The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

Many people are still delinquent on rent payments as a result of the recent recession. Some relief came in the form of emergency rental assistance (ERA), which also required landlords take additional steps before being able to evict for nonpayment. The additional protections were set to expire on March 31st, but there was a last minute change to the law.

Under the new regulations, while the protection will still only apply to delinquencies on rent payments owed before March 31st, it will now continue to apply to those delinquencies through July 30th if the ERA application is still being processed. Tenants will still owe rent for April and subsequent months, even if their ERA application for earlier payments is still being processed.

Spring tends to be the hottest season for the real estate market, which means heavy buyer competition, especially while inventory is still recovering. These tips, including some lesser-known ones, can help you stay in the running.

It’s not unusual for homes to be listed low in order to garner interest. While this may not be necessary with higher demand than supply, it’s good to know that you may want to look lower than your expected budget. Even if an offer is accepted near the list price, that just means you have a bit extra for repairs or updates. Alternatively, you could put it towards a higher earnest money deposit, which shows the seller you’re actually serious. Getting an actual approval letter, and not just a pre-approval, will do the same thing.

There are also a few contract terms you can change to appeal more to sellers. A good agent can advise you on matters related to your current situation to see which contract terms are best for you. These include various waivers, particularly an inspection waiver; a lease-back for sellers who are also prospective buyers; and a relatively unknown thing called an escalation clause. An escalation clause, also called an escalator, lets the seller know as soon as they receive your offer that you are willing to increase the offer if outbid, and defines an upper limit. This can prevent a situation in which the seller sees your offer, sees an offer higher than yours, and accepts the higher offer, without realizing that the higher offer is actually lower than what you are willing to pay.

What buyers want and what they’re able to get isn’t always the same thing. Buyers nowadays are frequently settling, due to high prices. However, their search keywords are a decent indicator of what they want, even if it’s just wishful thinking. And what they want right now is outdoor living, except from the comfort of their home.

The number 1 most searched home feature is a swimming pool. In fact, buyers currently seem rather obsessed with water. If they can’t get a pool or hot tub, many are happy with a view of the water, and it doesn’t necessarily need to be an ocean view. The second most searched term is a view of rivers, and beaches, waterfronts, lakes, or really any kind of water is a popular view. Buyers are also looking for other types of outdoor amenities, such as horse facilities, boating facilities, golf, tennis, and basketball. And of course, they search for a large lot or outbuildings to accommodate all these features.

Tax season is upon us. You may have already started working on your taxes. But perhaps you haven’t thought about everything you may be able to deduct. Some of the most significant costs of homeownership can be tax-deductible.

Many people are aware that their property taxes may be tax deductible — if you didn’t, well, now you do. But did you know that the interest on your mortgage always is? Your lender should have this line separated out, so it’s easy to find and deduct from your taxes. Another homeownership cost that is sometimes tax deductible is home repairs. Significant repairs are probably tax deductible. Be sure to check with a tax professional to determine which of these you can actually deduct. They may even be able to find more tax-deductible expenses you weren’t thinking of.

With home prices as high as they are, qualifying for a loan becomes more difficult. This is especially true if your household is single-income. But that doesn’t mean it’s impossible. There are options available for low-income households.

As always, it’s important to check your credit score before attempting to get a loan. You can check it for free once per year from any major credit bureau. If your credit looks good enough to qualify for a loan, you can advance to searching for loans. For low-income households, the best place to look is government loans, since these usually have lower thresholds for down payments. Some FHA loans require only 3.5% down. Your specific region may also have government loan programs. If your credit score is low, however, consider looking for a co-signer for your loans. The co-signer doesn’t necessarily need to be the one paying, but if their credit score is better than yours, it will help improve your chances of loan approval and possibly even get you a lower interest rate on the loan.

Realtor.com has released their Best Time to Sell Report for 2022, and the predictions land on April 10-16. Spring is usually a hot season for the real estate market, and this year is no different. Demand is going up, prices are still high, and inventory is still low. Homes are already selling quickly after listing.

It’s not going to last for too much longer, though, which is why the window is so small. Mortgage rates are increasing, which will reduce buyer demand or cause them to look for lower priced listings. Inventory is also starting to recover as construction is accelerating. Also, if you are planning to sell in order to buy a new home, keep in mind that the best time to sell is frequently not a good time to buy.

Multigenerational homes are becoming more common recently. But what exactly does that mean? And why? A multigenerational home has a rather simple definition. It includes any home in which two or more generations of adults live in the same building. This doesn’t include children, but children can be present as well.

Common examples of multigenerational homes are parents of young children living with the children’s grandparents and adult children moving in with their parents. The former is frequently in order to give parents some extra help raising their kids. Moving back in with your parents, or vice versa, can be done for a couple reasons. A common one is recent college graduates wanting to have a place to stay while they pay down their student loans. Sometimes older parents move in with their children because they need help taking care of themselves.

There are two main reasons to refinance your home. One is to reduce your monthly payments in order to free up cash, and the other is to pay off the loan more quickly. But refinancing doesn’t just simply do this automatically; you have to choose a new mortgage with terms that work for you. Figure out what your goal is and pick the right mortgage.

Reducing your interest rate is the surest way to free up cash, but it can also simply be used to pay off the loan faster. With a lower interest rate, a greater percentage of the principal is reduced each time you make a payment. However, this only works if you can qualify for a lower interest rate. If you don’t qualify normally, consider reducing the length of the mortgage. This will probably result in higher monthly payments, but will also likely allow you to qualify for a lower rate, and almost certainly allow you to pay off the mortgage faster as long as you make the payments. If you have plenty of cash on hand and just want to save money in the long run, consider replacing your mortgage with one that allows you to make larger payments on your principal. This is more costly in the short term, but would allow you to pay off the loan early and thus spend less on interest, reducing the overall cost.

Sellers who haven’t done their research, especially first-time sellers, are prone to certain errors when selling their home. Many of these involve wanting to get as much money as they possibly can. What sellers don’t realize is that they may need to either temper their expectations or spend some money to make money. Besides these sorts of issues, sellers also sometimes don’t have a new place lined up for themselves for when the sale goes through, which can cause them to spend unnecessary money on temporary rentals.

Especially in a hot market, sellers tend to overprice their homes. It’s true that prices are high right now, but listing your home at exactly market value isn’t going to draw attention. List lower, and let market competition do more of the heavy lifting. More competition also means more serious offers, but do keep an eye out for offers that seem too good to be true — they probably are, and would be a waste of time. Time is something you don’t want to waste when trying to sell your home, since interest will wane and home values may change. The best offer isn’t necessarily the highest offer, either; look at contingencies and down payment percent as well.

“For sale by owner,” or FSBO, can be tempting because it cuts out the middleman. If sellers don’t have to pay an agent, they keep more of the profit. Seems simple, but as it turns out, their profit will probably still be higher with an agent representing them. Agents have better marketing tools, more experience with pricing and staging, and the ability to host open houses or get in contact with photographers and videographers to create virtual tours. FSBO sellers can decide to do these things themselves, but the cost comes out of their pocket, so they don’t manage to skip out entirely on costs.

Prices are still going up, as are interest rates. Despite this, the market is currently going strong. It’s unclear whether this is temporary or seasonal, or part of a larger trend, but the near future of real estate is looking fairly good.

The reason for the rate increase is a recent increase to the federal funds rate of 25 basis points. The initial announcement didn’t have an immediate effect, but later caused an increase in interest rates. This, in addition to rising prices, has contributed to a decrease in home sales. However, it’s still above pre-pandemic levels, and supply is improving, which should help keep prices in line.

Part of the reason for supply increases is increased construction. Though construction actually decreased in the Western US, it has increased elsewhere and is at its strongest since 2006. Builders remain confident despite a slight drop in confidence, from 81 to 79, due to increased costs.

Kids can complicate the process of moving. Young children may not understand what’s happening, or just not understand the reasons why. Older kids that know what’s going on may simply have strong emotions about significant life changes such as this. Parents wish they could do something to make the transition smoother. Well, it turns out they can: Involve the kids in the process.

A large factor in kids’ reluctance to move is that they feel a lack of control. It’s simply something that’s happening and unavoidable, rather than something they’re doing. Take them to open houses with you, so they can familiarize themselves with their potential new homes. Ask them to help pack — you may think your kids aren’t going to want to be given tasks, but if it helps them feel like they are an actor rather than observer, they will feel more in control. Hosting a goodbye party for the kids, and not just for adults, can also help to add closure.

The process doesn’t end with moving out. There is more to do after moving in. Unpacking is just as important as packing. Let them help choose paint colors and the arrangement of furniture, especially in the room that will become their new bedroom. Once you’ve settled in the new house, go meet your neighbors, and take your kids with you.

Some property owners don’t like the idea of allowing pets on their property. However, it’s probably a good idea to consider offering a pet-friendly rental property. 72% of renters own pets, so pet-friendly rentals are in high demand. This ensures you’re more likely to find a tenant and also allows you to charge more for rent. You can also ask for a pet deposit, in addition to the normal security deposit.

You also shouldn’t be too worried about property damage. Yes, pets can cause minor damage to property, but it’s actually more likely that costly property damage is caused by young children or even adults. In addition, you can reduce property damage by replacing carpets with linoleum, vinyl, or laminate floors. These are more resistant to damage and easier to clean. It may also be a good idea to install pet doors and gates.

WalletHub examined 182 of the largest cities in the US in an effort to answer the question of which cities were the happiest. Their research focused on various aspects of emotional and physical well being, income and employment, and community and environment. As it turns out, their data suggest that California could be a very happy state. 6 of the top 10 ranked cities are in California. This includes Fremont, which was the number 1 ranked city, as well as San Francisco, San Jose, Irvine, Huntington Beach, and San Diego. The other four cities in the top 10 were Columbia, MD; Madison, WI; Seattle, WA; and Overland Park, KS.

However, these results should be taken with a grain of salt. WalletHub never directly asked anyone whether they were happy or not, though their methodology does include –among many other criteria — a few clear correlations, such as suicide rates and depression rates. Their data may be accurate, but the conclusion that their data points to happiness is up for debate. In addition, the focus was 182 of the largest cities. It’s entirely possible that the happiest places are not large cities, or even cities at all. Not to mention California has a huge advantage in this regard, since it is very large, is almost entirely urban, and makes no legal distinction between cities and towns. California therefore has far more cities analyzed by the data than any other state, at 28. WalletHub’s selection criteria did include at least two cities per state, but many states only use data from those two cities.

Many people are blindsided by rising mortgage rates after getting a preapproval, thinking that the preapproval has locked their rate. It hasn’t. The first opportunity to lock your mortgage rate happens when your final loan application is approved, though you don’t even have to lock it until shortly before closing on a purchase, if you think rates will go down. In addition, the lock period is not indefinite. It usually lasts anywhere from 15 to 60 days, and it could definitely take longer than that to find a home.

There are ways to mitigate the issues presented by shifting mortgage rates. Rates don’t tend to change much during a typical closing period, but you want to lock early when rates are rising and late when rates are falling. Consider budgeting for a loan lower than your preapproved amount in order to account for fluctuations in mortgage rates. Different lenders also have different locking policies. Make sure to shop around and ask about lock periods, renewing options for locked rates, and the possibility of locking out rising rates but not falling rates.

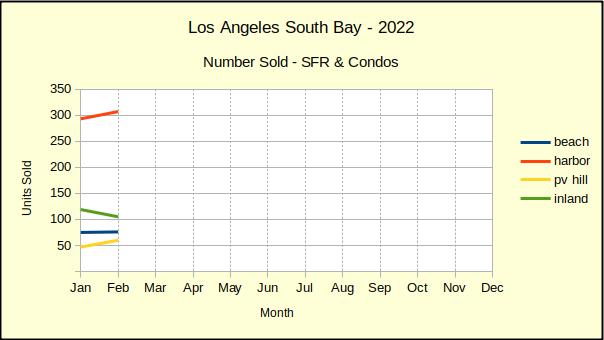

February sales data carried a surprise for South Bay residents. With fewer monthly sales than last year, the median price for PV homes sold has made a huge jump. The average number of homes sold on the Hill in 2021 was 88, and December recorded 87 sales. January saw 47 sales and February 60. At the same time the sales volume was dropping, the median sales price jumped by over 33%! (Details at Median Prices below.)

Sales in the Harbor area were up 5% from last month. Increased real estate activity and prices in the Harbor have been anticipated for some time now and are gradually coming to fruition. The multi-billion dollar investment in the West Harbor commercial development has spawned a number of smaller development projects throughout San Pedro. On the east side, Long Beach has been steadily adding infrastructure across much of the city. The net result is improved real estate markets across the Harbor area.

The number of homes sold in the Beach cities was essentially flat with 75 sold in January and 76 in February. This is however significantly down from the average monthly sales of 159 units in 2021, and from the December sales of 132 units. In a unique twist, the drop in sales volume is a return to sales numbers we were experiencing before the Covid19 pandemic.

In a further shift downward, Inland home sales dropped off from an average of 168 in 2021 and a total of 160 homes sold in December. January fell to 119 and February fell again to 105 homes sold. A modest decline in sales volume is expected during the winter months. Once again, as we saw at the Beach, we’re seeing the same return to pre-pandemic numbers for Inland home sales. One could almost think things are normal again.

Median Prices Going Up, Up & Up

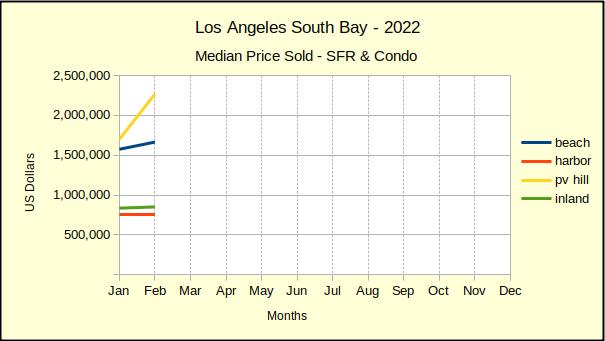

Take a look at what’s happening with PV prices. That yellow line on the chart below shows an explosion in median prices on the Hill. Pre-pandemic, the median was just under $1.5M. January it was $1.7M–February it’s $2.3M.

We found that 19 newly constructed residences have been sold at the Rolling Hills Country Club development over the past six months. Those homes sold for a median price of $4.1M, boosting the median dramatically and adding $80M to cumulative sales for the Hill.

The median for Beach cities home sales is up $100K from January and stands at $1.6M, up from the pre-pandemic median of $1.3M. Harbor area and Inland prices are similarly up showing signs of a pending correction from the overly enthusiastic bidding wars of the past couple years.

We anticipate a leveling of the median prices across the South Bay, with the exception of unique circumstances like new construction at the Rolling Hills Country Club. As the Federal Reserve Bank increases interest rates, some buyers will drop out of the market. Sales are expected to slow while time on the market expands and prices contract.

Cumulative Home Sales Dollars

We wrote above about the steep yellow line for sales on the Hill. If nothing else, adding $60M to the monthly sales total should serve to demonstrate that if someone will build homes, they will sell.

The Beach and Harbor areas are both up about $20M over January numbers. Although slower than it was last year, the demand for housing is still strong.

Inland total sales dollars are down $6M for the month of February. Occasionally we see February sales totals drop from January, however it’s rare. We suspect the sales decline for the Inland area is a harbinger of the future for all of the South Bay.

The Statistics

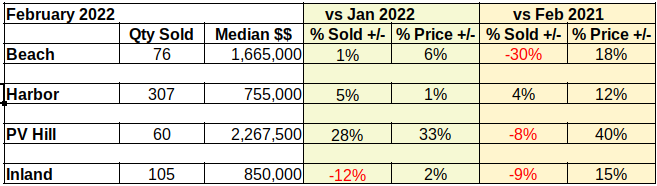

As usual we’ll close with the statistics for last month as compared to the prior month and compared to the same month last year. The negative numbers (red) will quickly show that Inland home sales declined from January to February. Glancing at the other areas, we can see the Beach area volume was a mere 1% growth, while the Harbor showed strong sales and PV went through the roof compared to prior month.

Three red blocks jump out comparing to February of 2021. This is not surprising considering we were well into a panic buying season this time last year. This is reminiscent of most months in 2021 when we were able to only compare to the prior month because of Covid-contaminated statistics.

The strong Harbor area performance stands out here. A 4% gain over last year versus a 30% drop in volume at the Beach is certainly something to watch next month!

Some routine expenses may not seem like they’ll break your bank individually, but they aren’t just one-off expenses, and there’s often a cheaper way. You may notice these things more easily if you record your budget in a spreadsheet. This is a good practice for tax season anyway, and it could open your eyes to a whole lot of unnecessary spending.

Many people start their work day by grabbing a cup of coffee from someplace like Starbucks or a donut shop, then at lunch time, pick up a ready-made sandwich. Both of these things can be done at home. It takes more time, but it doesn’t have to get in the way of your morning, and it’s far cheaper. The coffee machine can be prepped at night and turned on when you wake up, and you can prepare and bag a sandwich in the evenings as well. You can also probably save on groceries by creating a list and sticking to it. Impulse buys are not uncommon, and while you may simply start adding some of these items to your list, they probably won’t all make it there. Another cost saving measure, this time unrelated to food, is ditching cable service. Streaming services can cover the same channels for a fraction of the cost.

The results of a November 2021 survey of real estate professionals about the 2022 forecast are in, and they’re rather split. 41% expect prices to continue to rise and 41% expect them to fall. The remaining 18% predict prices will remain about where they are. Keep in mind, though, the survey was conducted a few months ago and may not reflect experts’ current beliefs. In addition, all of those who predicted continued rise in price conceded that the rate of increase will probably be slower.

There are a few factors pointing to slowdown, whether it’s a decline or a slower rise in home prices. Interest rates are increasing, which decreases buyer demand and buyer purchasing power, pulling down prices. The job recovery is still lagging behind. Forbearance exits mean greater inventory. Even global events are threatening to destabilize the economy, and uncertain buyers makes for less frequent buyers.

Most people who have been paying attention to real estate are aware that the construction industry has been struggling lately. But there’s one area where the industry is doing just fine, and that’s townhouses. Townhouse construction dropped in 2020 along with everything else, but it’s already recovered and is now above pre-pandemic levels. It seems townhouses are simply in fashion right now, as they feel like single-family homes — and are considered as such by some categorization methods — but are generally less expensive.

The truth is a little more complex, though. In reality, townhome construction has been on the rise for about a decade, and 2020 was merely a small dip — which also happened in 2011 and 2012. Perhaps townhome construction specifically was largely unaffected by the most recent recession, and this is just a continuation of the trend. It was actually the Great Recession in the latter half of the 2000s that caused townhome construction to plummet, and it’s been steadily recovering ever since. It’s not quite back at 2006 levels, slightly lower than the 2005 peak, but it’s not far off.

Almost everyone has a few smoke detectors and a fire extinguisher somewhere in their home. If you don’t, you definitely should, and are required to by law in California. Unfortunately, that’s as much care as many people take in their fire safety. That may not be enough.

Smoke detectors should be spaced around your home so that they can be heard regardless of where you are. California requires smoke detectors in certain areas of the home. This includes every bedroom, every hallway that leads to a bedroom, and at least one per floor in a living area. Check to make sure that you are conforming to code, and that your smoke detectors have working batteries. If your home is large, you may also want to consider additional smoke detectors above the minimum requirements to cover more area.

Homes are only required by law to have one fire extinguisher. However, this is the bare minimum and not ideal. You want to have easy access to a fire extinguisher regardless of where you are. The suggested number is one per floor. If you live in a multi-family building, every unit should have easy access to a fire extinguisher. This doesn’t necessarily need to be inside the unit, if there are hallways with access to multiple units. But having just one for the entire building isn’t a good idea, even if there are only a few units.

Technology has made it easier than ever to secure a tenant for your rental property, as long as you’re making good use of the technology. There are several websites that you can use to help spread the word about your listing. Some of these are websites you may use already for other purposes, and others are specific to real estate. You can even create your own website, though you’ll have to make sure people find out about it.

There’s a number of websites that allow you or your agent to list properties for rent. There’s the local MLS, which would need to be accessed by your agent, but this will also spread to aggregator sites like Zillow and Redfin. Alternatively, you can post to Zillow and Redfin yourself. Other similar websites include Zumper, HotPads, and ListHub. Make sure to verify the information after a property is listed, since automated systems can get things wrong. In your descriptions, include certain frequently searched keywords, like the school district, amenities, area, and some basic features.

Email campaigns still work, but it’s not the only way to expand your reach. Social media websites are excellent at this. It’s especially necessary if you’ve created your own website. The obvious ones include Facebook and Twitter. perhaps less obviously, you can post pictures or videos of your property on Pinterest and Instagram. You can also reach out to your network on LinkedIn.