The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

With the current market’s low inventory and high prices, buyers are struggling to find entry-level or starter homes. There is one type of home they can afford to buy, though: fixers. These also aren’t in high demand, so competition isn’t as fierce. The problem is, first-time homebuyers typically don’t want to spend extra or can’t afford the additional cost of fixing up their homes. But that can be resolved with home renovation loans.

Two common home renovation loans are the FHA 203k loan and the Fannie Mae HomeStyle loan. Both require a minimum credit score of 620 and a minimum down payment of 3%. They cover most home improvements, including both structural and cosmetic. However, keep in mind that the FHA 203k loan can only be used for primary residences, while the HomeStyle loan can be used for both primary residences and investment property.

An increasing number of people are seeking ways to contribute to the environment. While a single person isn’t going to suddenly solve the climate crisis, every little bit can help. Planting gardens improves air quality and also gives you access to fresh fruits, vegetables, or herbs, while also slightly improving your energy efficiency. Some other energy efficiency upgrades can also significantly reduce your annual costs.

Everyone knows about solar panels, and you may even have already upgraded to solar energy. But there are other solar energy upgrades you may not be aware of. There are solar attic fans and solar water heaters as well. If you haven’t upgraded to LED lighting yet, you definitely should. LEDs are massively more energy efficient than regular lightbulbs, which translates to much lower utility bills. They also last longer, so you won’t need to spend money on replacements as often. Even windows have gotten energy efficiency upgrades. Energy efficient windows combined with good insulation reduces the workload of heating and cooling units.

The idea of open concept living used to be pretty hot, but it’s started to cool down recently. Shifting trends in usage have made open concepts less useful to most families. That doesn’t mean the advantages have disappeared; they’re just not in high demand right now. This is mainly a result of COVID-19, which has made the advantages less appealing and the disadvantages more salient. Ultimately, though, it’s a personal choice.

But what are these pros and cons? The biggest con is noise. Open concept floorplans have fewer walls and doors to muffle sounds from other rooms. With more people transitioning to work-from-home, the added noise is distracting people from their work. In addition, having lots of empty space is just not a priority for most people. Yes, people want larger homes, but that’s to accommodate more usable space, not empty space. The biggest benefit of open concept living, and the reason it rose to popularity, is that the wide open spaces with good natural light allow for excellent entertainment spaces. However, the pandemic had drastically reduced the appeal of hosting indoor events. What it does still accomplish is creating a feeling of togetherness, even when family members are in different rooms.

New constructions are always built to certain specifications, whether that’s tract uniformity or client’s wishes. In the latter case, the client is usually also going to be resident. That’s starting to change, as investors are noticing that renting is becoming a lot more common as prices rise. Investors are now getting new constructions built for the express purpose of renting them out.

Only 3% of new construction SFRs were build-to-rent in 2019. By the end of 2021, this number jumped to 26%. It’s not entirely clear if this will continue to increase or not. While increased inventory of rental properties does benefit renters, renting is rarely a desired state. Almost everyone would prefer to buy if they can afford it. But it’s not renters pushing the trend. It’s the investors, and they stand to benefit as long as renters must continue to rent, whether they want to or not.

Buyers rarely find exactly the perfect home for them. There’s always something that isn’t quite what they wanted. But how do they decide what they’re willing to give up? Well, it’s different for everyone, because different buyers have different needs, and their decision may not actually be the best they could make. What can be tracked is statistical likelihood of certain decisions.

The most frequent concessions are age or condition, size, and style. Location is typically extremely important and not something most buyers want to budge on. While many buyers don’t want complete fixers, they may settle for homes with natural wear and tear due to age. Larger homes are becoming more popular, but the main attraction is more rooms. For many buyers, the rooms don’t actually have to be very big, as long as they’re big enough to serve their purpose. Style of a home does have some importance, since some styles may be more popular and fetch a higher price when you eventually go to sell it. Since you won’t know what will be trending far into the future, though, style is ultimately cosmetic. Many buyers are perfectly content ditching their preferred style for something that better suits their practical needs.

Especially if you are a first time buyer, buying a home can be an exciting prospect. Unfortunately, that excitement can lead you to overlook potential problems. Slow down and make sure you know what you’re getting into, otherwise you may regret your purchase. On the bright side, there are a few things you can do to curb potential issues.

Possibly even before looking at homes in an area, you’ll want to get to know the area itself. Visit the neighborhood to learn about the local amenities and maybe meet potential neighbors. When inventory is low, you may be tempted to look at homes that are slightly out of your budget. While this can be a good way to find homes that are overpriced, if it turns out the home is actually out of your price range, don’t think too much about it. Stick to what you know you can afford. But that doesn’t mean go looking for dumps that are well below your price point. Even if you’re a DIY type of person, fixers are a big job and frequently more trouble than you’d expect.

Another thing you don’t want to get involved with is large bidding wars. Even if you eventually win the war, it likely came at the cost of paying more than you intended. It may not be worth the cost anymore. Getting involved in homes that are selling fast also doesn’t give you time to really think about the properties. It could be an excellent deal for someone, but that someone isn’t necessarily you. When you do find a home you like, don’t rush to make an offer immediately. If you think you’ll run out of time, that also means you’ll probably run into a bidding war. Instead, take your time, look at other properties, then come back and look at that property again. You may find you missed some details that could be a dealbreaker.

In many regions, the weather during much of the year is not very conducive to outdoor living. Which is why many people like to introduce elements of nature into their home with a few houseplants. That’s all fine and well, but with the weather warming up, what about introducing your home into nature?

Instead of bringing plants inside, plant a garden outside. If you don’t have a large enough plot of soil, you can plant a container garden. That way, you can grow your own herbs and vegetables. Your garden becomes an extension of your kitchen. You can make it even more of an outdoor kitchen by cooking outdoors as well. The easiest way to do this is by grilling, but there are even outdoor stoves, ovens, and sinks. The kitchen isn’t the only room you can bring outside. An outdoor patio doesn’t have to have outdoor furniture. You can put a couch, coffee table, and even a TV outside and create a new outdoor living room. Since you probably don’t want to haul these back inside when the weather cools down again, you can invest in a patio covering.

Student debt is becoming a huge problem, for both those affected by it and the economy as a whole. Wages are stagnant and tuition is increasing. The UC system has also increased its tuition, but recognizes that it’s simply not sustainable with their current financial aid program, as students aren’t able to afford to attend.

As such, the UC has made a couple of changes, with the end goal of a debt-free education by 2030. First, some of that tuition increase is actually going toward student aid. Currently, 33% of the UC system’s revenue is allotted for student aid. The Board of Regents voted to increase this to 45%. Second, they’ve changed their prioritization order for student aid. Student loans are above student employment in the ranking right now. The new priorities shift part-time student work above student loans, and in fact, all students will be expected to have at least 15 hours per week of work. The eventual goal is also going to be dependent on the state’s debt-free grant that has, so far, only been partially funded.

Moving fraud has increased recently in the wake of the work-from-home relocation boom, nearly doubling from 2020 to 2021. Fortunately, moving fraud is actually fairly easy to detect if you know what you’re looking for. Most of the things you can look out for aren’t necessarily indicative of a fraudulent company, but probably wouldn’t be the case with a good company. Major red flags involve legal requirements not being met or legal information not being provided, and almost surely indicate fraud.

Very importantly, the company must provide a copy of Your Rights and Responsibilities When You Move. This is a legal requirement. Included in this document is the requirement that moving companies only collect money for successfully delivered items, meaning demanding up-front payment is illegal. Moving trucks are also subject to FMCSA regulations. If they aren’t willing to provide their FMCSA registration, they probably aren’t registered and therefore not operating legally. The company should also provide contact information, including an exact address, and you should be able to find them online.

There are also less surefire red flags. As usual, “if it’s too good to be true, it’s probably false” applies. Scammers offer low prices to entice customers, but frequently add hidden surcharges or fees, or simply bump up the cost well above their estimate — if they provide one at all. They may say they’ve been around forever, but they may not have any proof of that. Especially if all their reviews are recent. If they’re all five star reviews, they’re probably all fake. Scammers are also frequently very pushy.

Prospective buyers tend to cancel viewings on days of unexpected rain. This makes sense, as most people don’t want to be out in the rain. However, a sudden downpour may actually be an opportunity. If you’re able to tolerate the weather, rainy days are actually the best day to evaluate a home.

Water damage can be extremely expensive to repair. But how are you going to know whether or not a home is prone to water damage? Well, by looking at it in the rain, of course. After rainfall, the water is naturally going to run downhill. If you see water running towards the house, that’s a potential problem. You can also watch for signs of pooling or flooding, especially with waterfront properties, and try to spot leaks before water damage occurs. Sight isn’t the only sense you can use; mildew has a more pronounced smell in the rain. There’s also a bonus advantage — the fact that many people don’t know all this, meaning you’re going to have less competition.

When you’re trying to buy and inventory is low, it may seem inevitable that sometimes there simply isn’t anything available that suits your needs. If this happens to you, it may be that you need to expand the scope of your search. This doesn’t necessarily even mean broadening the range of acceptable homes, but rather looking for them in a different way. There are a couple different options for doing this.

The first option is looking at different media. Many homes are listed on a Multiple Listing Service (MLS) and can be easily found by your agent or on an aggregator site such as Zillow. Off-MLS sales aren’t common, but they do happen. And they’re becoming more frequent with the increasing popularity of social media sites. You can potentially find listings on sites such as Facebook or Twitter. The other is to look at old listings or listings slightly outside your price range. Often these will actually be one and the same. Overpriced homes tend to sit on the market longer because no one wants them at the current price. But that also means there will be less competition, so you may be able to offer below asking price, even in a generally competitive market. Even if the listing isn’t old yet, you can keep tabs on potentially overpriced listings and see if the price drops or it hangs around for a while.

Moving to a new area and not knowing anyone there can be an awkward situation. Some people are social butterflies and will be eager to get to know their neighbors. Others may need a little help. Here are a few suggestions to break the ice.

The most forward approach is to simply go up and knock on their door. Not everyone is going to answer the door to strangers, but you may be able to entice them. Consider bringing a gift of homemade cookies or any other dish you know and love. If you don’t want to take the situation to them, you can instead invite them over. Throwing a housewarming party is a great opportunity to invite all your new neighbors, or you can suggest a block party. For the less socially inclined, there’s an option that doesn’t require contact, but can build up familiarity over time. That is taking walks around the neighborhood and simply greeting people you happen across. If you have a dog, there’s a good chance you’ll do this anyway, but it could just be part of your exercise routine.

When buying a new home, you should not always expect that you’ll stay there forever. This is especially true for first time buyers, who often need to buy a starter home first before they can build up enough equity to buy a forever home. But sometimes it’s the right call. Keep in mind that you don’t actually have to live in your forever home forever; it just means that you could see yourself doing so. And a starter home doesn’t have to be your first home; it can be a middle stage on the way to your forever home. Neither is a binding commitment.

So when should you buy your forever home, and when should you buy a starter home? Starter homes are generally less expensive, and are something you plan to sell later. If you immediately purchase a new home after selling, you may be able to avoid capital gains tax. It’s an investment for the future. The downside is that they’re generally smaller. If you are planning to have kids soon, a smaller home may not be big enough, and moving frequently can be hard on kids. But that isn’t the only factor in determining if you should buy a forever home. Even if you could see yourself living there forever, that doesn’t mean it’s financially sound. More expensive homes will also have higher mortgage payments, taxes, and insurance fees. You may want to consider it, though, if you are able to secure a low interest rate.

Finding the right neighborhood can be difficult. You probably don’t know everything about a neighborhood you’re about to move to. Your agent may know more, but won’t know as well as you quite exactly what you’re looking for. But there are certain factors that are important for most everyone, and many of them can be researched objectively.

Everyone wants to feel safe in their community. No area is entirely without crime, but crime rates can give you a good idea of how safe you will be. The websites Neighborhood Scout and Crime Report can give some in-depth details. You should also look at transportation options and commute time. This includes not just your job, but also shopping, amenities, and schools. Not everyone is going to have the same needs in this respect, but everyone will want their specific needs met. Another important factor is the people in the community. It’s near impossible to judge them without going there, but you don’t have to be living there. You can visit community centers or even just knock on doors. Some people aren’t going to answer the door to strangers, but if that’s an important factor in providing a sense of community, that can also inform your decision.

Accessory Dwelling Units (ADUs) have been contentious for a while, but SB 9 has passed recently, ostensibly making them easier to construct in California. Unfortunately, this hasn’t panned out as well as expected, as local governments aren’t entirely on board. They’re trying to sidestep the requirements by introducing zoning ordinances that effectively, but not explicitly, ban ADUs. Zoning restrictions have always been the largest obstacle to ADUs.

What clearly isn’t much of an obstacle is popular support. Particularly in California, major cities are seeing support of over 70%, even up to 80% in San Jose. But California isn’t the only state. Nationwide support is at 69%, with the remaining 31% split between opposing and indifferent. It’s no surprise that more renters than homeowners support it, since they’re more likely to be searching for housing. But both groups show strong support — 76% of renters and 66% of homeowners.

While we can all agree that high prices and low inventory is not a recipe for a healthy real estate market, reversing the trend too quickly can cause issues as well. Prices are predicted to start declining towards the end of 2022 and throughout 2023 and 2024. This may be good for prospective homebuyers, but it’s not good for sellers who purchased relatively recently.

A sharp decline in prices could result in negative equity for some people looking to sell, meaning that they won’t be able to sell normally and may have to go into foreclosure. This is not the same type of recession that we’ve just experienced, but it’s a recession nonetheless. Fortunately, it’s not likely to result in a crash, since the continued low inventory is a positive for sellers. The market is expected to begin to stabilize in 2025, but not without steep economic losses.

In a normal year one would expect April to be the turning point for the LA real estate market. March is still cold and the children are still in school for another 10 weeks. April’s the month when the weather turns warm, the flower buds poke up, and the buyers come out to start the spring buying season. It hasn’t happened that way this year.

Prices had gone through the ceiling by the end of 2021, much of the activity stimulated by fear of escalating mortgage interest rates. Usher in 2022–January and February were typically slow and in March home sales bounced up like an indicator of business as usual. But, interest rates continued to climb and April ended with the total number of home sales down instead of up. Likewise, total sales dollars were down across the South Bay.

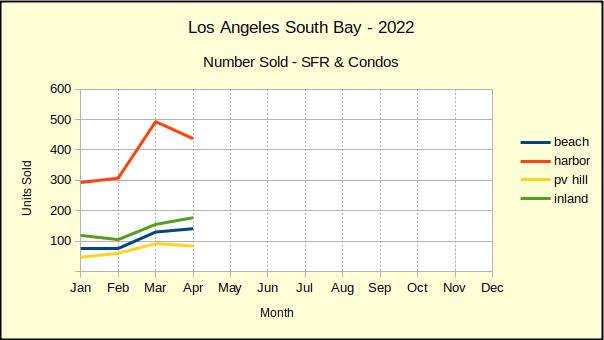

Number of Homes Sold

Judging from the charts, entry level homes in the Harbor area were clearly the center of activity for South Bay real estate. As interest rates pushed against the 5% mark, panic set in among first time buyers who had been outbid multiple times. Prices went up as high as buyers could afford, a number that shrinks amazingly fast with each tenth of a percent increase in the interest rate.

Across the South Bay, the number of homes sold in April dropped by -4% from March, which had been an increase of 59% over the prior month. As we see from the chart below, sales were uneven between the various areas.

On the entry level front, at the same time Harbor area home sales were dropping off, Inland homes gained sales. On the high end, sales on the Palos Verdes peninsula were also facing declining numbers, while Beach area sales increased.

So far declining sales counts have been modest, but a decline overall, coupled with a decline in half of the individual areas covered indicates that buyers are pulling back. Part of the resistance is a matter of simply being priced out of the market. Another important piece is the anticipation of price corrections in the near future. We have heard multiple buyers say they are watching and waiting for lower prices later this year.

At this point we’re well into the second quarter of the year and it looks as though those folks may be on track for some savings. even some of our most gung-ho pundits are beginning to see a market downturn on the horizon.

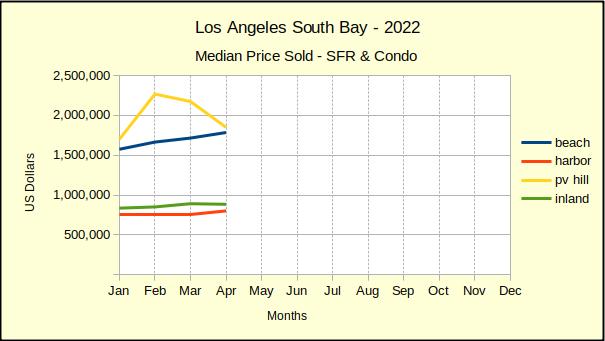

Median Price Sold

Interestingly, Harbor area prices went up at the same time the number of sales went down.The March to April price increase was a modest +6% compared to a +21% increase over April of last year. Similarly, the Beach cities had a month over month increase of +4%, while showing +19% year over year. While sales prices are still rising in those areas, the increase is a fraction of what it was last year.

Sold prices on the Hill continued to slide downwards. Because the February increase in the median price was created by the sale of new construction, and that building phase is now sold out, a downward turn in median price is expected. We anticipate that leveling off soon.

In the Inland area the median price for homes sold during April of 2022, was +12% greater than sales in April of 2021. By comparison, the median price of those sold in March of 2022 versus April of 2022 decreased by -1%. It’s a modest decrease that points to the direction of the South Bay real estate market for the balance of the year.

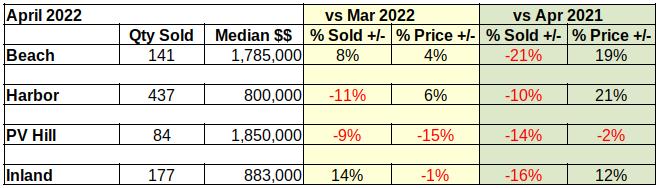

Area Sales Dollars

The total dollar value of home sales in the South Bay usually tracks right along with the number of units sold. The few times it differs are important times like these when the number of homes sold is dropping, and/or the sales prices are dropping. Today, of the four areas we track, PV Hill has a declining number of sales, both in comparison to last year and in comparison to last month. As we noted above, the area also is declining in total dollars compared to last year and last month.

As we discussed in last month’s issue, some of the reason for the drop is found in new construction homes that sold at a much higher price than the typical Palos Verdes resale home. The rest of it can be found in longer days on market waiting for a buyer, and in price reductions.

At the opposite end of the spectrum, the Beach cities showed gains last month for both number of units sold and for the total sales value of those homes. The only decline this month for the Beach was in number sold compared to April of last year. Sales this April were off by -21%.

The Harbor area still trended upward in dollar value, both month over month and year over year. But, the number of units sold was down for both time measurements. The price competition was very stiff in what is generally an entry level market. During the past couple years, bidding wars and over-asking sales prices have kept the dollars high. The April numbers show that changing rapidly.

Total dollar sales for the Inland community increased 15% month over month. That was the highest growth of all four areas. Scanning those individual transactions showed an odd pattern. Sales in the price range from about $325K up to about $750K were a familiar mix of some under asking price, some at asking and some above asking. The degree of variance was about what one would expect. Unexpectedly, for sales over $750K, nearly every property sold above asking price, and in many cases well above asking.

We found no clear explanation for why this phenomena occurred. There is a suspicion that buyers who were priced out of Beach properties may have shifted their bidding wars into the increasingly popular parts of west Torrance. This theory is supported by the distribution of sales among the various neighborhoods.

In Summary

In the table below are the core statistics comparing April to March of this year, and comparing April of this year to April of 2021. The prevalence of negative numbers is convincing evidence that high prices and high interest rates are pushing the South Bay real estate market into a recession.

Notable Properties

One of the more interesting properties sold in April is a four bedroom, five bathroom home located in west Torrance. The home was purchased by the seller as their family home in 1990 for just above $360K. The children grew up and the parents remodeled in 2022 and sold the house.

As would be expected in a good neighborhood with a contemporary remodel, the home sold for over the asking price of $2.7M. The final selling price was slightly over $3M. and just happened to be almost exactly $360K over the asking price.

In the 32 years that family owned the home it appreciated at an average rate in excess of $84K per year. It’s the classic “American Dream.”

With home prices on the rise, young adults are experiencing struggles paying for a home with just their own income. As a result, cohabiting is becoming more common, in which unmarried partners –or possibly just friends — choose to pool their money and purchase a home together. Some may be concerned that this can cause some financial headaches. But really, all you need to do is make sure you know your cohabiting partners well.

Marriage certainly confers some legal and financial benefits. As far as purchasing a house, though, the financial side of things doesn’t actually care whether you’re married or not. Relationship status is not a factor in mortgage rates, as every co-purchaser’s financial history is considered separately, whether they are married or not. However, this also means that if you don’t really know a partner’s financial history too well, you may be in for an unwelcome surprise. It’s also important to note that even after successfully purchasing the home, conflicts between co-owners can result in situations not too dissimilar to divorce proceedings, even if you aren’t married.

Fannie Mae was sued back in 2016 under allegations of fair housing violations, and the organization decided to settle in February of this year. The settlement amount was $53 million. Fannie Mae had acquired a large number of properties in the wake of the subprime mortgage crisis, and thus became responsible for their maintenance until they were sold. But fair housing organizations started to notice a trend: only the ones in predominantly white neighborhoods were being adequately maintained.

The settlement agreement was the first to determine that foreclosed properties, like the ones Fannie Mae holds, are also subject to fair housing laws. This was not officially determined prior. Also, it’s possible that they were in worse conditions to begin with, but that doesn’t absolve Fannie Mae of their responsibilities. Their argument was that their intentions were not discriminatory. Perhaps they simply were not able to maintain the homes as well since they were in worse shape. But they were unable to reject the claim that regardless of their intentions, the impact was obvious. This is what led to Fannie Mae needing to settle.

With mortgage rates on the rise, more and more buyers are struggling to obtain loans. Given this, an infrequently-used financing option is starting to make a comeback. Seller financing is an process in which the seller of a property offers to carry the mortgage, and the buyer will then owe the seller rather than a lender. This doesn’t have the same stringent requirements that mortgage loan approval has, so it’s much more accessible to buyers.

Seller financing tends to be attractive to buyers. Not only is it more accessible, but the interest rate is usually lower. It also doesn’t incur any fees such as loan origination fees. But why would a seller want to do this? Well, there are a couple reasons. Firstly, because seller financing is so attractive to buyers, it can improve the property’s marketability. There’s an additional benefit, though. It allows the seller to defer part of the taxes on sale profits. The seller only pays taxes on the principal as it is received. At the time of sale, they pay taxes on only the amount the buyer paid. This can include the down payment and any partial loans the buyer received.