The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

California’s housing market saw multiple shifts during 2020 as different sectors reacted differently and regulations changed with the times. When 2020 began, we already had high home prices and a construction deficit. The lockdowns of the pandemic propelled an economic recession that was already in the making, causing it to arrive faster than expected. Normally recessions cause a drop in prices, but the circumstances of this recession were forced, and therefore not necessarily subject to the same natural tendencies.

In the beginning of the lockdowns, real estate agents were not able to meet with clients or show property, causing the market to grind to a sudden halt. As the year progressed, regulations loosened somewhat, allowing showings under safe conditions. That prompted a spike in demand, as people who were itching to buy, especially with low mortgage rates, were finally able to start looking again. However, that did nothing to change available inventory. Inventory is low as a result of lack of construction, and what little construction there was being halted by lockdowns. In addition, most of the construction being done was for higher-end single-family residences, even as many prospective buyers were losing income due to the pandemic. With high demand and low inventory, prices simply continued to go up.

The market itself isn’t the only thing that changed, though. Prospective buyers are no longer looking for the same types of properties they wanted before 2020. If people are going to spend more time at home, they want the type of home that they’ll be happy living in. Move-in ready. Plenty of space. Home offices. Room versatility. It even extends to the outdoor amenities — houses with pools and outdoor living space are selling quickly, since people are able to be outside without leaving the confines of their property.

“Exercise more” is a common New Year’s resolution, but few are able to keep to it for long. They may go to the gym for a couple months, but the lack of time or energy makes it difficult. The simplest solution is actually something that many people are planning to do already as a result of the pandemic forcing them to stay at home: Build a home gym.

If you don’t know where to start, here are some tips for you. The first step is to designate the space where you want your home gym to be. Dedicating an entire room allows you to work out without distractions, but that may not be possible for everyone. A couple alternatives are a section of your garage or basement. Next, lay down some rubberized flooring, and make sure there are mirrors to check your form as you work out. Now for the actual equipment: at least one cardio machine, weights and a bench, and a yoga mat for post-exercise stretches. There are many types of cardio machines variously suited to different types of exercise. Common ones include treadmills, elliptical machines, stair steppers, and stationary bikes, or, if you don’t have the budget for expensive machines, simply a jump rope will do just fine.

There are many factors leading to the current housing market being a rough time for first-time homebuyers. This group is already at a disadvantage from the outset, not having the ability to sell their existing home to help pay for a new one, and frequently already saddled with rent payments. In addition, first-time homebuyers tend to be lower income workers. This is further exacerbated by high home prices, low rates of construction for affordable housing, and an ongoing pandemic.

Home prices have been high for quite some time, and are continuing to climb. In a volatile market, sellers want to be sure to get as high of a return on investment as possible, and with the majority of buyers now being higher income, they can afford to raise prices. There is buyer demand at all income stages, as a result of low mortgage rates, further incentivizing price increases. However, the pandemic causing job losses for those unable to work from home, who are primarily lower-income workers, means they’re unable to take advantage of the moment. Lack of affordable housing construction also plays a part in higher prices. It’s not that we aren’t building. It’s that the construction demand currently is primarily for higher income housing, which is also preferred by builders, since high-density, low-income housing is more costly to build.

The increasing popularity of home offices has been mentioned ad nauseum, but how else have homeowners changed their behavior in the house as a result of the pandemic? The America At Home Study, a nationwide survey with about 4000 respondents, may have some answers.

One of the biggest answers should be obvious: Disinfecting more. In addition to this, though, homeowners are reorganizing to save space, particularly in their garages. Some are buying shelving for their garages, others are converting part of their garage into a home gym. Other rooms are also becoming multipurpose, and backyards are being used more frequently as entertainment spaces. Homeowners are also interested in updating their home technology. While interest in germ-resistant countertops and flooring has decreased between April and October, it’s still incredibly popular with 50% of respondents still showing interest.

Whether a high priority on the checklist or just a nice-to-have, most everyone wants to live near the places where they shop. While some people remain loyal to their store of choice regardless of distance, others are perfectly happy to live nearby any place that serves their shopping needs. But which stores are local can say a lot about another important criterion for buying a home — price.

ATTOM Data Solutions releases an annual comparison of properties near three grocery stores: Trader Joe’s, Whole Foods, and ALDI. The data analyzed are current average home values, 5-year home price appreciation, current average home equity, home seller profits, and home flipping rates. Based on their data, Trader Joe’s is the best bet for homeowners wanting to sell, while ALDI reigns supreme for investors look to flip homes. Whole Foods is in the middle of the pack for all measures except home price appreciation, where it is weakest.

Near a Trader Joe’s, the winning scores are average home value of $644,558, average home equity of 37%, and home seller ROI of 51%. ALDI leads in flipping ROI with 58% and 5-year home price appreciation at 41%. It’s important to note that despite ALDI’s advantage in appreciation when measured by percent, the rather low average price of $250,850 means the gross appreciation amount is still lower than the 35% appreciation near Trader Joe’s and 33% appreciation near Whole Foods. Overall, buying near Whole Foods is a pretty safe bet as long as you don’t plan on flipping, since you’d lose out on a 22 percentage point difference in flipping ROI at 36%, still higher than Trader Joe’s at 30%. Of course, whether or not you actually want to shop at the store you’re near is also important!

A moratorium is currently protecting many renters from evictions, but it’s going to end eventually, and many renters will still owe a backlog of payments. What’s more, the legal process for acquiring protection can be difficult to grasp for some renters. The bottom line is that renters are going to need help understanding their rights — as well as fighting for them in court. I’m sure most everyone is aware of their guaranteed legal right to an attorney if they cannot afford one, but not everyone realizes that only applies in criminal cases. People struggling with evictions don’t have that same guarantee.

Fortunately, the federal COVID-19 relief package has taken that into account. In addition to $25 billion in rental assistance and an extension of the eviction moratorium through January, the most recent package also includes $20 million in legal assistance for renters. The vast majority of landlords can already afford an attorney, so aid to renters is aimed at levelling the playing field. The prediction is that it will do more than that, though. An estimated 92% of renters in Baltimore, Maryland, would win their cases if they had legal counsel, yet only 1% do, compared to 96% of landlords.

This brings us to the next step in helping renters get back on their feet: extending the guarantee of legal counsel to renters facing eviction, which is what the aforementioned city of Baltimore has just decided to do. The city has been given four years to complete implementation of this new requirement. It’s even expected to save the city and state money in the long run by reducing costs elsewhere, such as homeless shelters and foster care. Baltimore was only the most recent city to try this, though. It was first accomplished by New York City in 2017, and similar laws exist in San Francisco, Philadelphia, and Newark, New Jersey.

If you’re looking to buy, but aren’t quite sure what you want to buy, this article may help you. There are a few factors you want to consider when deciding between a townhouse and a single-family residence (SFR). The factors we look at here are cost, maintenance, space, and proximity to neighbors.

If price or maintenance are big concerns of yours, you probably want to look at townhouses. Townhouses are generally less expensive than SFRs, both in up-front cost and future costs. Many of your maintenance costs will be handled by the community association. This also goes for the maintenance tasks themselves, so you don’t need to spend as much money or time on maintenance. In addition, the smaller size of townhouses means there will be less maintenance to do in the first place.

Speaking of size, if you want a lot of it, SFRs are the better bet. SFRs are frequently larger and have more flexible space, allowing for the increasingly popular home office. You can also rearrange and redecorate as you please, or add or renovate rooms. Another type of space you’ll have more of is the space between you and your neighbor. SFRs are more private and often quieter with no shared walls.

Remember that there’s no right or wrong answer; it depends entirely on your budget and preferences. If you need help making a decision, though, don’t hesitate to call or email us.

Many attempts have been made, and are still being made, to help lower income people to acquire affordable housing. We haven’t been worried about higher-income housing; those who can even consider affording it don’t particularly need the help. But there’s a group we’ve mostly been forgetting about: the dwindling middle class. The income gap has increased dramatically, but there are still those few who earn too much to get subsidies, yet too little to afford higher priced housing.

To this end, California lawmakers have passed AB 725, which modifies California zoning laws to allow for more moderate-density housing in metropolitan and suburban areas. 25% of the Regional Housing Needs Allocation must be for moderate income housing zoned for 4 or more units. Interestingly, a further 25% must be for above-moderate income housing, also zoned for 4 or more units. This is potentially because there could be significant backlash from a major drop in home values in areas that are already primarily high income neighborhoods.

AB 725 definitely has its flaws, though. Of course, it does little to nothing to further affordable housing, only increasing the density of housing, but that wasn’t the objective. The more pressing issue is that there are no provisions to improve infrastructure for higher densities, fund new constructions, or guarantee that new constructions will qualify for the required income range. Essentially, California lawmakers are saying “You better do this,” without providing any assistance in making it feasible.

With the pandemic creating an employment nightmare, the unemployment rate has been a closely watched statistic. Employment is still below pre-pandemic levels, but has rebounded fairly well. That may be giving us false hope, though, since there are other jobs-related statistics to consider.

In a previous article (https://www.carlandarda.com/?p=1370) we looked at the difference between employment rate, measuring what percentage of those in the labor force have jobs, and labor force participation rate, measuring what percentage of people are able to hold jobs, whether they currently do or not. We already saw there that LFP dropped as a result of the pandemic, indirectly reducing the unemployment rate without actually creating jobs.

But there’s another statistic that sheds some light on what the pandemic has done to the jobs market. The long-term unemployment rate specifically measures what percentage of those looking for a job have been searching for 27 weeks or more. Before this recession, the LTU rate has been around 20%. This means that 80% of unemployed people were finding jobs, retiring, or giving up entirely within six months. This rate has been going up rapidly and was at 37% as of November 2020. Not only have more people given up or been forced into retirement, but more of those still searching for jobs aren’t able to find one quickly.

When the pandemic began towards the end of the first quarter in 2020, people were understandably reluctant to start purchasing houses. As a result, mortgage applications saw a sharp decrease. However, they rebounded quickly, surpassing 2019’s numbers even while trending downwards again in December. In the week ending December 23rd, 2020, mortgage applications dropped 5% from the prior week, yet remained 26% higher than the same week in 2019. As a result of low mortgage rates, refinances shot up in 2020, increasing 4% in the aforementioned week to end 124% higher than the prior year.

So we know that more people sought new mortgages in 2020 because mortgage rates are low, but what does the recent downward trend mean for the market in the near future? Well, probably not much. While some attribute the decrease to the housing shortage and rising prices, the fact of the matter is that this has been the case for quite some time. It’s actually more likely just seasonal variation — mortgage applications already have a tendency to decrease near the holiday season. The pandemic could have some impact, but we’ve already seen that the sharp decline earlier in the year was completely mitigated by low rates increasing demand. A more telling statistic is the average loan balance, which set a record high of $376,800. This is because much of the available housing is on the higher end, pointing to a deficit of affordable housing.

With the pandemic forcing people to stay at home, many are looking to improve the smart technology features of their home. A quarter of those surveyed have more interest in smart tech as a result of spending more time at home, up to 37% for those in the 18-34 age range. Even people who already own smart home technology, which encompasses 57% of all people in the US, are looking for more, with 41% having purchased more since the pandemic began.

The most commonly owned smart tech includes smart TVs, speakers, doorbells, robot vacuums, and thermostats. But if people had to choose just one smart feature to add to their home, over a fifth said it would be a high-tech home security system. This was also one of the most desirable features of a new home, along with a smart doorbell with a camera. Looking to the future, however, 35% want smart home features that would enable them to be more green and energy efficient, particularly focused on solar energy. Practicality isn’t the only concern, though, as entertainment and relaxation based smart tech features are also gaining in popularity as it has become more difficult to entertain oneself outside the home.

Foreclosure and eviction moratoriums for FHA-backed loans were previously set to expire December 31st, 2020. The FHA has now given them a two-month extension to February 28th, 2021. Borrowers will also be able to request initial forbearance through this date, potentially allowing them to remain in forbearance through February 2022. The moratorium applies only to legal occupants of single-family residences.

This extension means FHA moratoriums are extended beyond the FHFA moratoriums affecting those with loans backed by Fannie Mae or Freddie Mac. Those were also recently extended, but only through January 31st, 2021. Of course, given how recent that extension was, it’s entirely possible FHFA borrowers will also get another extension in the future if needed.

The Neverland Ranch, near Santa Barbara, California, is a 2700 acre property previously owned by Michael Jackson. The main residence is 12,500 square feet, and there is also a 3,700 square foot pool house as well as a movie theatre and dance studio. Neverland Ranch additionally features a train station, fire house, and barn. After attempting to list the property for $100 million in 2016 and then again for $67 million in 2017, the trust has now sold it for $22 million.

The new owner is billionaire Ron Burkle, co-founder of the investment firm Yucaipa Companies, who had been an associate of Michael Jackson. Also the controlling shareholder of Soho House, he had been searching for a new location for the members-only club. Burkle eventually concluded that Neverland Ranch was too remote for a new Soho House location, but decided to put in an offer anyway, and was successful.

In the neighborhood of Jordan in Hong Kong is a street called Woosung Street, popular for its restaurants. There is also a hockey academy there, as well as a sports foundation founded by Ahmen Khan. But Khan is doing something else to make people want to come to Woosung Street — he went to a nearby refuse collection site, picked up a refrigerator, painted it blue, and set it up just outside the hockey academy. The color isn’t important, though; what’s important is the sign reading “Give what you can give, take what you need to take.”

And that’s exactly what’s happening. The blue refrigerator project has gone viral, and people are visiting just to drop off food so that others can pick it up for free. The refrigerator is there 24 hours per day. Even though it’s a refrigerator, food isn’t the only thing people are picking up and dropping off. You’ll also find masks, cleaning supplies such as towels, and even clothing items such as socks.

Photo by Latrach Med Jamil on Unsplash This photo does not depict the refrigerator described in this article.

2020 hasn’t been quite as bad for the real estate market as expected; Quarters 3 and 4 have actually experienced incredible recovery and even some growth from Q1 since the enormous downturn in Q2. Home sales are up about 800 from Q1, after falling by over 1100 in Q2. Despite the slowdown in construction, total housing starts now are slightly higher than they were in Q1, with the main difference being that more of them are individual homes and fewer are the more affordable multi-family residences. And now, the announcement of the COVID-19 vaccine has brought even more hope for a better 2021. Fannie Mae still expects a slowdown during the first half of 2021, but that’s because people, including builders, are going to need a bit of time to get back into the flow of things. Once prospective buyers have their incomes sorted, sellers see values going up, and halted constructions have been completed, those new homes should fly off the market. While it’s true that this is a lot of things that need to go right, it’ll be an automatic, albeit slow, process once lockdowns end and employment starts back up.

These delicious holiday muffins are quick and easy to prepare, thanks to your trusty blender. Added bonus: they also happen to be low carb!

Yields 12 muffins

4 large eggs

1/2 cup sour cream or Greek yogurt

1 teaspoon vanilla extract

3/4 cup brown sugar

3 cups almond flour

1 tbsp cocoa powder

2 teaspoons baking powder

1/4 teaspoon salt

2 teaspoons ground ginger

1 teaspoon ground cinnamon

1/4 teaspoon ground cloves

Preheat oven to 325˚ F.

Line a muffin pan with liners.

In large blender jar, combine eggs, sour cream and vanilla extract. Blend approximately 30 seconds.

Add sugar, almond flour, cocoa powder, baking powder, salt and spices. Blend until well combined. If batter is too thick, thin out by adding 1/4 cup water.

Pour the mixture evenly among the prepared muffin cups. Bake 25–30 minutes until golden brown and firm to the touch.

Chances are you’re familiar with the concept of inspecting a home before sale. Seller’s agents are required to list observable defects, but sometimes problems aren’t as easily noticed, which is why seller’s agents will frequently recommend that a qualified home inspector take a look. A good home inspector will always look for defects that affect the property’s value, desirability, habitability, and safety, and they are required to provide the seller’s agent with a home inspection report (HIR). But it may surprise you to know that who can be considered a home inspector is actually rather broad.

A home inspector is really anyone whose business is conducting home inspections and preparing an HIR. The State of California has no home inspection licensing. That doesn’t mean they are necessarily unlicensed, however, as many home inspectors have general contracting licenses or are pest control operators, architects, or engineers. You will occasionally find home inspectors without a license of any kind, which is why seller’s agents always want to be cautious about which home inspector they choose. There are some rules that even unlicensed home inspectors must follow, such as that the inspection be non-invasive and non-damaging to the structure, and that they provide an HIR to the seller’s agent.

Quite a year! Soon we’ll have to do a wrap-up on 2020. But, for today it’s going to be November 2020 versus last year, (November 2019) and versus last month (September 2020).

Let’s start with the big numbers. Over all, total sales in the Los Angeles South Bay for November came in at just shy of $880M, 9% off from September. One could easily consider that drop a seasonal variation as we move into the cold months.

Compared to November 2019, total sales dollars for the combined areas of the South Bay were up 25%. Much of that is making up for sales that didn’t happen during the confusion of the first shutdown this year. Now that things are more stable, we’re seeing a lot more come on the market. Nearly everything coming on the market is selling, and at good prices.

Harbor

The star of the month is the Harbor area with a 42% year over year improvement in sales dollars. Units sold were up 26% Y-Y and median sales price was up 13%. This is a big boost for the San Pedro-Carson-Long Beach area. The increased action and the increased price, outpaced the rest of the South Bay by huge margins.

Generally speaking, the Harbor cities have entry level homes. Those are being bid up dramatically by buyers who newly qualify for purchase loans because mortgage interest rates are now down in the 2-3% range. I suspect there are more than a couple of investors are mixed in there, too.

Palos Verdes

The Palos Verdes peninsula presents an anomaly this month. November compared to October universally shows a seasonal decline in the 1-10% range, but PV dropped 27% in dollar volume. Looking deeper we see the M-M median sales price has dropped by 13%, while neighboring areas have remained within 1-2% of last month’s median price. Monthly sales volume also plummeted by 15% versus an average of 4% down for other areas.

Year over year values are all in line with the rest of the South Bay, by PV seems to be taking a beating from the pandemic.

Beaches

The Beach, by comparison to PV and the Harbor, had a boring November. Volume was down from October by 9% and median price off by 2%. Total dollar sales fell from October by 9%. The numbers are within seasonal expectations, but any time Beach prices fall off more than neighboring areas, it’s a cause of concern. The Beach tends to be a precursor to future changes in the South Bay.

Looking at 2020 over 2019, the number of sales was up 1% and median price was up 3%, leaving a tidy 11% increase in Y-Y total dollars sold. Despite the Covid-19 pandemic, those rock-bottom interest rates are making sales happen faster than last year.

Inland

Inland cities sales volume for November dropped off from last month by 3%. Median sales price declined a mere 1%, while total sales dollars were off by 3%. These are minor drops in light of seasonal impact, showing a strong market even as we go into the winter months.

Looking back to last year, the Torrance-Gardena-Lomita area showed more than respectable growth. Sales volume was up 12% over 2019. Median price was up 10%. Those increases created a total sales dollar increase of 25% above last year.

Not bad for being in a pandemic. Existence of a vaccine should relieve the fear keeping many people away from buying and selling during the coming months. The Federal Reserve Bank has indicated that interest rates will stay down for another 12-24 months. Everything points to a growing confidence over the winter and a booming market in the spring.

The High and the Low

The Los Angeles South Bay is a very diverse set of communities. To show you the breadth of that diversity, let’s take a quick look at the highest priced sale for November, versus the lowest priced sale.

On The Strand in Manhattan Beach a 6025 sq ft house on a double width lot of 6927sf sold for $17,750,000. The listing agent bills this property as a perfect opportunity to build a world class home of over 11,500sf of living space. The sold price per square foot of residence is $2,946.

On Ackerfield Ave in Long Beach a one bedroom one bathroom condo of 641sf sold for $205,000. Per the listing agent the home boasts a community pool and laundry facility, with one carport plus storage. The sold price represents a rate of $319 per square foot.

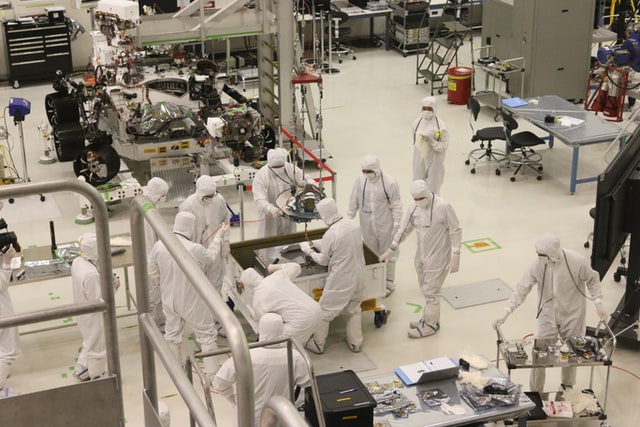

Earlier this year, in April, NASA announced development of Ventilator Intervention Technology Accessible Locally (VITAL), a ventilator designed specifically with COVID-19 in mind. Existing ventilators have more general use cases, but are more expensive and more difficult to build. Currently, 28 manufacturers are licensed to build VITAL, with models variably either pneumatic or using compressed air. In August, one such manufacturer, Russer, has gained approval for its pneumatic model from Anvisa, which is Brazil’s equivalent of the FDA. Nonprofit research organization CIMATEC in Brazil helped develop the Brazilian model. Leone Andrade, the Director of CIMATEC, says that VITAL can also help boost Brazilian industry in addition to helping combat the pandemic.

It’s no secret that California has a shortage of affordable housing, and the diminishing construction rates definitely aren’t helping. Fortunately, there’s a rising statistic that isn’t captured in construction rates — conversions. Various types of commercial structures have been being converted into apartments over the past three decades. In the 90s, the most common type was hotels, followed by factories in the 2000s then offices in the 2010s. Now it seems we’re likely to circle back to hotels, which are experiencing extraordinarily high vacancy rates as travel has decreased during the lockdowns and recession. Hotels are also the best target for conversion to affordable housing because they generally produce lower tier apartments. We shouldn’t discount office conversions, either. As businesses are transitioning to partial or full work-from-home models, less office space is required and businesses will be looking for mixed-use structures.