The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

The Home Purchase Sentiment Index (HPSI) is a 100 point scaled measurement of housing consumer optimism based on Fannie Mae’s National Housing Survey (NHS). The HPSI is an aggregate of several categories within the NHS. Only one category decreased in March from February, which is mortgage rate outlook. Overall, the HPSI increased 5.2 points in March, up to 81.7, and the year-over-year increase was 0.9 points.

Multiple factors have contributed to this increase. More people are being vaccinated against COVID. Stimulus checks had just been sent out. The spring season also naturally brings more homebuyers, and in this case, even more than usual as buyers had pent up demand from being unable to purchase the prior March due to lockdowns. The statistics generally point to a seller’s market, so prospective sellers should be even more optimistic.

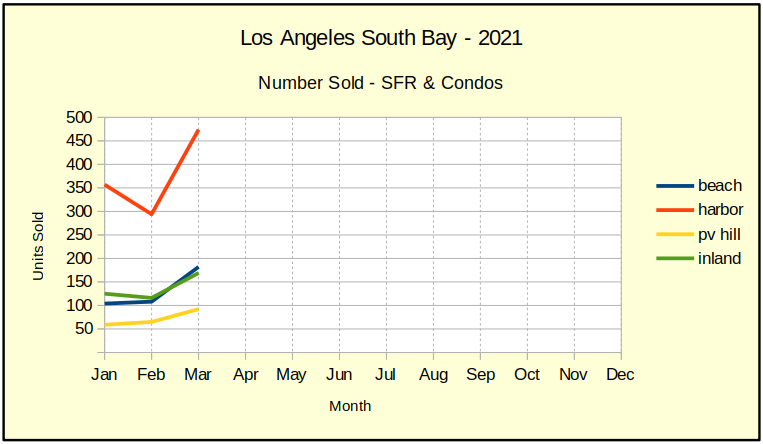

From the Beach to the Harbor, from Inland to the Hill, the month of March brought an average of 57% more home sales than February! This, after February fell 10% from January, and January was down 30% from December! It’s almost as though spring’s sunlight is breaking through a crack in the Covid wall.

Last March we were seeing healthy spring growth ranging from 8% to 29% in sales volume over the prior month. By comparison this March is in a range of from 42% to 69%. That’s a tremendous jump in sales, and it corresponds nicely with the 35% to 70% annual increase in sales over March of 2020. Rarely do we see year over year sales growth above 35% in any given area, so that level of growth across the South Bay is a strong indicator that we are coming out of the erratic market of the past year.

We need to remember that home sales recorded in March of last year were transactions initiated in February for a Close of Escrow 30 days later. The comparison we’re looking at is the last normal March sales, pre-pandemic, compared to the most recent March sales as we roll into vaccinations en masse. That means they were the final set of “normal” transactions before the Covid pandemic was declared. It also means comparing statistics for this April to last April won’t be terribly useful.

That spike in sales is the “pent up demand” we’ve been hearing about. Circumstances that create a need for people to relocate have continued throughout the pandemic. Simultaneously, sellers have been very reluctant to put their homes on the market and take a chance on contracting Covid-19 from a visiting buyer. Now that threat has diminished, so buyers and sellers are making up for lost time.

We anticipate continued froth in the form of increased prices and bidding wars for the balance of 2021. Gradually everyone will catch up with their real estate goals and things will settle down. There is a good chance most of the price increases will stay with us. That’s a plus for sellers, while buyers will only be hurt by the higher prices.

Prices Skyrocket with Pent-Up Demand

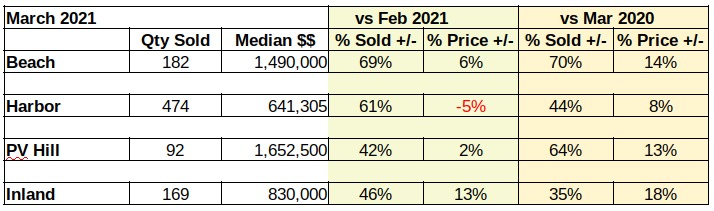

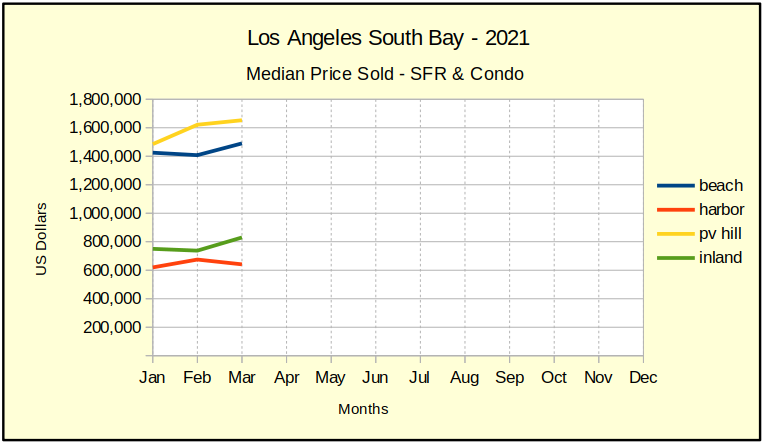

Switching our attention from sales volume to median value, let’s look at how prices have been changing. Year-over-year, the median price came in above last March in the range of 8% to 18%. This is stubbornly high compared to the Consumer Price Index (CPI) of 4.7% for increased housing costs in the Greater LA area during 2020. The last time annual price increases were this dramatic was just before the Great Recession.

When we look a little closer, we’re seeing some weakness in the more current sales prices. Beach and Inland areas both showed big month-to-month improvement over February of this year. The Hill had a more modest 2% increase. The single negative showing in the first quarter, Harbor prices are down -5% for March, despite rising 1% in January and another 9% in February.

As the pandemic ends, we’re seeing a lot of people trying to escape the lease trap (rental prices are going up even faster than sales prices) by taking advantage of historically low interest rates. However, rising sales prices are meeting resistance on the part of some buyers. Possibly because interest rates have starting climbing again. Possibly because the employment picture is still untenable for many.

As the chart above shows, prices for the first quarter are wobbly–a little up and a little down. The Fed is trying to stimulate financial activity to pull our nation through the pandemic by keeping the overnight bank loan rate at near zero. Meantime, the investor market is smelling money and gradually hiking mortgage rates. As the mortgage interest rate edges up, more and more potential buyers are priced out of the market. The first place this shows up is in the entry level market, which is predominately found in the Harbor and Inland areas.

Real Estate for Spring / Summer??

So what’s the forecast for the hottest selling months of the year? The pundits are split about 50/50 on whether the stimulus funding will turn this into a booming economy, or when we emerge from the pandemic, we’ll run smack into a wall of recession.

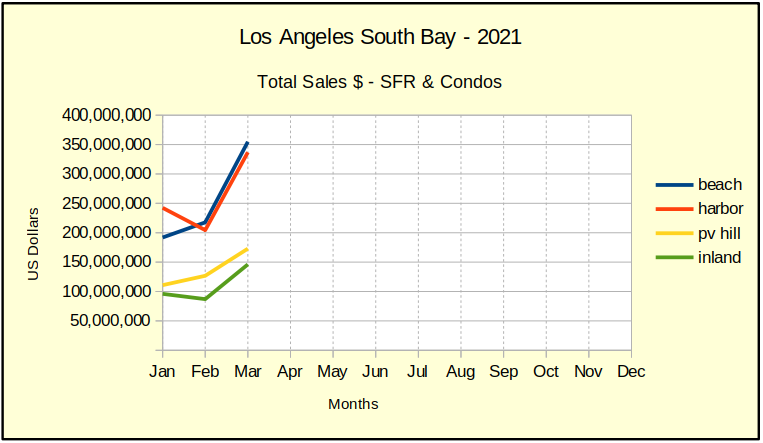

There is definitely money flowing. The Beach and the Harbor areas show the steepest growth, both adding about $135M in overall sales from February to March.

Anecdotally, there’s a significant percentage of first-time buyers who are now able to qualify for a loan, because of the interest rate. That group is looking at entry level homes throughout the area. Another set of buyers is now able to buy an additional investment property to rent out, because of the interest rate. First time buyers and investors are looking at the same properties and bidding against each other.

As mentioned earlier, April 2020 is when the pandemic blew holes in the economy. Whatever April brings this year, we’ll have to find a new way of looking at it. April and May last year plummeted with drops ranging from 25% to over 50%. Comparisons to last year could be interesting, but most likely uninformative.

Part of the COVID relief package included a change to tax deductions for business meals. Until December 31, 2022, businesses can write off 100% of their food and beverage spending at restaurants. This provision does not include grocery stores, office cafeterias, or similar. It was designed to assist restaurants, which have been greatly affected by the pandemic, by encouraging business spending. It does include writeoffs by freelancers who are considered to own their own business.

There are some requirements. The business owner or an employee must be present, so it doesn’t apply to situations such as contactless pickup or delivery directly to a client. You need to keep your receipts and provide an explanation of when, where, why, and with whom the meal was shared. The meal must reasonably be considered business related, such as between coworkers or an agent and client, though it’s not necessary that the meeting be successful.

The FHA has its origins in the Great Depression, as a method for people down on their luck to secure a loan without much upfront cost. Given the current recession’s similar circumstances, it may be expected that FHA loans would increase in popularity around this time. That isn’t the case at all, because now there’s competition. FHFA loans — those backed by Fannie Mae or Freddie Mac — are currently a better deal.

The normally low upfront cost of FHA loans is countered by the fact that they have mortgage insurance premiums (MIPs), part of which is an upfront cost. This means that you are spending more over the life of the loan than with a conventional loan even with an equal interest rate. This MIP can be cancelled after 11 years if the down payment was at least 10%. However, the appeal of an FHA loan was the minimum down payment of only 3.5%, so this circumstance rarely came up.

But now, 3.5% isn’t even the lowest minimum down payment. FHFA loans have adopted a 3% minimum. What’s more, their upfront costs are actually lower, with no upfront mortgage premium. The MIP cancellation criteria are also different: The down payment amount and loan length don’t matter, and it can instead be cancelled whenever the home equity reaches 80%. Given that it’s rare for a house to be owned for 11 years, especially for first-time buyers who benefit the most from low down payment minimums, this flexibility is highly attractive.

Under normal circumstances, unemployment benefits are considered taxable income. However, the current circumstances aren’t normal. The American Rescue Plan brought with it a provision that the first $10,200 — or $20,400 if married and filing jointly — of your unemployment payments will not be taxed for 2020. The estimated tax break is around $1000 to $2000.

While the IRS will automatically adjust your tax refund amount, it may be helpful to send in an amended return, because tax credits are not automatically adjusted. The Earned Income Tax Credit (EITC) is a frequently unclaimed tax credit that can net you up to $6600 in additional credits, based on filing status, income, and number of children. Because a large portion of your unemployment benefits can be dropped off your income amount, it may cause you to become eligible for EITC if you were not already. Given how frequently it’s unclaimed, it’s also entirely possible that you were already eligible and didn’t bother to claim it, and you can still do so in an amended return. However, be aware that filing an amended return can cost money, and may not actually benefit you depending on the amount of additional tax credits you are eligible for.

The eviction moratorium has received multiple extensions, buying tenants some time to gather necessary funds. Unfortunately, buying them time doesn’t actually aid them in getting funds, and all the while, landlords are also missing a portion of their income. There is no plan for loss mitigation. SB-91 may help somewhat — it allows landlords to acquire 80% of their rent payments via federal funds by waiving the remaining balance. However, this law exists only in California, and doesn’t apply to all rental situations.

Landlords do have another way to mitigate their losses, but it’s not a good option. Landlords who are close enough to do the job themselves could reduce their costs by laying off their property managers and maintenance staff. This doesn’t help anyone, though, and results in increased job losses. While landlords definitely do take a risk in getting a mortgage on a rental property, currently their best recourse to offload that risk is in ways that do nothing to aid a recovery and instead exacerbate job losses. It may be tempting to let risky investments fail, but at the same time, it could be worthwhile to also give landlords as well as tenants some breathing room to avoid worsening the issue.

Death rate is a regularly documented figure within most countries in the world. Less common is calculating the excess death rate — the number of deaths in one country in excess of a control rate. An international study used the average rate in western Europe as a baseline and compared 18 individual countries to that rate. The US ranked among the worst for individuals under age 75.

This isn’t even about COVID — the study examines the years from 2000, 2010, and 2017, well before COVID was a thing. In 2017 alone, Americans between the ages of 30 and 34 were three times as likely to die as those in Europe. This is mostly attributed to drug overdoses and gun violence. The US has much laxer gun laws than many other countries, and drug abuse is usually not medically treated. Structural inequality is also a large factor, including in access to health care.

The category in which the US actually fared better than Europe was those over age 85. There were 97,788 fewer deaths than expected based on the control rate in 2017. The reason is not entirely known, but one suggestion is the fact that US medical care places higher emphasis on end-of-life care. Another possibility goes back to the inequality in access to health care. Access is higher for senior citizens; in addition, those with good health care are more likely to have reached age 85.

Common interest development (CID) is a broad term referring to condominiums, community apartments, planned developments, and stock cooperatives. CIDs often have a homeowner’s association (HOA), which has been the governing force for how units within the CID are rented out, as CIDs have not been subject to government rental laws. California changed this in January, requiring CIDs to allow at least 25% of the owners to rent out the units. They also may not prohibit rentals of accessory dwelling units (ADUs). CIDs can still prohibit short-term rentals.

The law came into effect on January 1st, 2021. CID documents may not immediately reflect this change, but they still must abide the new law and are required to amend their documents by December 31st, 2021. Violation can result in a fine of up to $1000.

Assembly Bill 1885 went into effect January 1st of this year, increasing the debt exemption amount on a property when the owner’s spouse dies. Prior law set the amount at either $75,000, $100,000, or $175,000 depending on factors related to the residents. New law instead bases the amount on the countywide median sales price. The exemption amount is equal to this amount if the countywide median sales price is greater than $300,000, up to a maximum exemption of $600,000. Otherwise, the exemption amount is the minimum of $300,000.

Back in November 2019, the California Law Revision Commission (CLRC) recommended some changes to the laws surrounding the Revocable Transfer on Death Deed (RTDD). RTDD simplifies the process of transferring properties upon death. CLRC also suggested a 10 year extension, but noted that further study would be required. RTDD was set to expire on January 1, 2021, but the pandemic has made review difficult. To give more time for review, it has now been extended an additional year, to January 2022.

Several pallet shelters have been going up around Southern California to aid in housing the homeless, including in Riverside, the San Fernando Valley, and Redondo Beach. Wilmington is the newest addition, with 75 structures expected to be finished sometime this month.

Pallet shelters, while considered temporary housing, have several advantages over more permanent structures. Notably, it only costs $5000 to build a pallet shelter. It may seem inexpensive to convert existing buildings, but the truth is, it’s costly to modify buildings that aren’t meant as residences to accommodate living quarters. Pallet shelters are designed as residences from the get-go, meaning they’re more similar to traditional housing and feel more like a place to live, rather than a place to seek temporary shelter. They also offer more privacy than 100-resident shelters.

The Wilmington project is also designed to instill a sense of community. While the individual shelters are private, the area itself is public and includes communal areas for the residents to interact with each other and friends from outside. Food will be catered to the site. The site will be overseen by The Salvation Army and they will provide case workers and housing counselors.

I’m sure you all know that when you take out a mortgage loan, you pay back the principal plus interest over the life of the loan, in monthly payments. But it’s important to understand that monthly payments are not simply the principal plus interest divided by the total length in months. Because the amortization schedule ensures that each monthly payment is the same amount, it may appear as though each payment is identical. However, this is not the case.

Amortization schedules determine what percentage of each monthly payment is principal and what percentage is interest. When you first get a loan, nearly the entirety of your monthly payments are used to pay off interest, with scarcely any reduction in the principal. As you pay off more of your interest over the life of the loan, a greater percentage goes towards the principal. When you sell a home that still has a mortgage, the amount of money you receive due to equity depends on how much of the principal amount is paid off. If it’s still very early in the loan’s lifetime, you haven’t paid much of the principal, so your equity will be quite low.

Well, as with most things, that depends. Sooner rather than later is certainly the correct time to buy, since mortgage interest rates are going back up and prices are still going up. However, it’s also very difficult to buy right now, because high demand and low supply makes for cutthroat competition. The pandemic certainly played a role in this, but the principal factor in the low availability is lack of construction that has been going on for decades, particularly of multi-family residences. So, the question is really, “Can I buy now?”

Houses are not staying on the market very long, and only the best offers are being accepted. Hesitation is sure to lead to a failed attempt. If you think you can provide the best offer, just send it in; don’t wait. If you attempt to wait out the competition, you’ll be waiting quite a while to get the best deals. It’s likely that inventory is going up in the near future, but that’s not going to instantly impact prices — prices are unlikely to go down at all until interest rates are higher. If you can’t provide the best offer, your chances may be low now, but they will be even lower in the future in the short term. Either act now, or play the long game.

The nonprofit company Restore Neighborhoods LA (RNLA) has just built a small homeless housing development in the Vermont Knolls neighborhood of LA. The cost per unit to build was a mere $225,000, less than half of the $500,000 average for homeless housing in LA. With only eight units, it does little to solve homelessness on its own, but RNLA hopes its financing strategy can be used by others to build more affordable housing faster.

How many builders get money is called the “lasagna of financing” — acquiring funding from several sources, including city, county, state, federal, and private sources. Going through this process takes time, as each different source requires a different application and approval process, and things could change between getting approval from one source and being rejected by another. It could also incur additional costs, such as application fees and hiring financial and legal experts. RNLA instead avoided this bureaucracy by opting for mostly single-source financing. They received the entirety of their $920,000 loan from a single private company called Genesis LA, and the rest of their financial support came from LA county grants and crowdfunding.

Unfortunately, it’s not likely that many builders will be able to acquire funding in this way for larger projects. Single sources simply don’t have the money, or don’t want to risk it, for a large project. The lasagna system has the benefit that no single source is incurring much risk, since they are each able to finance a smaller portion of the costs.

Populous cities are generally considered to be higher density areas, but in some of the largest cities in California, about 75% of the land is zoned for single-family residences. The history of the overabundance of SFRs can be traced back to segregation. It was a tool designed to price out lower-income Black people from predominantly white neighborhoods, something which cities hope to rectify with new zoning laws.

Though many people aren’t aware of the racist roots, and rezoning isn’t going to completely eliminate racism, SFRs are outdated in more ways than one. California desperately needs more affordable housing, but building large apartment complexes is expensive for construction companies. The middle ground is medium-density housing, such as triplexes and fourplexes. To that end, San Francisco has drafted plans to allow fourplexes in every district considered a residential district. A few other Bay Area cities are considering similar plans.

The first 3D-printed house was put on the market last month, and already multiple other companies are following suit in other states. SQ4D is the company that started it all in New York, and Texas was the first to get on the bandwagon, with ICON completing four 3D-printed homes in East Austin. 3Strands followed suit in Kansas City, and Mighty Buildings in California is also working on a project.

3D printing buildings didn’t just start out, though. ICON actually built several a year ago. They just never went on the market, because they were built as homeless housing, not for-sale properties. ICON has the most experience, but they are no longer without competition. Their biggest competition currently is thought to be Mighty Buildings, which actually started back in 2017 but has taken the time to develop what they hope to be more cost-effective and energy-efficient building materials.

President Biden has proposed a $15,000 tax credit for first-time homebuyers, perhaps aimed at allowing renters who were getting ready to make the jump to homeownership before the pandemic to realize their plans. Not all renters have homeownership in the near future, but it’s possible that the tax credit could help quite a few people. Assuming a down payment of 3.5% for a 30-year loan at 3% interest rate, it could be a boon to renters in 40 of the 50 largest US metros.

Since it’s a flat amount and not a percentage, the tax credit would be especially useful in less expensive metro areas. Areas like Pittsburgh, Cincinnati, Cleveland, and St. Louis could see somewhere around 40% of renters being able to afford a mortgage on the median property with the tax credit. More expensive regions, such as California, aren’t going to benefit as much. It’s more likely that the number of people aided would be only in the thousands. However, these are all probably high estimates, since they are based on the minimum down payment of 3.5% for an FHA loan, which is not ideal.

The proposal does have one major flaw. Currently, demand is quite high and supply is incredibly low. The supply of available properties is already struggling to support the number of prospective buyers. If first-time homebuyers start trying to take advantage of their tax credit, it’s probable they’ll be entirely out of luck. Competition is fierce with multiple offers per property, and those attempting to use tax credits to scrape together money to buy aren’t likely to be providing the best offer.

It shouldn’t be surprising that rates of education are trending upwards, but what you may not be aware of is that the median age is also going up. In 2000, the median age was roughly around 30-34 in most major areas of California, with a statewide median of 33. Our most recent statistics are from 2019, which show that the median age is now above 34 in all but two of these same major areas. The statewide median is up to 37.

This is relevant for the real estate industry, as it portends that there may be fewer first-time buyers. First-time buyers tend to be younger, primarily in the 25-34 age range. The real estate market has generally been able to count first-time homebuyers as a reliable source of market stability, even in uncertain times. Granted, it is true that Millennials — who make up the largest segment of homebuyers currently — are trending towards making their first purchase later in life, which may mean that the effect of an increasing statewide median age is going to be less apparent to the real estate market.

The increasing rate of education, while not necessarily surprising, also could have an impact on the real estate market. More educated people statistically have a tendency to live in large urban centers and are wealthier. This is consistent with the upwards trend in total home value sold despite fewer homes being sold. It is not, however, consistent with the fact that more people are moving away from urban industrial centers as a result of being able to work from home, so the effect is still rather nebulous.

During the 2000s, California’s population increased by 2 per new housing unit constructed. With an average varying between 2 and 3 people per household, this was a fairly sustainable rate of construction. Unfortunately, construction has slowed at the same time that population is still increasing. The ratio is now an increase of 4 per new housing unit constructed. The state has passed laws to combat the housing shortage, but it’s not enough.

UC Berkeley’s Terner Center may have cracked the code. They’ve done a case study of one San Francisco project that was completed 30% faster and 25% cheaper than similar projects, and identified the key factors that led to its success. According to the Terner Center, they are 1. an upfront commitment to low costs and a quick construction, 2. flexible funding, 3. streamlining the approval process, and 4. taking advantage of modular construction, so that some parts of the construction can be done in parallel with others. This is going to require the aid of local governments to make flexible funding more available and modify the approval process.

Currently, there are approximately 2.7 million homeowners protected under forbearance programs. When the foreclosure moratorium expires, which it is slated to do June 30, 2021, these homeowners will have a respite as long as they are in good standing with their forbearance program. This is important, because 2.1 million of those are delinquent in their payments and would otherwise be subject to potential foreclosure immediately after June 30th. This is a fate likely to befall 1.1 million more US homeowners, who are delinquent and aren’t protected under a forbearance program.

Why aren’t they protected? Well, the answer is probably that they don’t know what their options are. Some may not know that forbearance programs even exist, but they certainly do and are still available. They may think they aren’t eligible for whatever reason, even though the only eligibility requirement is financial hardship due to COVID-19. It’s possible they don’t think they will be able to make a lump sum payment after their forbearance period. This is a real concern for a few people; however, most mortgages are backed by Fannie Mae or Freddie Mac, who will allow you to continue to make payments throughout the life of the loan, rather than immediately as soon as forbearance ends.