could suddenly qualify to purchase here, have jumped at it. Sales under $1M comprise 42% of the total.

At the opposite end, sales over $3M made up 9%. Once again, the interest rate makes it possible to leverage a mansion at a relatively affordable monthly payment. A lot has been said about the future worth of property compared to today’s dollar. Investing at a reduced interest rate usually contributes to a sizable profit at some future sale date.

In between, from $1M to $3M, we have 49% of the third quarter sales. That’s roughly the number of people we would expect to sell for one or another of the typical reasons people move. In fact it corresponds nicely with the rate of market activity for the first half of the year.

In summary, if the thought of making a move in the near future has crossed your mind, this may be the best moment to do so. Call and we’ll put together some numbers specific to your property and your situation. No problem–no obligation!

California, in partnership with Long Beach and LA County, has begun the process for Project Homekey, a project to convert two hotel properties into homeless properties. One will be a 100 unit project and the other approximately 50 units. While it’s not yet announced which properties have been chosen, the decision has already been made, and these criteria narrow it down significantly. Only one property fits for the 100 unit structure — the Best Western of Long Beach. There are a few different options for the 50 unit project.

The converted units aren’t going to be ready immediately. The properties have not yet been purchased, and the deadline to do so is December 30, so it could be up to two months before the conversion even begins. The contract for funding the conversion process is expected to last several years, though the conversion could already be complete before the contract expires.

The port of Long Beach will open its eagerly awaited new bridge on Oct. 5 after seven years of construction. The long wait was due in part to COVID-19 restrictions and was also intentionally delayed for careful attention to earthquake safety. The bridge currently has no name, but will be replacing the Gerald Desmond Bridge.

This new bridge will have three lanes in each direction across its two mile length to reduce traffic congestion. It will have connections to the 710 Freeway, Terminal Island, and Downtown Long Beach. In addition, larger container ships will be able to pass under the bridge, as it is taller than the Gerald Desmond Bridge.

![[UPDATED] What Will Halloween Look Like During COVID-19?](https://www.beachchatter.com/wp-content/uploads/2020/09/jackolantern.jpg)