The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

The percent of income put into savings on average fluctuates rapidly, but for the most part tends not to be subject to sudden large shifts. There have been a few notable spikes or dips across the decades, but nothing like the pandemic spike. April 2020 saw a record-breaking 34% savings rate, attributed to lower spending during lockdowns in tandem with stimulus payments. There was a second less major spike after the second round of stimulus payments.

The 34% rate was approximately double the record in prior years, which was back in the 1970s. That prior record was still only a 2% difference from the prior year. By contrast, in October of 2019, the personal savings rate was 7.2%, a 26.8% difference. The most recently calculated rate, in October 2021, was nearly identical to the pre-pandemic rate, at 7.3%. The savings rate has still been trending upward in the past couple of decades, though, after a relatively steady decline since the 70s, bottoming out in 2005.

Increased demand following the lockdowns meant that many people were eager to buy in 2021, especially first-time homebuyers, 85% of whom were renting at the time. Unfortunately, many of them weren’t able to because of heavy competition, with over 25% making an unsuccessful attempt. That hasn’t deterred most of them, though, with 72% of prospective first-time homebuyers expecting 2022 to be their year.

However, it’s important to note that less than 15% of those now looking to buy in 2022 were already looking in the beginning of 2021. That means it’s unclear whether they’re only recently planning a move to homeownership, or they deliberately avoided the highly competitive phase. It’s possible that they’ve only recently acquired the means to purchase, but it’s also possible they’ve had the money lined up and held off for a better time. In any case, optimism is strong among the current group of prospective first-time homebuyers.

Two-thirds of homeowners feel they spend a large portion of their annual income just on their house. For 54% of homeowners, it’s their single largest financial burden. Most homeowners are well aware that homeownership is costly, yet still worth the price. Nevertheless, just over a third are struggling more than they expected with the annual cost of things such as mortgages, property taxes, and maintenance.

Housing costs are also increasing over time, which is contributing to the unexpected struggles. Single-income households are certainly worse off, but even dual-income households are having financial woes. But the most significant contributor to unexpected costs is repairs and maintenance. It seems most homeowners simply don’t consider how much it could cost to maintain their home. However, even costs that are laid out ahead of time are causing more strain than people realize. Almost half of homeowners didn’t think HOA costs would be such a big deal.

Interest rates are by no means high right now, but they’ve been steadily rising and can no longer be considered low. Prices have also been high, but they’re predicted to drop dramatically, for a couple of reasons. First, inventory is opening up as foreclosure moratoriums and forbearance programs are ending. The other reason is that the Fed has been reducing their mortgage-backed bond (MBB) purchases. Tapering back MBB purchases will both lower prices and increase interest rates.

The Fed had previously announced plans to keep the Federal Funds Rate at its current value of zero through 2023. However, they’ve now decided that 2022 the year to begin returning to normalcy. With scaled back MBB purchases, the zero benchmark rate is the only remaining factor in economic stability that isn’t transitory. Increasing the benchmark rate will further increase interest rates, though, so 2022 is going to be a year of higher interest rates, but lower home prices.

Water leaks or burst pipes can be disastrous and unpredictable, but many homeowners don’t know how to maintain their plumbing. Obviously, a plumber could do a lot more than the average homeowner, but you can still do your part to help the pipes last longer. Long-term stress is the primary cause of plumbing issues, so reducing their work load is the most effective preventative method.

Most people enjoy high water pressure when showering, and may even upgrade to a higher pressure system. But higher water pressure means higher pressure on your pipes. They will slowly start to wear down. If your water pressure is higher 80 psi, consider hiring a plumber to lower it. The $300-400 expenditure is a sizable sum, but still far less than the cost of a water leak. Another thing that can damage the pipes is having a lot of minerals in the water. Think about purchasing a water softener, which will also improve the effectiveness of your washer and dishwasher. They are expensive, though; a good water softener will cost about $500. One method that doesn’t cost you anything at all is to simply avoid pouring grease down the drain. It may seem like liquid grease will pass through easily, but it solidifies as it cools and can clog the pipes over time.

There are several options to decorate your windows. Some of them also help maintain privacy. The most common is window curtains, but there are other things you can do to make your windows more stylish.

If your window isn’t in a location that necessitates privacy, such as the kitchen, try putting some plants on the windowsill. A traditional valance performs a similar job, but you can also use painted wood or metal to achieve the same effect. For more privacy, consider frosted glass. It lets in more light without being see-through, and doesn’t need to be fiddled with. If you’re the more traditional sort, you can opt for pull-down shades, which aren’t as commonly used nowadays but do the same thing as curtains.

While it’s now legal to build multiple units on land previously zoned for single-family residences (SFRs), the cost of construction is still high. The costs of acquiring a site, making sure to conform to environmental codes, and building from scratch definitely add up. Builders aren’t able to work out a positive return on investment for new constructions.

They can cut a lot of the costs by using existing structures and renovating them. But, many of these structures are zoned for commercial use only. There are certainly zones that can be commercial or residential as needed, but not nearly enough to satisfy buyer demand. New zoning laws in the Los Angeles metro area and in the San Francisco Bay Area have facilitated conversions from commercial to residential, but even that isn’t enough. And in areas without these new policies, such as the San Diego and Sacramento metro areas, conversion rates are dramatically lower.

The rising cost of lumber has been mentioned a few times, mostly in the context of slowed construction rates. But lumber costs aren’t the only issue, and it’s affecting more than just construction. The pandemic and subsequent recession were the primary driving force for supply chain difficulties across the board, and climate change is also a big player.

Though lumber prices are still relatively high, they are actually much lower than the peak in Q1 of 2021, and the number of construction workers, while still below pre-pandemic levels, isn’t far off. Where there are still issues are in other sectors. Paint and furniture are more expensive than ever. Part of the increased cost of furniture is the still-high lumber prices, but it’s mainly the result of extreme weather — Texas was the main contributor to raw materials to produce paints and furniture stuffing before cold snaps and hurricanes halted much of the production. Paint and furniture are also both in high demand as a result of people spending more time at home and therefore wanting to remodel. The same trend has resulted in an ever-growing backlog of home appliance deliveries.

Out-of-state purchases are becoming more common, with improvements in remote showing technology as well as increased popularity of the work-from-home model. People have even been purchasing sight-unseen, and requesting remote closing processes. Remote transactions may not be what you’re looking for, but regardless of your reasons for buying in another state, being prepared is even more more important than usual.

While big-name real estate agents are big for a reason, it may be more beneficial to choose a local agent for the area you’re looking in. They will be more intimately familiar with the area. Don’t be afraid to ask them questions, especially about the area’s transaction process. You may think you’ve been through it before, but it could be different in another state. Even if you’ve been to the state before, a local agent will likely know more than you. Not just the agent, either — ask the locals questions as well.

Many homeowners don’t want to consider renovations unless they plan to continue to live there, or the home is in dire need of upgrades. After all, part of the return on investment is emotional. But there are some relatively inexpensive upgrades that can boost your home’s value immediately.

Instead of committing time and money to replacing floors and countertops, update some less permanent fixtures. Replace mirrors and light fixtures, making sure they coordinate with the space and with each other. Professionally cleaning the floors often does just as good a job as replacing it for a much lower cost, especially if you have carpet. While higher end models can be expensive, new appliances won’t necessarily break the bank and will definitely be appreciated by buyers.

The most commonly used benchmark rate to determine mortgage rates has long been the LIBOR, or London Inter-Bank Offered Rate. However, this has some issues. The LIBOR is not tied to actual transactions. Because of this, bankers that have influence on the LIBOR can simply manipulate the rate to their benefit. This occurred in the 2008 recession, where the LIBOR was kept artificially low to encourage people to borrow money. The financial world has finally decided LIBOR won’t cut it as a benchmark, and it’s being phased out.

Financial institutions won’t be forced to stop using the LIBOR, but if they do use it, they will be required to include at least one rate that isn’t LIBOR-based as a backup. They will have until the end of 2021 to comply. The front runner for a backup rate in the US is the SOFR, or Secured Overnight Financing Rate. This rate is administered by the New York Fed. It’s not subject to the same manipulation that LIBOR is because it does take into account actual completed transactions. Fannie Mae and Freddie Mac already swapped from LIBOR to SOFR in 2020.

We’re seeing more potential signs of economic recovery as housing affordability is trending slightly upward from the second quarter. This is measured as the percentage of people that can afford a median priced California home, which was valued at $814,580 for the third quarter. The overall difference is small, an increase of only 1% — from 23% to 24% — but the upward trend holds across 30 of the 51 counties tracked (California has 58 counties total). Affordability is still down from 2020 numbers.

The county that showed the largest increase was already the most affordable California county, Lassen County, increasing 6% from 62% to 68%. There was also a 5% increase in Contra Costa County, from 26% to 31%. Contra Costa is also in a region that experienced an increase in affordability across every county, the San Francisco Bay Area. The least affordable county remains Mono County, but even in that county there was a 4% increase in affordability, from a measly 9% to 13%. The sharpest decline in affordability was felt in Siskiyou County, dropping 3% from 44% to 41%.

Nearly two-thirds — 64% — of homebuyers in the US don’t consider climate change in assessing the safety of the property they plan to buy, according to a recent survey. More and more areas are becoming prone to wildfires or flooding. Of course, some of them don’t believe in climate change at all, accounting for 12%. But just over half of the people not thinking about climate change simply failed to consider it, but recognized the value in doing so. 19% of respondents are aware of climate change but didn’t think it relevant to their homebuying decisions.

There’s plenty of evidence that the younger generations, Millennials and Gen Z, think about climate change and consider it a significant issue. But apparently, mostly in a broad sense, and not specifically in relation to home buying. It is important to note that most of those in Gen Z are not old enough to buy a home yet, and therefore wouldn’t be included in the survey. Only 10.6% of respondents considered climate change to be a top priority in homebuying decisions. For 5.9%, it was the most important consideration.

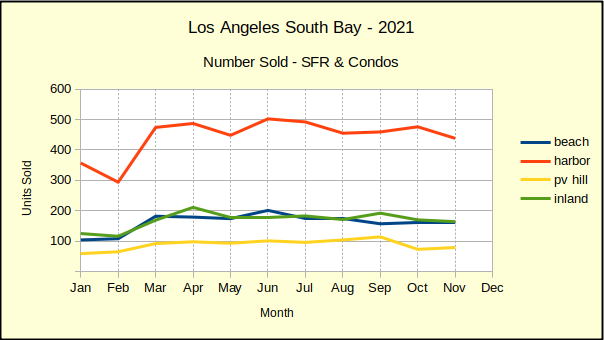

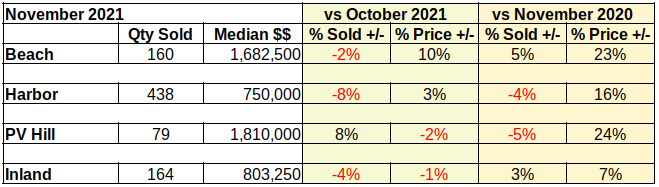

Real estate sales prices in the Los Angeles South Bay for November were mixed on declining sales volume. The declining volume is to be expected, given that we’re entering the slower winter selling season. Even SoCal slows down a little bit in the winter.

Another obvious impact is coming from the economic disruption of the coronavirus pandemic. The appearance of the omicron variant just as we begin year end celebrations has struck a fearful chord among more vulnerable segments of the population. So there are multiple reasons for the number of units sold to drop as it has for most of the South Bay.

Statistics show Palos Verdes as the only area to have an increase in sales for November. Looking more in depth, we discover this is actually the second month in succession that PV sales volume has been well below the 2021 average of 89 units monthly. September sales were exceptionally good at 114 units sold, then October plummeted to 73 before coming back up to 79 in November.

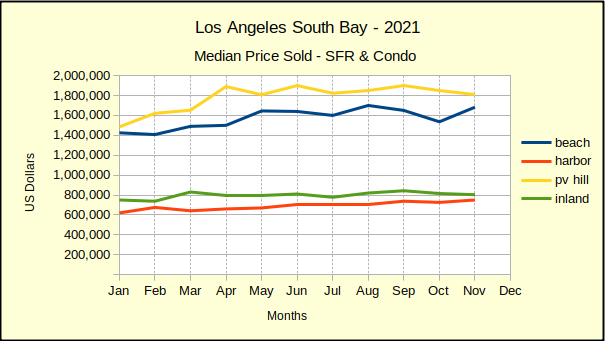

Median Price Mixed

Changes to the median price ranged from -2% in PV to +10% at the Beach. The +10 percent at the Beach makes up for price drops in September and October. Sales prices have been relatively stable since March in all areas.

It’s important to remember that the number of homes in the Beach cities and on the Palos Verdes peninsula is quite a bit smaller than either the Harbor or the Inland areas. The smaller sample size causes sharper and more dramatic looking movements in the charts.

We expect to end the year 2021 with strong price appreciation. However, early forecasts for 2022 are coming in with warnings about downward pressure on prices as a result of an anticipated increase in short sales and foreclosures. Because lenders were prevented from processing evictions during the pandemic, homeowners who were not able to pay their mortgage are now facing possible refinance, short sale or foreclosure. Some sources expect 3-5% of next years sales to be “distressed” transactions.

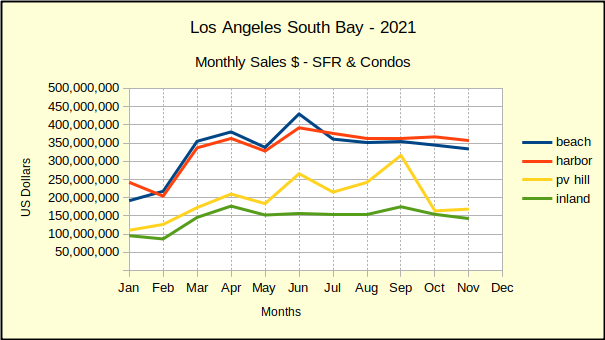

Monthly Sales Dollars

Cumulative dollars per month of residential sales started the year way down on the charts. Home buyers and sellers alike were at a loss as to where the pandemic was going and sat still. March brought activity back to the real estate market as sales–and sale prices–raced upward.

As the chart shows market conditions bounced up or down through most of the year as the public mood shifted with the ebb and flow of Covid-19 surges and successes.

As we near the end of a rocky, uneven year we’re seeing the monthly sales numbers settle into a more rational pattern. It’s the winter season, so the minor drop-off in sales we see in the charts is to be expected. December should be slightly lower, giving us a gentle end to 2021.

The Stats

Year-to-year statistics for the first half of 2021 were essentially useless because we were comparing “apples to oranges.” The first quarter of 2020 was “business as normal” and the second quarter was significantly reduced as the pandemic brought sales activity to a near halt.

By the second half of 2020 protocols for showing and selling property became established and business started returning to something close to normal. Mortgage interest rates were still under 3% creating solid motivation for buying and selling. And there were more buyers than sellers resulting in bidding wars and rapidly escalating prices.

Much of that activity slowed when the the “winter surge” of Covid hit. Homes were still selling, but at a slower pace from October through February of 2021. Then March and warmer weather arrived, which combined with the increasing number of vaccinated individuals, put the real estate market into overdrive.

Compared to last year November shows the number of sales slower in the Harbor and PV Hill areas, while sales have picked up at the Beach and Inland. Though sales are slower, the price increases have abated very little. Home affordability is slated to become even more of a problem than it has been in LA.

Conducting an energy audit involves checking the home for areas where air could be leaking in or out. Much of the time, this is left to a professional. But it doesn’t have to be. Even if you don’t have the proper tools to fix the leaks, you can certainly conduct an audit yourself and determine whether anything needs to be fixed in the first place. Plus, if you do have the tools or can acquire them, the fixes don’t require a professional either.

All that testing the walls requires is a candle and a way to light it. Bring a lit candle with you as you tour any exterior wall, door, or window. If the candle goes out or starts wavering while you’re not moving, it probably means air is coming in. You can fix the leak yourself with caulk if you find one. Besides exterior walls, doors, and windows, other areas you should check are the attic and ducts. You don’t need a candle for this, but you’ll want a mask and gloves for protection. Lift up insulation in your attic to see if there is any lack of coverage, and fill it with additional insulation before sealing it. Check the ducts for holes, and also check the joins to make sure they’re airtight. Ducts can also lose heat if they’re not clean.

Rent control is highly contentious. Certainly many of its opponents are landlords who stand to lose the most financially. But even among those who agree that something needs to be done to help tenants, rent control isn’t a popular answer, since it seems to do more harm than good in practice by encouraging landlords to exploit legal loopholes to evict tenants — or even just evict them illegally, which is rarely contested in court.

It’s no surprise, then, that the vote to enact rent control in Santa Ana was hotly debated. The final vote was 4-3 in favor, but even the four council members that approved it all admitted it isn’t an optimal solution. The saving grace is that the measure also includes tenant protections. The opposition’s primary contention was that the measures aren’t too different from the existing statewide regulations, making it a largely redundant venture whose implementation and enforcement would be a waste of city and taxpayer money.

The labor force has been unhappy for quite some time, given that wage growth continually fails to meet inflation levels. What has been holding workers back from quitting en masse is that they don’t have anywhere to go. Unstable finances, mostly due to that same lack of wages, means many of them would rather keep a job they don’t like than risk being unemployed. During lockdowns, about 3 million people quit, but many of them were forced to — people normally don’t want to quit during recessions because the economic climate is too unstable. This year, even without being forced, over 4 million have left their jobs.

In many ways, this was actually spurred on by the pandemic. School closures are still happening in some areas, and they’re not necessarily predictable. That means families need to either find a way to pay for childcare or quit their job to take care of the children themselves. For some, it’s the stimulus payments plus the trend towards economic recovery that allows people to be more confident in risking temporary unemployment. In addition, older at-risk individuals are retiring early to reduce exposure. Employers are starting to reopen positions that were cut during lockdowns, and are desperate to fill them, offering higher pay and more benefits — though still not a living wage in many cases.

Looking for investment property is a bit different from looking for a personal home. There are a considerable number of factors when purchasing a personal home, such as affordability, whether it suits your needs, proximity to work, schools, and shopping, and whether you actually like the space. But with investment property, while you probably won’t be getting much return on your investment if no one wants to live there, it’s not your own preferences you should be looking out for.

Ultimately, investment property does come down to your bottom line, and finding something you can afford and that has a good return on investment is certainly very important. But it’s important to realize that your return on investment is partially determined by others’ preferences — which means you need to know what they are. Research the market area and figure out trends. Which types of homes are selling, and to what type of clientele? Also, don’t discount remodeling. It may have a higher up-front cost, but if it does, the return on investment is sure to be high as well in the long term. You may even find it’s actually cheaper to buy a home in need of care and remodel it into something similar to existing homes.

Zillow launched its Zillow Offers program back in 2018, in which Zillow would purchase homes directly to update and relist. This process is called flipping, and is a fairly common strategy. Within California, Zillow Offers was available in LA, Riverside, Sacramento, and San Diego. Unfortunately for Zillow, they weren’t actually very good at it. Their investment efforts turned out to be losses, and as a result, they are now eliminating the program.

That may not even be the end of the problems for Zillow. The reason they struggled to flip homes? Their home value estimates, called Zestimates, are not very accurate, something which real estate professionals — but not the general populace — already knew. Zestimates are a major offering of Zillow, and if they wanted anyone to trust them, they’d have to use their Zestimate as a baseline for home values. But that led to losses, as Zillow ended up purchasing homes for more than they sold them for. Their gamble didn’t pay off, and now their poor estimating algorithm has been exposed anyway.

Sellers have a tendency to overlook buyers who are expecting to get a VA loan, since they think VA loans are more likely to fall through. But deals involving VA loans actually have a higher rate of success. It’s not difficult to qualify for a VA loan if you meet the basic requirements. There’s still the issue of convincing the seller, but there are things you can do to help with that.

Consider working with a lender that specializes in VA loans. Expert guidance can help both the buyer and the seller truly understand what a VA loan means for their prospects. In addition, while VA loans don’t require any down payment, it’s a good idea to put money down anyway. This makes the deal look better to the seller, and ensures that they won’t assume you lack the money to cover a potential difference in appraisal vs sale price, which VA loans don’t cover. And of course, making a better offer will always appeal to a seller. It may not skyrocket you to first choice, but you’ll be in better contention.