The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

The first 3D-printed house was put on the market last month, and already multiple other companies are following suit in other states. SQ4D is the company that started it all in New York, and Texas was the first to get on the bandwagon, with ICON completing four 3D-printed homes in East Austin. 3Strands followed suit in Kansas City, and Mighty Buildings in California is also working on a project.

3D printing buildings didn’t just start out, though. ICON actually built several a year ago. They just never went on the market, because they were built as homeless housing, not for-sale properties. ICON has the most experience, but they are no longer without competition. Their biggest competition currently is thought to be Mighty Buildings, which actually started back in 2017 but has taken the time to develop what they hope to be more cost-effective and energy-efficient building materials.

President Biden has proposed a $15,000 tax credit for first-time homebuyers, perhaps aimed at allowing renters who were getting ready to make the jump to homeownership before the pandemic to realize their plans. Not all renters have homeownership in the near future, but it’s possible that the tax credit could help quite a few people. Assuming a down payment of 3.5% for a 30-year loan at 3% interest rate, it could be a boon to renters in 40 of the 50 largest US metros.

Since it’s a flat amount and not a percentage, the tax credit would be especially useful in less expensive metro areas. Areas like Pittsburgh, Cincinnati, Cleveland, and St. Louis could see somewhere around 40% of renters being able to afford a mortgage on the median property with the tax credit. More expensive regions, such as California, aren’t going to benefit as much. It’s more likely that the number of people aided would be only in the thousands. However, these are all probably high estimates, since they are based on the minimum down payment of 3.5% for an FHA loan, which is not ideal.

The proposal does have one major flaw. Currently, demand is quite high and supply is incredibly low. The supply of available properties is already struggling to support the number of prospective buyers. If first-time homebuyers start trying to take advantage of their tax credit, it’s probable they’ll be entirely out of luck. Competition is fierce with multiple offers per property, and those attempting to use tax credits to scrape together money to buy aren’t likely to be providing the best offer.

It shouldn’t be surprising that rates of education are trending upwards, but what you may not be aware of is that the median age is also going up. In 2000, the median age was roughly around 30-34 in most major areas of California, with a statewide median of 33. Our most recent statistics are from 2019, which show that the median age is now above 34 in all but two of these same major areas. The statewide median is up to 37.

This is relevant for the real estate industry, as it portends that there may be fewer first-time buyers. First-time buyers tend to be younger, primarily in the 25-34 age range. The real estate market has generally been able to count first-time homebuyers as a reliable source of market stability, even in uncertain times. Granted, it is true that Millennials — who make up the largest segment of homebuyers currently — are trending towards making their first purchase later in life, which may mean that the effect of an increasing statewide median age is going to be less apparent to the real estate market.

The increasing rate of education, while not necessarily surprising, also could have an impact on the real estate market. More educated people statistically have a tendency to live in large urban centers and are wealthier. This is consistent with the upwards trend in total home value sold despite fewer homes being sold. It is not, however, consistent with the fact that more people are moving away from urban industrial centers as a result of being able to work from home, so the effect is still rather nebulous.

During the 2000s, California’s population increased by 2 per new housing unit constructed. With an average varying between 2 and 3 people per household, this was a fairly sustainable rate of construction. Unfortunately, construction has slowed at the same time that population is still increasing. The ratio is now an increase of 4 per new housing unit constructed. The state has passed laws to combat the housing shortage, but it’s not enough.

UC Berkeley’s Terner Center may have cracked the code. They’ve done a case study of one San Francisco project that was completed 30% faster and 25% cheaper than similar projects, and identified the key factors that led to its success. According to the Terner Center, they are 1. an upfront commitment to low costs and a quick construction, 2. flexible funding, 3. streamlining the approval process, and 4. taking advantage of modular construction, so that some parts of the construction can be done in parallel with others. This is going to require the aid of local governments to make flexible funding more available and modify the approval process.

Currently, there are approximately 2.7 million homeowners protected under forbearance programs. When the foreclosure moratorium expires, which it is slated to do June 30, 2021, these homeowners will have a respite as long as they are in good standing with their forbearance program. This is important, because 2.1 million of those are delinquent in their payments and would otherwise be subject to potential foreclosure immediately after June 30th. This is a fate likely to befall 1.1 million more US homeowners, who are delinquent and aren’t protected under a forbearance program.

Why aren’t they protected? Well, the answer is probably that they don’t know what their options are. Some may not know that forbearance programs even exist, but they certainly do and are still available. They may think they aren’t eligible for whatever reason, even though the only eligibility requirement is financial hardship due to COVID-19. It’s possible they don’t think they will be able to make a lump sum payment after their forbearance period. This is a real concern for a few people; however, most mortgages are backed by Fannie Mae or Freddie Mac, who will allow you to continue to make payments throughout the life of the loan, rather than immediately as soon as forbearance ends.

Project Homekey, a cooperative effort between the State of California, LA County, and Long Beach to convert hotels into homeless housing, has reached a new milestone in its progress. One week ago, on March 15th, one of the transitional housing developments finally opened its doors. Previously a Best Western hotel in Long Beach, it’s now a 102 unit development that’s bringing in homeless residents.

Unfortunately, 102 units can’t support the entire homeless population of Long Beach. They’re currently only looking at accepting at-risk residents — those with medical conditions or who are 65 or older. Homeless residents who are in the process of obtaining permanent housing are also able to apply while they wait to obtain their permanent home.

If you’re in need of rental assistance, now is the time. California opened the window for COVID-19 rent relief applications a few days ago, on March 15th, 2021. There are state, county, and city programs — be sure to look at all the possibilities, because they do have some differences. Also be aware of the application windows. Some close as early as March 31st.

Information about the California state program is available at www.housing.ca.gov, and you can get a personalized report from https://ucilaw.neotalogic.com/a/Cal-Covid-Info-App-for-Tenants-and-Landlords. If you are a landlord, you can also participate in the state program by waiving 20% of the rent in order to get reimbursed for 80% of the unpaid rent. Tenants whose landlords don’t wish to participate are given 25% of their unpaid rent. The state program also pays 25% of prospective rent and provides assistance with utility payments.

Statistically, single women purchase fewer homes than couples or single men, as a result of both economic and societal factors. The gap between single women and single men is only roughly 3-4%, but it’s still not negligible. Fortunately, it’s slowly shrinking, as women are beginning to have a larger share of home purchases. The percent of homes purchased by single women increased by 8.7% in Q4 2020 as compared to Q4 2019. The same statistic for single men is 4.6%. For couples, who may have dual incomes and/or better access to loans, the increase was 11.5%.

This doesn’t mean everything is great for women, though. The pandemic did disproportionately affect women, especially women of color. The industries hit the hardest were restaurants, retail, and healthcare, all of which statistically employ more women than men. What this actually demonstrates is the disparity between economic classes. Those single women who were able to buy in 2019 but held off were likely also able to buy in 2020, and simply had more incentive to purchase because of low interest rates. In some cases, these women were saving up with the intention of buying in the future, and took the opportunity to buy something less expensive to take advantage of interest rates. But those women that were struggling in 2019 definitely had no chance in 2020.

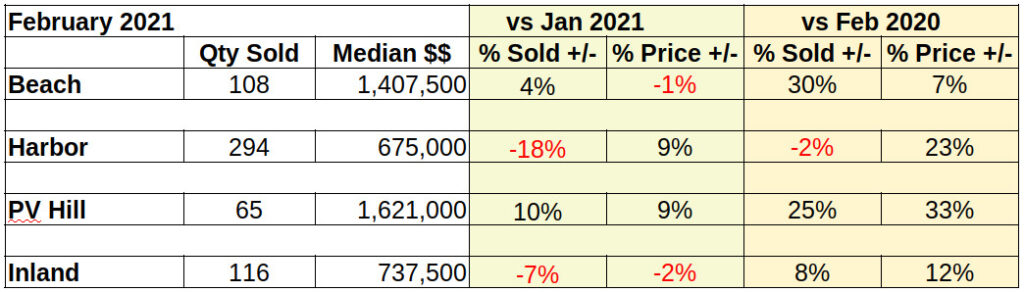

Covid-19 has kept the South Bay real estate market in disarray for a solid year now. So when we try to compare sales activity from 2020 to 2021 we find huge swings in the data that only tell us we’ve been living in a pandemic. We’re here to try to tease some intelligence out of that data and to guide our clients through buying and selling in these tempestuous times.

Month to Month

Let’s start by looking at the number of homes sold in the South Bay for February 2021. At the macro level sales volume is down -10% below January. Of course, that ignores the fact the number of sales last month (January) was down -30% compared to December, the prior month.

That’s the macro level. We start to see the range in sales volume when we step down to an area level. Looking more closely, the number of homes closing escrow in February versus January sales ranged from a decline of -18% in the Harbor area to an increase of 10% on the Palos Verdes peninsula. Comparing sales volume for the first two months of the year very much demonstrated the old maxim about the importance of location .

February against January for median price: Dollar-wise, the Beach dropped again, but by only 1% of the median price paid in January. However, note that this follows a 12% monthly drop in January from December 2020. From that scenario we can’t tell if prices are heading up, or still coming down. In other areas, the prices increased a robust 9% each for the Harbor and PV areas. Inland cities were down by -2%.

In total dollar sales, the South Bay was off by -1% from January activity. Once again, the detail was scattered with the high at 14% for Palos Verdes and the low -16% for the Harbor.

Compared to pre-Covid, these numbers are simply freakish.

Outrageously high! Compared to pre-Covid, these numbers are simply freakish. Back in 2019 any of the percentage statistics we look at on a monthly basis would have been in the range of +/-1%, occasionally a tad more. So, instead of Harbor area prices going up 9% in a month, we would normally be talking about .9%, one tenth the amount of increase.

Year to Year

Clearly the pent up demand from the past 12 months has had some impact. That, combined with the limited supply because so few people want to move during the pandemic. There’s always the question of what percentage of the buyers are home owners as opposed to investors. From speaking to other brokers in the area, we find a large number of the transactions are all cash.”

As always, one should note that ultra-local sales numbers are small in terms of mathematical models. As such, a single sale, high or low dollar, may make percentile statistics jump into outlier ranges. Similarly, a seasonal burst, or dearth of sales can seriously skew the numbers. Based on 25+ years of local real estate experience, I can assure you this is closer to a bubble than to a season burst.

Looking at it on a year over year basis doesn’t improve the image. Still the increases in every corner of South Bay, both in the number of sales and the median price increases, are beyond rational.

In response to the coronavirus pandemic, the Federal Reserve (the Fed) reduced the Federal Funds rate to near zero, which is the rate that the Fed charges banks for loans. Its lowest, and current, point was 0.09%. For comparison, it was at 1.55% in the beginning of 2020. Typically, the 10-year Treasury Note interest rate follows suit. However, the relationship is indirect, so we could see anomalies — which is what has happened.

The T-note rate correlates strongly with investors’ economic certainty, as T-notes are an extremely safe investment. In times of uncertainty, the rate drops as more people are buying T-notes. In more certain times, investors instead move their money to less secure investments with a higher return. While it did decrease from 1.76% to 0.62% in the first half of 2020, it bounced back in the second half. At 1.08%, it is still below the Jan 2020 rate, but is continuing to climb. The Feds meanwhile have no intention of changing the Federal Funds rate until 2023, at which point the T-note rate is virtually guaranteed to go up.

What does all this mean? Well, we can say for sure that the Fed’s decision to keep the Federal Funds rate at 0.09% means they aren’t hopeful for a recovery until 2023. There are a few possibilities as to what the increasing T-note rate means. It could be that investors are too hopeful about less secure investments, and they’ll experience losses. Maybe the Fed is being overly cautious, and the economy is actually about to start recovering soon. Or it could be that investors realized in the first half that they have been largely unaffected by the economic recession, and don’t particularly care that the overall economy is in a slump.

If you know architects, you may know Edward Killingsworth, a US architect who lived in Long Beach. One of the houses he designed still sits at 2 Laguna Place. The estate of the original owners sold it in 2018 with the original design for $2.6 million.

It’s no longer fully Killingsworth, as the new owners have remodeled it, but it retains some quintessential Killingsworth features: plenty of glass, floating stairs, stone countertops, and perhaps most importantly post-and-beam ceilings. It’s been updated with top-of-the-line new appliances and modernized master suite and bathrooms. There’s even an elevator. The new additions bring the price tag up to $5.179 million.

Real estate was halted only briefly as a result of pandemic lockdowns, but real estate is not the only aspect of the economy. Not all sectors were equally affected, so real estate won’t recover at the same rate for each sector. Retail was hit the hardest, with many businesses closing temporarily during lockdowns and some being entirely replaced by e-commerce. Success of retail is somewhat difficult to measure from a real estate perspective, but one obvious statistic is vacancy rate, which increased to 6.2% in Greater Los Angeles. It’s since dropped slightly to 5.9%, though restaurants still seem to be faring better than other retail establishments even with weakened restrictions.

Offices are essentially treading water after a steep dropoff. Many businesses have already recognized the need to transition to fully or mostly work-from-home, and already have plans in the works for how they’re going to adapt. Though they’ve certainly experienced losses, it’s unlikely to get much worse for them.

The residential market is still a flurry of activity, albeit predominantly from buyers trying to get a competitive edge. With how low inventory is, it’s inevitable that some of them will fail. Competition favors higher-income buyers, who were also less affected by the recession to begin with, so they haven’t experienced any pull to slow down. Nevertheless, it’s still clearly a seller-controlled market, and sellers don’t want to sell right now.

Meanwhile, the industrial sector has actually experienced gains. Contrary to brick-and-mortar retail, consumers don’t need to go anywhere to pull products out of warehouses. They just buy everything online. Currently, the industrial sector’s biggest roadblock is not having enough land to build even more warehouses to keep up with demand.

The lockdowns from the pandemic negatively affected several industries. With most flights being cancelled, you’d expect the aerospace industry to have suffered quite a bit. In reality, their employment numbers rose 6% during the shutdowns. How? They adapted, beginning to focus more on space technology and even on pandemic relief engineering.

Several aerospace companies aided the coronavirus relief effort by designing and manufacturing ventilators, face helmets, and face shields. These include Virgin Orbit, Virgin Galactic, and the Jet Propulsion Laboratory. Some focused more on the booming space industry. All in all, aerospace lost 1400 jobs but gained 3000.

It’s a well-known fact that Black and Latinx people tend to struggle economically more than whites and Asians in the US. The wealth gap may be larger than you think, though. Examining homeownership statistics demonstrates just how significant the difference is.

California’s housing affordability for Latinx people is 20% for single-family homes and 33% for townhomes or condos. Blacks fare even worse, at 19% and 30% respectively. By contrast, 38% of whites and 43% of Asians can afford an SFR in California, and 51% of whites and 56% of Asians can afford a condo or townhouse. Part of the problem is California’s high prices, but while affordability at the national level is higher for everyone, the disparity remains about the same, and possibly larger. 62% of whites and 70% of Asians can afford a home in the US. Only 51% of Latinx people and 42% of Blacks are able to.

Within California, the disparity is smallest in San Bernardino County, which is also the most affordable for Black and Latinx households at 46% and 54% respectively. The difference between Latinx and white households is only 3%. It’s not the most affordable for white and Asian households, though — those are actually Fresno County at 61% for whites and Kern County at 68% for Asians. The least affordable county for Blacks is San Francisco County at 8%, and for Latinx households it’s Santa Clara County at 11%.

Demand is so high compared to supply that many prospective buyers are finding competition to be a larger impediment to purchasing a home than lacking funds, even in the midst of a recession. In January 2021, 56% of prospective buyers had bidding wars. This number is up 4% from the prior month. Getting outbid is the primary reason that 40% of prospective home buyers’ searches have dragged on. Only a year ago, just 19% cited this as the primary reason, with 44% saying it was high prices that drove them out of contention. Prices don’t seem to be as much of an issue now, as buyers are willing to overpay in order to get their chance at slim inventory while mortgage rates are still low.

That 56% nationwide doesn’t tell the whole story, though. Competition is much fiercer in some areas. San Diego, San Francisco Bay, Denver, and Seattle all had numbers over 70%. Even beyond that is Salt Lake City, where a whopping 90% of offers had competition.

In many cases, a recession results in credit scores dropping as more people are forced to temporarily rely on credit to make routine payments. This is just one of the many ways that the current recession bucks the trends. Lockdowns, work-from-home, moratoriums, and federal relief packages have all resulted in people spending less and recouping more of their losses than their normally would during a recession. As a result, people are less reliant on credit and their credit scores go up.

The two credit scoring services lenders use the most are FICO and VantageScore. Generally, one’s FICO score is slightly higher than their VantageScore, since FICO requires a full six months of credit history to calculate a score and therefore counts fewer people. Both systems range from 300 to 850, with a FICO score of at least 660 or VantageScore of at least 670 being considered good credit. At the start of 2020, the average FICO score was 703. This increased to 711 by October 2020. Average VantageScore also went up from 686 to 690 from 2019 to 2020. VantageScore reports indicate that subprime scores — those below 600 — decreased by about 3% between January and November 2020, while prime and super prime scores went up. Near prime scores remained about the same.

Unfortunately, some of this is just delaying the inevitable. Some of those who did take out loans during the pandemic were able to negotiate deferring their payments, which also had the effect of protecting their credit scores. Once federal protections end, which will occur 120 days after the coronavirus emergency declaration is lifted, some people aren’t going to be able to repay their deferred loans. That’s going to result in credit scores plummeting.

New York construction company SQ4D may have the latest and greatest in construction technology. They’ve used a giant 3D printer to print houses from the bottom up out of concrete, right on the site. Their first demo house, as a proof of ability, was in Calverston, New York. The next one is already up for sale, despite not having been built yet. The 1400 square foot house will be located in Riverhead, New York and is listed at $299,000.

This isn’t just some publicity stunt. 3D printing has some real benefits. Most notably, construction is significantly shorter. SQ4D’s first house took just eight days to build — and that includes the planning process. The actual construction? 48 hours. Making the process this quick must incur significant expenses, right? Well, no, it was actually cheaper according to SQ4D. The transportation and labor costs associated with traditional construction mean that 3D printing is about 30% less expensive. The new method has been met with some skepticism, though. No one is sure exactly how this will affect the construction industry, as skilled tradesmen may suddenly find themselves replaced with printers.

WalletHub, normally a personal finance website, has released data of a somewhat different nature. They’ve decided to rank 182 of the most populated US cities according to various indicators of health. The categories measured are health care, food, fitness, and green space. On a scale from 0 to 100, the top scoring city averaged across all categories was San Francisco, CA, with a score of 69.11. The lowest score was 23.39, given to Brownsville, TX.

Half of the top 10 cities are on the west coast, with 3 of them being in California. Two through ten are Seattle, WA, Portland, OR, San Diego, CA, Honolulu, HI, Washington, DC, Austin, TX, Irvine, CA, Portland, ME, and Denver, CO. In addition to being #1 overall, San Francisco also takes the number 1 spot for two categories, food and green space. Top rank for the health care and fitness belong to South Burlington, VT, and Scottsdale, AZ, respectively. These cities are also in the top 20 overall, though South Burlington ranks rather low in green space.

Low mortgage rates have resulted in increased buyer demand, and shifting preferences in home features are specifically increasing the demand for new constructions. With sellers waiting out the pandemic, there aren’t many existing homes available for sale. In addition, they don’t always have the features that the new generation of buyers is looking for, such as home offices, larger spaces, and outdoor amenities.

Chief economist Robert Dietz of the National Association of Home Builders (NAHB) predicts a 5% increase in construction starts by the end of 2021. Even so, buyer demand is expected to continue to outpace construction, so sales of existing homes will likely also increase. Builders are going to have trouble keeping up, not only due to lack of time or labor, but also because of increasing costs. The cost of lumber has gone up 169% since April 2020, the month after lockdowns started. Construction companies also report significant issues with obtaining timely approval and navigating new construction ordinances.

Those who have been able to buy during the pandemic have enjoyed extraordinarily low interest rates. It seems like time may be running out, though. At 2.96% as of February 10th, the 30-year fixed rate is still below 3%, but it has started to go back up, from 2.92% the prior week. Because of the increasing rates, mortgage applications to buy dropped 5% in that week. Refinances also went down, by 4%.

It’s still not clear whether this trend will continue in the future, as it’s only just begun. And both applications to purchase and refinances are still up significantly from last year, by 17% and 46% respectively. The Mortgage Banker’s Association (MBA) is predicting that this was only a slight dropoff in total loan volume, as a greater percentage of the loans are for higher-priced homes, primarily because their availability is higher. Of course, even though this is a silver lining for mortgage bankers, it doesn’t help the general populace at all.