The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

The foreclosure moratorium is over now, putting many homeowners at risk. However, unlike the previous recession, homeowners actually have options this time around. Home prices are high, rather than low, meaning home equity has also increased. This will allow many homeowners to sell their homes instead of being foreclosed on.

The average annual gain in equity this year was $51,500, the highest point in the past 11 years. It’s also five times the value last year. Another important statistic is negative equity, which CoreLogic started tracking in 2009. Fewer homes than ever since the statistic has been tracked have negative equity, at only 2.3%. At the state level, Louisiana is somewhat struggling at 7.8% negative equity share. Among metros, Chicago has the highest negative equity share at 5.2%, but also the second lowest amount of negative equity — meaning more people have lost money than average, but those who have haven’t lost very much. Conversely, San Francisco has the lowest negative equity share at 0.6%, but the highest amount of negative equity.

Homeownership has been a mainstay in suburban areas, where the typical house is a single-family residence or possibly a duplex. Residents in these areas have tended to be middle- or high-income earners. All of this is starting to change as the demographic is switching to Millennials and Gen Z homeowners. The majority of residents in suburbs are now renters, unable to afford to purchase a home.

Millennials and older Gen Z people inherited the effects of the Great Recession, which delayed their careers and consequently their ability to own a home. This also compounded with student debt, since Millennials are a highly educated generation. All the while, prices are increasing but wage growth is stagnant. While some of these people recovered somewhat since the Great Recession, others were still trying to get back on their feet or were just entering the job market when the 2020 recession hit. Most of Gen Z is still not old enough to own a home, so it’s unclear whether this would extend to them as well.

Cryptocurrency has been around for a bit now and is in widespread use, with its major appeal being how difficult it is to counterfeit or manipulate. It’s usually used to make smaller payments, such as purchasing software or electronics. But as with physical money, cryptocurrency can be used for payments of any magnitude. That includes thinks like home purchases or mortgage payments.

If you’re unfamiliar with cryptocurrency, you may think that because it’s generally used for smaller payments, it must take a lot to be able to afford a house. That’s not exactly true. One popular cryptocurrency, Bitcoin, is actually worth $43,000 per coin currently — most payments are made in mere fractions of coins. The value of cryptocurrency does fluctuate wildly, but the trend has been generally upwards in the past few years, albeit at a declining rate of increase.

Some people are rather handy around the house and like to do repair or patch jobs themselves. Or maybe you’d prefer not to have to do it yourself, but money is tight. Whatever your reasons, there are some things you really should call a professional for, if you don’t have experience in that field yourself. If you can’t decide whether you want to try it yourself or not, the bottom like is that structural work and potentially dangerous work should be done by a trained professional, but cosmetic work or simple repairs you can do yourself.

For most people, applying a fresh coat of paint to interior walls or cabinets is not a difficult task, and you may even have leftover paint in storage from when it was originally painted. Exterior walls, however, generally require specialized tools and can have safety concerns. Some plumbing jobs can be done yourself, such as small parts replacement, but leave the pipework and repairing major leaks to an actual plumber. Electrical systems and carpentry are potentially dangerous and should always be handled by a professional.

The California Association of REALTORS® (C.A.R.) has launched a new website, www.BringYourFamilyHome.com. This page will provide information to prospective homebuyers, especially aimed at first-time homebuyers, about financial literacy, credit scores, steps in the process, and how to contact agents. And C.A.R. hopes to address a long-standing issue by presenting the page in both English and Spanish.

California has a significant Latinx population, and many of them believe they aren’t able to afford a home. While certainly some of them don’t have enough income for the high prices in California, a significant number have misconceptions about what they can and can’t afford. 85% of Latinx prospective homebuyers still see owning a home as a big part of the American Dream, and the majority of those haven’t given up on it. But four out of five aren’t aware that they qualify for mortgage loans. 25% of Latinx people that are renting actually don’t need to because they can already afford to purchase, but don’t realize that and aren’t aware of the process. By providing educational materials in Spanish, C.A.R. hopes to help many more Latinx households achieve homeownership.

Property insurance is not legally mandated; however, it is a requirement in order to qualify for the majority of mortgage loans. But with wildfires increasing in frequency in California, higher risk means higher insurance premiums for anyone living in a fire-prone area.

Some people can’t even qualify to renew their insurance because they can’t afford it. Since their lenders still require it, that just means they’ll pay even more for coverage under the Fair Access to Insurance Requirements (FAIR) plan. FAIR is a California state insurance program that anyone in a high-risk area qualifies for. Unfortunately, it’s usually even more expensive and generally provides weaker coverage.

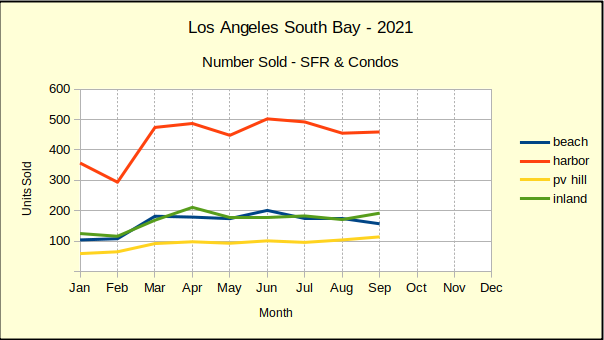

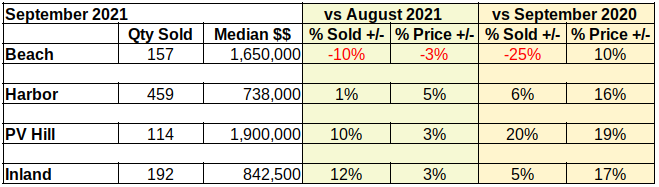

Compared to last month, overall sales increased slightly. The chart below shows that since March the number of units sold has remained relatively stable. Sales at the Beach were down 10% in September, while all other areas of the South Bay registered increases.

The number of Palos Verdes homes sold in September shows a strong 10% growth above August after remaining flat through the summer. That volume increase on the hill was over-shadowed by a 12% increase in the Inland cities. Sales volume in the Harbor area was nearly flat with only a 1% increase in activity.

Sales Prices Up in the Harbor

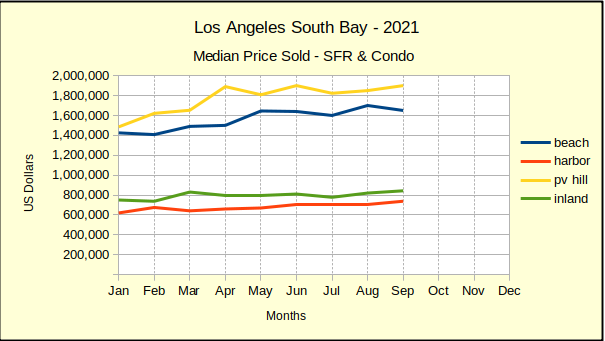

While the number of homes sold was low at the Harbor, median prices there increased the most of the South Bay. Harbor area prices in September were up 5% from the prior month. Prices on the PV peninsula rose by 3% as did prices in the Inland cities.

The Beach cities dropped into negative territory on pricing as well as volume. Median sold prices at the Beach were down 3% from August.

Looking back over the year, it’s interesting to note that the Inland and Harbor area home prices have remained close to level all year. Both areas have shown modest increases of about $100K, attained gradually over the year. By comparison, the median sales price in Palos Verdes jumped nearly $400K before levelling off in April. Similarly, median prices at the Beach climbed about $200K before stabilizing in May.

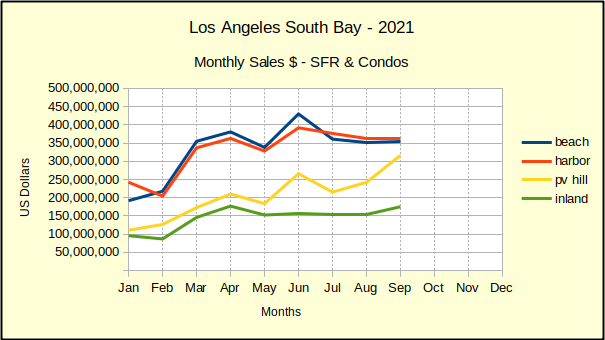

Area Sales Dollars Climbing in PV

Homes sales in the Palos Verdes cities increased in both sales volume and median price. Combined those increases catapulted the September sales dollars for peninsula properties upward by over $50M. This results from a trend we’ve been watching this year where median PV home prices are out-pacing Beach homes by $200K-$300K every month.

This is a change in the norm. In 2020, in the midst of the pandemic, median prices were close between homes sold at the Beach and those sold on the Peninsula. PV home prices were usually higher, but not always, and not by very much. In 2019, before the pandemic, PV and Beach median prices were nearly the same, with PV often having the higher number.

Statistics – by Month, by Year

We continue to ignore the comparison between the current month in 2021 versus the same month in 2020. The pandemic influenced statistics are too far from normal to show meaningful relationships. The current month versus last month is impacted also, though to a lesser extent. For example, monthly increases of 10%-19% in median price bespeak runaway inflation. Similarly, increases of 5% every month are not reasonable, nor are they sustainable.

We’ve had questions about median price versus average price–which is better and why. We use median, which is halfway between the highest and the lowest sale. Being at the exact midpoint tends to give a more accurate picture of the whole market, as opposed to an average, which can be more easily skewed by an abnormally high or low sale.

Pricing – The Highs and the Lows

It’s easy to fall into the trap of thinking that some neighborhoods are expensive and some are inexpensive. While that can be true of smaller geographic areas, most larger areas have a healthy amount of price variance in the available housing. Below we’ve included the highest and lowest rounded sale prices in the four broad areas we review.

Area Beach Harbor Palos Verdes Inland

Low Sale $475K $200K $470K $300K

High Sale $16.5M $2.6M $9.0M $2.3M

The prices shown are the extremes as recorded on TheMLS as of the third day of the month. We allow three days for agents, brokerages and the various multiple listing services to update records before we start our analysis.

One observation jumps off the page immediately. The variance in price is much more dramatic at the high end. The range among areas at the low end is from about $200K to $475K, a spread of $275K. Expressed in percentages, the high price is 237% above than the low.

At the upper end, the variance in price ranges from $2.3M to $16.5M, a spread of $14.2M. This time, expressed in percentages, the high price is 717% higher than the low.

So, what does $200K buy in the South Bay? This time it was a one bedroom, one bathroom “fixer” condo in downtown Long Beach. On the ground floor, with 580 square feet of space.

And $16.5M brings you six bedrooms, with seven bathrooms in 5715 square feet, a three car garage, a dedicated home theatre, and stunning ocean views from the Manhattan Strand.

Smart home technology has been around for a bit by now, but smart refrigerators are still a relatively recent addition. They can also be rather pricy. These two factors combined mean most people don’t have one. You may not actually know what features they have. Here are a few things it can do for you.

Smart fridges can connect to phone and television service. They have a built-in display that can be used to watch TV or videos, as well as audio services to play music or give reminders, such as alarms or notifications that the fridge is low on ice. Handy tools include a digital notebook, recipe lookup, and shopping checklists. There’s plenty that a smart fridge can do for you without you even opening the door.

With the foreclosure moratorium ending, the only thing keeping many homeowners in their homes is a forbearance plan. Once those end, the effects on the market could be drastic. The good thing is that it’s easy to predict when that will happen, since forbearance plans have a designated end date. Many of them have already ended in the past two months, but we will continue to see more ending throughout the rest of the year.

One of the effects of a large increase in foreclosures or forced sales is plain to see, and that is an increase in inventory. With inventory being so low right now, one could be forgiven for thinking that’s what the market needs. But it most certainly is not. Let’s take a look at the reasons demand is so high right now: low interest rates, and the fear-of-missing-out (FOMO) mentality that buyers have when inventory is low. Interest rates are going back up now, so that’s no longer an incentive to buy. If inventory increases drastically, FOMO won’t be a factor either. Foreclosures and forced sales will remove all incentive to purchase while increasing inventory considerably, causing a full swing in the market. But that’s not all. People living in foreclosed-on homes aren’t just statistics; they are actual people, and their increased economic struggles will only make it more difficult to reach a recovery point in the recession.

Gov. Gavin Newsom recently signed two housing bills into law, SB 9 and SB 10. SB 9 modifies areas zoned for 1 unit to also allow duplexes. However, it isn’t without restrictions — it also limits the construction that would convert a single home into a duplex to homes that have not been rented out in the past 3 years, and only allows 25% of the external walls to be demolished if it is a conversion and not a new construction. SB 10 is aimed at helping local governments to streamline processes for allowing up to ten units on lots formerly zoned for SFRs, but only if the lot is over 8000 square feet.

One region in which these bills were highly contentious is Long Beach, which has 59,803 single-family lots. But the laws aren’t likely to change things as much as people think, especially SB 10. Only 4,609 are eligible for the provisions under SB 10, due to the lot size restriction. Moreover, the City of Long Beach is under no obligation to allow up to ten units at all — the bill merely streamlines the approval process, should they choose to. A significantly larger number of units could be affected by SB 9, but city officials expect that between 17000 and 28000 units would be ineligible due to the rental restrictions, and there’s no guarantee that the eligible units would be converted. In addition, ADUs are already allowed, and the biggest difference between an SFR-plus-ADU combination and a duplex is the size of the units.

There are a plethora of articles about what to do before buying a home, especially for first-time homebuyers. But has anyone ever told you what you shouldn’t do? Of course, some of these are just a different way of writing the same things you’ve heard before. But others are advice you may not have been provided.

The biggest mistake to avoid is financing a big-cost item, such as a car, immediately before looking to get a home loan. Lenders will see that, and they’ll know you’ve just taken out a loan and will have debts to pay. That doesn’t look good for your credit score or your debt-to-income ratio. Similarly, avoid maxing out your credit card debt, even if it’s on many smaller items. It doesn’t even matter if your limit is low; what lenders look at is the percentage of your limit that is used. Another thing that may make lenders look more closely is a change of jobs. If you’ve simply moved from one company to another in the same occupation, you’re fine. But if you switched career paths or lost your job entirely, that looks like instability. All this advice continues to be relevant throughout the purchasing process — don’t make any big financial decisions until the transaction has closed.

Some other mistakes relate more specifically to real estate and not simple economic decisions. Many buyers neglect to get a preapproval before they start looking, thinking it’s a long process that they don’t want to get involved in before they find something. Yes, it does take time, but if you wait, that house you found may not be available anymore by the time the process is finished. Not only is this something sellers look for, preapproval will help you figure out what you can afford. It makes the search a lot easier if done ahead of time. Don’t try to expedite the process by just going to the first lender you find, though. The rates quoted in the news are always averages. Not every lender is going to have the same rates, and the rate isn’t the same for every situation. And contrary to popular belief, your personal bank doesn’t owe you the best rates just for being their customer. Once you know what you can afford, figure out how much your down payment is going to be. Don’t make the mistake of thinking it has to be 20% or more. That is frequently a good idea, since it avoids private mortgage insurance, but it’s still possible that paying the PMI and putting less down is a better financial decision for you. Plus, it’s almost never a good idea to put off buying solely because you can’t afford to put down 20%.

The 2021 housing market has experienced heavy competition from buyers, with most sellers receiving multiple high-priced offers. The peak was back in April, with nearly three-quarters — 74.3% — of listings generating at least two offers. While the numbers have been dropping off, with July’s percentage at 62.1%, it wasn’t until August that it fell just slightly below the prior year’s percentage for the month, at 58.8%.

The percentage is still over half, but that’s generally pretty normal. The current numbers are to be expected as far as seasonal variation. What’s even more indicative of a return to normality is the drop in number of offers and speed of sale. Agents are noticing decreases from 25-30 offers to 5-7 offers. In addition, a bit fewer offers are above asking price.

That’s just national averages, though. There are still some highly competitive markets, and the most competitive ones are actually becoming more so. 8 of the 10 most competitive markets actually had an increase in bidding wars between July and August.

A significant number of homes don’t have a basement at all, but there are more distinctions than simply whether or not there is one. There are actually three different methods of basement construction, and which method is used could affect durability and maintenance requirements. The three types of construction are concrete, block masonry, and precast panels.

Concrete basements are the most common and certainly have some advantages over the other types, but also have some disadvantages. Concrete basements are the most resilient, so are very unlikely to cave in. They are also fireproof. Though they are water resistant, they’re not entirely waterproof so it’s important to maintain the humidity levels and check for mold or mildew. A concrete basement will improve a home’s property value.

The least expensive type of construction is block masonry, composed of connected cinder blocks or masonry units. Unfortunately, that also means it has the fewest advantages. One thing it definitely has going for it is that it’s by far the most waterproof construction. Block masonry is still highly resilient, but for full durability it needs to be reinforced with steel rebar.

Precast panel basements, actually made in another location before being transported to the construction site, share some qualities of both the other types. Like block masonry, precast panels are waterproof, but like concrete basements, they require maintenance to stay that way. Precast panel basements can be susceptible to pest infestations, but this can be prevented with boric acid treatment. Fortunately, the individual panels don’t have any issues with resilience; it’s only the joints that need to be maintained.

Title insurance is one of those additional costs of purchasing a home that, unlike many other fees, is actually optional. Most people don’t want to deal with additional fees and ignore title insurance. That’s not necessarily a good idea. If you can afford to pay the fee, it’s a good investment.

There aren’t very many options available for homebuyer protection, and title insurance is one of the best. Title insurers have the best access to records and most experience detecting problems of any form of homeowner protection. Fraud is on the rise in the electronic age, and title insurance protects the homeowner from both fraudulent claims and losses. You may also not realize that title insurance, unlike most forms of insurance, is just a one-time charge. You won’t be saddled with monthly or annual payments.

There are many similarities and also many differences between the current recession and the Great Recession of 2008. Two of the core similarities — and the ones that define a housing bubble — are that prices are accelerating faster than purchasing power, and that there are changes in consumer values. While legislation and shifting values have addressed some of the issues that contributed to the Great Recession, most notably subprime lending, ultimately the crisis was a relatively natural economic response to the events that triggered it and followed a normal boom-bust-rebound cycle. The 2020 recession is somewhat of a reflection of this, though the specifics differ. The economy was already headed towards a natural downturn in the cycle, but the process was sped up by the COVID pandemic.

That’s where the similarities end, though. While nearly everything is ultimately tied to the economy in some way, it’s the pandemic, more so than economic conditions, that prompted valuation changes. Preference for larger homes and home entertainment, rather than homes closer to work and out-of-home entertainment, will probably continue as long as work-from-home remains a common practice, which will likely last a while. It’s true that people are leaving large cities and moving to cheaper areas, but this is more so out of necessity than desire. Peoples’ tastes have actually become more expensive, even if their wallet isn’t any larger. An economic downturn wouldn’t prompt this behavior. The only reason this isn’t currently sustainable is that the market hasn’t recovered yet. Once it does, probably around 2024-2025, it’s likely that the bubble will slowly deflate rather than explode.

I’m sure some of you haven’t heard of the term bioprinting. It’s a relatively new concept, combining stem cell research with 3D printing to print biological matter. Earlier this year, ribeye steak was printed using this method in Israel. The latest development out of Japan is a more complex cut of meat — Wagyu beef, known for its intricate fat marbling. The team at Osaka University has managed to perfectly replicate the look of Wagyu beef using 3D printed muscle and fat tissues, and their new methods provide a more accurate texture.

There’s still more research to be done, though. Though it certainly looks and feels like Wagyu beef, no one actually knows whether or not it tastes like Wagyu beef, or is even edible at all. More studies will be needed before the regulatory agencies in Japan will greenlight testing the cooking and consumption of bioprinted meat. In addition, the goal of sustainability is a long ways off with the cost of production being so high.

Fannie Mae keeps track of the Home Purchase Sentiment Index, or HPSI, each month. From July to August, the change in total value was negligible, from 75.8 to to 75.7, though it’s down 1.8 year-over-year. But the HPSI is a composite of six different categories, and none of them were without change. Three categories increased and three decreased.

Notable changes were an increase in those who believe it’s a good time to buy and a decrease in those who expect home prices to increase over the next 12 months. While the number who think it’s a good time to buy is still not a majority, it’s approaching a third at 32%. In July, only a bit less than half — 46% of respondents — expected home prices to increase. In August, this dropped to 40%. Only 24% of respondents believe home prices will decrease.

The Federal Housing Finance Agency (FHFA) established the First Look Program back in 2009, aimed at promoting neighborhood stability by facilitating occupation of real estate owned (REO) properties by owners. The program created a special time period during which prospective owner occupants, public entities, and nonprofits would have exclusive rights to purchase properties owned by Fannie Mae or Freddie Mac, before investors would have access. Until now, this time period was 20 days. On September 1st, the FHFA extended this period to 30 days. They deemed this move essential during a period of low supply, to reduce the level of competition prospective owner occupants have to contend with.

In July, the Pew Research Center conducted a survey that asked the following question: Would you prefer a community where homes are larger, farther apart, and farther from amenities, or smaller, closer together, and closer to amenities. The answer was 60% for the former and 39% for the latter. When they conducted a similar survey in 2019, before the pandemic, the numbers were significantly closer: 53% to 47%.

Because each of the two responses involves three separate categories, it may be difficult to tease apart which one respondents were most focused on, or if they were considering all of them equally. The survey didn’t ask that question, and it’s unclear why the three separate factors were lumped into one question. Still, we may be able to guess what changed since the pandemic. It’s already established that the advent of work-from-home has caused an increase in desirability of larger homes, with room for a home office, larger kitchen space, and additional personal entertainment space. For a time, lockdowns and increased reliance on delivery services also meant that people weren’t really going to stores or restaurants anyway, so they didn’t care how far they were. It’s possible that social distancing has conditioned people to want their homes farther apart as well, but this seems either unlikely or a negligible factor.

For a few decades, the average period of time that a family stays in their home before selling has hovered around six years. However, in recent years, this number has climbed up to around nine years. Why the increase, and what does this mean for the housing market?

There could be multiple factors contributing to the increase, but a couple are fairly easily understood. The market crash in the late 2000s led to a price decrease, which encouraged sellers to wait longer for home values to go back up. Even once prices starting increasing again, not everyone was confident in the stability of the market or their own personal economic stability. Another reason is that the largest market group is currently Millennials, who have a relatively low homeownership rate, in no small part due to various economic factors largely outside their control. Not being homeowners, they aren’t able to sell, so they have no impact on the average length of homeownership.

Average length of homeownership is an interesting statistic to follow, but since it hasn’t changed in so long, it’s not entirely clear what the impact could be. One could guess that it would have a negative impact on available inventory. This could be a problem for anyone looking to buy, but also could further contribute to increasing average length of homeownership for people who don’t actually want to stay in their current homes, but have no option.