The original BeachChatter discusses the housing market in the coastal communities south of the city of Los Angeles. Some articles are peculiar to a single city. Some discuss the region as a whole. The focus is on privately owned housing.

Two more bills aimed at increasing multi-family construction go into effect July 1, 2023 after Governor Newsom signed them into law in September. These are AB 2011, called the Affordable Housing and High Road Jobs Act of 2022, and SB 6, the Middle Class Housing Act of 2022. Both laws sunset nine and a half years later, on January 1, 2033.

AB 2011 adds a secondary review pathway for some multi-family construction projects. If the project meets affordability standards and site criteria, the review will not take into account conditional use permits or environmental impact reports. The site must be primarily commercial, and unless it’s a commercial corridor, 100% of the units must be below market rate. Even if it is on a commercial corridor, 15% of the units must be below market rate. AB 2011 also includes provisions for fair pay and additional training for construction workers. SB 6 expands the types of buildings that can be constructed in areas zoned for office, retail or parking. These buildings may be residential if they meet certain other criteria, many of which are similar to the requirements set forth in AB 2011.

The State of California sets housing goals for every city in the state. Many cities, particularly more affluent ones, frequently decide to simply not meet these goals, as it doesn’t really benefit them to do so. Their only incentive to follow through has been what is termed the “builder’s remedy, ” which requires cities with no plan submitted, or that fail to meet their goal, to permit any and all housing as long as at least 20% of it is affordable housing.

This law has actually been in place for about a decade, but it hasn’t been easily enforceable. Recent changes have made it more enforceable, so now cities have to start thinking about it. Not all cities have the same deadline for submitting plans, but there are already 124 cities in Southern California that are out of compliance. Northern California has until January to submit plans.

Opendoor is an online real estate business based in Arizona that buys directly from sellers instead of going through the market process. While nothing about skipping the open market is illegal, the problem comes from Opendoor’s claim that its service saves sellers money. As it turns out, this claim is entirely false.

Opendoor claimed that those who use their service save money because they will be selling at market value with reduced transaction costs. There’s no evidence whatsoever that these claims are true. In fact, there is evidence that many sellers who go through Opendoor actually net thousands of dollars less than they would on the open market, despite cutting out the middleman. As such, the Federal Trade Commission voted unanimously, 4-0, to approve a final order against Opendoor. The final order requires Opendoor to pay $62 million in consumer redress, prohibits them from making deceptive, false, or unsubstantiated claims, and requires them to provide evidence of their claims.

Construction has had multiple ups and downs in recent years as a result of the pandemic and surrounding economic factors. Throughout it all, multi-family construction has actually done pretty well. In fact, it’s currently at its highest rate in the last fifty years in terms of total number of new multi-family constructions. Unfortunately, that doesn’t mean it’s high — construction has been in a slump for the past thirty years, and meanwhile the population has been increasing.

Los Angeles has it the worst of any US metro, underproducing by about 400,000 homes. This is despite the fact that it’s also one of the top metros for multi-family construction. In large part, this can be attributed to the fact that it is the second most populated metro in the US. But the real issue is restrictive zoning laws, which are only recently being changed in California. The vast majority of homes in the Los Angeles metro are single-family residences because that’s what the lot’s zoning allows.

After the pandemic forced many employees to work remotely, it was initially unclear how long the remote work trend would last. Some thought everyone would return to the office after the pandemic was over. Some saw that remote work was actually working surprisingly well, and expected fully remote jobs to rise in popularity. The latter has definitely happened, however, employers’ attempts at a gradual return to office work have caused another trend to emerge: the hybrid work model.

It turns out an office has benefits and so does remote work. And this is true regardless of an individual’s preference, if they had to choose just one. So why not get the best of both worlds, and just go into the office sometimes? This will be great for workers — though not for owners of office buildings. Those who held onto the office space they owned may have expected a full return to office work, which would result in a return to normalcy for the office building market. What is happening in reality is a gradual reduction in office space. Office space isn’t being eliminated completely, since it’s required for a hybrid work model. But companies won’t need nearly as much office space, and are already making plans to repurpose the space they already have.

One of the offerings of the Department of Veterans Affairs is mortgage loans. Of course, this is limited to current or past members of the US military. With this restriction comes a few significant benefits if you qualify. VA loans have perks for both low-income and high-income homebuyers.

If you have the money to buy a more expensive home as long as you can get a loan, VA loans may have you covered. There are jumbo loans available which can even exceed $1 million. This may be a good bet even if you are not currently a high-income earner, as long as you are purchasing investment property. This is because there is no minimum down payment for VA loans; you can borrow up to 100% of the home’s value. You don’t even need to worry about private mortgage insurance (PMI), which is required for conventional loans with a down payment under 20%, but not for VA loans regardless of your down payment amount. If your investments pay off, or you start earning more money, you can also pay off the loan faster. VA loans have no penalty for accelerating payments.

Insuring your home against natural disasters can save you quite a bit of money in the event such a disaster occurs. Frequency of different types of natural disasters varies by region. While this is also true of floods, floods can occur pretty much anywhere, so flood insurance may be worthwhile regardless of whether you are in a flood zone or not. So what do you need to know about flood insurance?

Flood insurance is not legally required. However, some mortgage lenders may require it, especially if the property is in a flood zone. As can be expected, flood insurance premiums are higher in flood zones, since there is more risk. That also means it can be relatively inexpensive if your area is not flood-prone. Since floods still occur at a significant rate in such areas, it’s probably a good deal even if the lender doesn’t require it. If you do get flood insurance, whether you chose to or your lender asked for it, make sure to compare plans. Premiums vary by company, and most companies have more than one insurance policy. Most policies cover damage to both the building and the contents of the home, but you should check to make sure. Some plans also include replacement expenses.

If you’re selling your home, or getting ready to do so, you may have thought about some of your prospective buyers’ potential questions and what the answers would be. Many of these probably relate to the home itself or the neighborhood, and can be expected questions. However, some not so uncommon buyer questions are decidedly more bizarre.

Perhaps not entirely unexpected is the question of whether or not there have been infestations, and it’s a common one. This would obviously be a major concern for a buyers, but be prepared for buyers to be overly concerned about certain unlikely infestations. Buyers may ask about pests that don’t even live in your area. Another very common question that may seem a bit silly to some people is whether or not someone has died in the home. Certain superstitious buyers may think this means the home could be haunted, which would be a major turn off. You may not even know yourself whether someone died there or not if it happened a long time ago, but buyers like this will still want to know. A less common death-related question, though perhaps one grounded more in observable reality, is whether anything was buried in the home’s yard. It’s not uncommon for people to bury their pets in the backyard, but buyers or their own pets may not want to unearth something like that.

It’s long been suggested that one should put down at least 20% of the purchase price as down payment. While this is probably a good idea if you can afford it, many people have taken this advice a bit too much to heart, and are reluctant to try to buy with a lower down payment amount. A third of homebuyers even think it’s a requirement to get a loan.

In reality, most loans have a much lower minimum down payment, with one of the most common types — FHA loans — having a minimum of just 3.5%. Some even have no minimum. In addition, the median down payment is significantly less than 20% for first-time homebuyers at 7%. It’s higher for repeat buyers at 17%, but that’s still under 20%. What’s more, there’s a good chance you can get homebuyer assistance to help cover the down payment. While a majority of homebuyer assistance programs are specific to first-time homebuyers, over a third of the approximately two thousand programs do not have this restriction.

Investors are frequently asking whether the current investment market is better for stocks or real estate. Usually, there’s a correct answer. Right now, the best answer is probably not to invest at all. When this happens, it’s called a hold phase. Real estate being both a less volatile and more long-term investment makes it a slightly better method of investment during a hold phase, but it’s still likely better to hold off until home prices reach a bottom, which is likely to be around 2025.

Stock price movement is a bit harder to generalize since it changes so much more frequently than real estate prices. This is mostly because stock trades can be initiated and completed near instantaneously, while home sales typically take a few weeks between listing and accepting an offer. That said, it’s clearly evident that stock prices are on a downward trend right now, with an annual change of -17%. Until this bottoms out, it may be too risky to invest. Home prices, on the other hand, increased 12% in the past year. Normally this would make it an absolutely terrible time to invest in real estate, and it’s certainly not a good time to do so, but home prices are now decreasing. Better investment opportunities in real estate will crop up in a few years.

Much of the danger to tenants is being unable to pay rent, as both rental prices and cost of living continue to increase while the job market is still in recovery. However, that isn’t the only way tenants can get evicted. There are even a few ways landlords can legally evict tenants that haven’t done anything wrong. That isn’t enough for some landlords though, who are actually resorting to illegal methods of eviction instead of notifying the tenant and potentially going through the court process.

Though both are legal, the court process distinguishes at-fault and no-fault evictions. At-fault evictions are the category where failure to pay rent lies, and this category also includes various contract violations and criminal activity while on the premises. The no-fault category includes landlord’s intent to occupy the property, withdrawal from the rental market, property being deemed unfit for habitation, or landlord’s intent to demolish or substantially renovate the property. Some of these can be used misleadingly as the landlord can simply change their mind later, but the real problem is unlawful evictions. The Office of the Attorney General (OAG) is particularly concerned with the type known as self-help evictions. This includes the landlord shutting off utilities, changing locks, or removing the tenant’s personal belongings in order to force them out of the property. Landlords initiating a self-help eviction can get charged with a misdemeanor, and the sentence is either a fine or a jail term of a maximum of one year.

Home staging is one of the best ways to garner interest in your home. Your home should look like someone lives there, otherwise buyers won’t be able to imagine themselves living there. At the same time, it shouldn’t be too personalized, otherwise it will look like a home for you rather than a home for them. Fortunately, some of the most cost effective methods of home staging are also impersonal.

While it’s certainly more cost effective if done for you rather than a buyer, updating your lighting to more energy-efficient models is sure to relieve some stress from buyers. Purchasing new furniture is expensive, but a similar effect can be achieved at much lower cost with new slipcovers and bedsheets. Even if you plan to keep them yourself, or just use them for staging, a few plants can add vibrancy to your home, particularly if they are in bloom. An important step that costs next to nothing in money, albeit a significant amount of time, is giving your entire home a thorough cleaning.

Due to the Fed increasing benchmark rates, the rates of fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs) are both continuing to increase at a rapid rate. The current average 30-year FRM rate is 6.70%, and it’s 5.96% for ARMs, as of Sept 30th.

It’s normal for FRM rates to be higher than ARM rates, but that may not be the case soon, because of the reasons for the rapidly increasing rates. The ARM rates are directly tied to the benchmark rates — as the benchmark rates increase, the ARM rates will also increase proportionally. While FRM rates are also increasing, it’s not directly because of the increasing benchmark rate. FRM rates are actually tied to bond market rates. However, since the FRM rates are already increasing much faster than bond market rates, they can’t sustainably go much higher, while ARM rates don’t have that restriction and are quickly catching up.

Any time you are selling your home, you want to ensure that the transaction goes smoothly. The best way to do that is to pick the right buyer. Simply selling to the highest bidder may net the most profits, but that assumes the deal actually goes through. Even if it does, you may have lost time and gained headaches. Instead, make sure your buyer is qualified.

There are a few things to look for in a qualified buyer. The first is mortgage pre-approval. If your buyer is not pre-approved, they may have to back out after discovering they don’t qualify for a loan. If there’s a buyer you otherwise like but they aren’t pre-approved, you can certainly suggest getting a pre-approval before submitting an offer. You should also establish terms in the contract regarding an earnest money deposit and check that the buyer has the money ready. There are also a couple of red flags to watch out for. As cliché as it sounds, if an offer looks too good to be true, it probably is. In addition, a buyer who isn’t interested in an inspection may not be very serious.

The housing crisis is a well-established issue and many efforts have been made, or are in the process of being made, to address it. Most of these efforts are focused on low-income housing, since it ensures that the greatest number of people are served by it. However, San Diego faces a different issue. A significant number of residents don’t qualify for affordable housing programs and are instead looking at middle-income housing. Unfortunately for the city, they aren’t able to receive federal subsidies for middle-income housing construction.

So now they’re beginning to devise a plan. The city’s Middle-Income Housing Working Group has recommended a combination of immediate actions, short-term plans, and long-term plans. Immediate steps include streamlining codes and review processes, creating a list of public land available for middle-income housing construction, and converting public facilities to mixed-use structures. Future plans include tax modifications, a public rent registry, construction loan guarantees, investing in community land trusts, and redirecting philanthropic funds to middle-income housing.

The Chris Gardner Foundation is focused on helping disadvantaged youths jumpstart their careers, through their Permission to Dream program. AFL-CIO has now announced a partnership with them specifically directed at building and construction jobs. The program will help high school students, particularly students of color, to first complete their education and then secure a union apprenticeship.

If a student is selected for the program, they will first be given resources to help them in their studies as well as an instructional course in apprenticeships. Once they graduate, if they’ve maintained a certain GPA, they will be introduced to an affiliated union in the field of building and construction. The student will be placed into a paid and registered apprenticeship program. Tools and equipment are covered by a stipend, and transportation assistance is provided.

Home prices fluctuate constantly, but have certainly been on an upward trend the past few years. In fact, it may not be quite as noticeable, but they’ve been trending upwards for about a decade. The difference is that the upward trend has occurred at an anomalous rate since 2019. But now, we’re starting to see hints that this isn’t going to continue. Currently, home prices are still high; however, sales volume has been dropping for the past four months, which will naturally lead to price drops.

On its own, rising home prices isn’t the problem; the issue is that they have been rising far quicker than wages. Even a period of flat home prices at their current high level would provide some slight respite to homebuyers, though of course they would benefit more from declining prices. Sellers aren’t going to be as happy in the next few years, especially if they bought recently. If they bought before 2019, they may still be able to sell at a profit, but not as much of one as if they had already sold by now. Without knowing how much prices are going to drop, there’s a risk of negative equity for homes purchased within the past three years, with the risk increasing the more recently it was purchased. If the downward cycle is particularly long or the decrease particularly steep, this could even extend to homes purchased much earlier.

With four months left in a very chaotic real estate year, we want to take this opportunity to lay some ground work for understanding why the market has headed into a recession. And, to keep things on a positive note, we end with a couple of suggestions on how you might profit from this turn of events.

Some of the nation’s most respected analysts (including Ivy Zelman of Zelman & Associates and Mark Zandi of Moody’s Analytics) are predicting recessionary price drops ranging from 10-20% and lasting through the next two years. (Arguing that we’re only looking at a brief correction, pundits at Goldman Sachs and the Mortgage Bankers Association continue to predict single digit growth.) Meanwhile, here on the street, we’re watching prices drop across the board for the second month in a row.

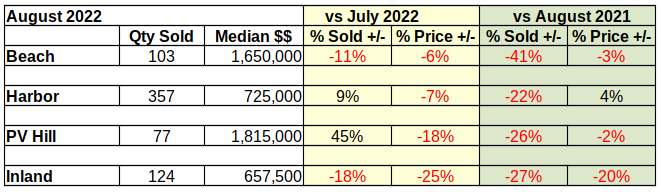

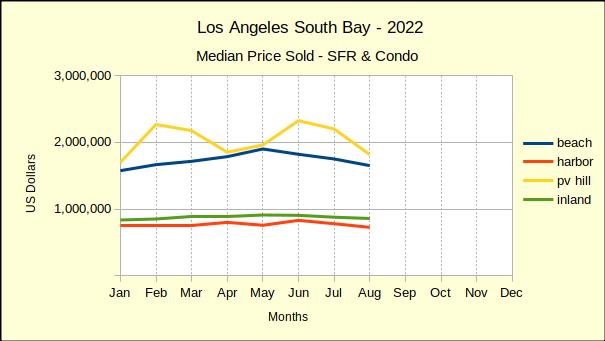

In August we reported that median home prices across the Los Angeles South Bay fell from July, the prior month. Now looking at August sales we find all four areas of the South Bay showed declining median prices again. The month-over-month price drops ranged from 6% at the Beach to 25% in the Inland cities. (See bottom for description of areas.)

Underlining the month-to-month price slippage, three of the four areas also showed declining prices versus the same month last year. Only in the Harbor area are homes still selling for more than they did in 2021. Even there, median price has slid from 9% down to 4% above August of 2021.

2022 Compared to “Normal” Business in 2019

The past two years have seen real estate stumble with the Covid lockdowns in 2020, then skyrocket with the low interest rates in 2021. It’s worth a look back to 2019 to see how the current conditions compare to the most recent “normal” market.

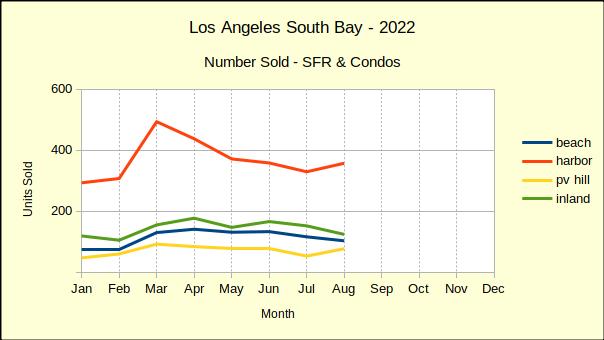

Looking at sales volume in the period January through August of 2019, 1064 homes had sold in the Beach cities. So far this year only 905 homes have sold. That is a 15% drop in sales since the last normal year of business. The trend line for the Beach area has been sliding downward since April.

For the first eight months of 2019 the Harbor area showed sales of 2955 compared to 2945 for this year. That is a drop of .3% – a statistically insignificant change. However, the trend line has been dropping since March. August sales were up slightly from July, which was an unusually slow month for the Harbor area. We expect sales to continue a downward trajectory into 2023.

Palos Verdes home sales for the same period in 2019 totaled 537 versus 568 in 2022. The Hill is the only part of the South Bay where year to date 2022 sales exceed those of 2019. At 6% it’s a healthy increase, too. Despite being the best performing area in South Bay, Palos Verdes sales volume peaked in March and continues to slide. Sales in July were unusually weak, so August shows an upward step in the trend line.

Sales in the Inland area, very much like the Harbor area are down only .4% from 2019 sales for the same period. The difference is statistically insignificant, and the trend line is headed downward.

Declining sales volume creates a larger inventory of homes to sell. As the inventory grows, sellers have more competition and buyers become more demanding and prices start declining. We anticipate continuing growth of available inventory, followed in late fall or early winter by a spate a price drops.

Median Price Up 54% Since 2019

Palos Verdes homes have seen the greatest impact of the Covid-era buying mania. Comparing median prices from the first eight months of 2019 to the first eight of 2022, we find a 54% escalation on the Hill. Normal growth over a three year period would have created 9-10% in price appreciation. Expect much of that excessive price expansion to be erased over the coming months.

Compared to 2019, Beach area median prices have shot up by 32%. This is easily three times normal growth. As we see in the chart below prices started adjusting downward as early as May in the Beach cities.

Since 2019 median prices for the Inland area have climbed 30%. Here in the August 2022 chart below we see Inland area prices have been dropping steadily since May when the median was $910K. During that four month period values have slipped by over $50K.

In the Harbor area home prices have escalated 34%. From 2019 at $565K to 2020 at $607K the Harbor area median grew $40k. Then in 2021, it added another $90K reaching $700K. So far in 2022 the median has reached as high as $830K – another $130K increase, but has now dropped back to $725K, losing $105K off the June median.

Most home buyers are constrained by their income to a particular price range, and salaries have not increased at a rate even remotely similar to real estate prices. Recent studies have shown about 25% of potential buyers were priced out of the purchase market in California by the soaring Covid-era prices.

Interest Rate Shrinks Annual Sales Dollars

In total sales dollars for January through August of 2019, the South Bay weighed in with $5.3 billion. During the same period in 2020 the aggregate amount shrank back to $4.9 billion, followed in 2021 by an upward explosion to $7.9 billion. So far in 2022 the area has reached $6.9 billion.

Each time the Federal Reserve System (fed) increases the short term interest rate the pool of potential buyers shrinks again. As this is written, the Fed is preparing to increase the rate by at least .75% in mid-September and two more increases are anticipated by the end of 2022.

At the current rate of declining value, we estimate the 2022 annual sales value to be approximately $9.5 billion, a decrease of 27% from 2021. Remember that huge budget surplus California had last year? Do not anticipate another this year, and possibly not for a couple of years as the state works its way through this recession.

The Silver Lining in the Cloud

One theory of success in real estate is “Buy low, sell high.” Flippers subscribe to that concept, buying at the bottom, updating and selling at the top of the immediate market. Another theory, not as well supported, but statistically more profitable, is “Buy and Hold.” Buy a piece of property at the best price you can and use it or lease it but – never sell it.

A deep market adjustment doesn’t come very often, so when it does one should take maximum advantage. At the moment it appears there will be a heavy price contraction starting late this year. We’ll know better in late fall and early winter, but all indications today are that a wise property investor should be preparing to buy at the bottom of the market – soon. We constantly search the Southern California coast for outsstanding investment bargains. Tell us what you want to invest – we’ll tell you where to buy.

Methodology

For purposes of comparing homes in the LA South Bay, we have divided the South Bay into four areas. Each is composed of homes of roughly comparable style, geographically similar location and physical characteristics, as well as approximately similar demographic characteristics.

The areas are: Beach: comprises the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: comprises the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor:. comprises the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: comprises the cities of Torrance, Gardena and Lomita.

You may have heard of a home equity loan, but you may not know what it actually is. A home equity loan uses the accrued value of your home as collateral against a loan, and typically allows you to borrow up to 85% of the difference between the home’s value and the balance due on your mortgage. If you fail to pay back your loan, you may have to sell the house to pay it back. This is similar to a home equity line of credit (HELOC), but unlike a HELOC, a home equity loan is a one-time event with a fixed interest rate. The interest rate tends to be higher than the rate for a standard mortgage loan, but lower than rates for most credit cards. Normal regulations for mortgage loan approval apply to home equity loans as well.

A home equity loan is frequently called a second mortgage. Homeowners frequently still have some balance due when they take out a home equity loan, which means they now effectively have not one but two mortgages. In addition, the money is often used to finance the down payment on a second home. However, this isn’t the only purpose of a home equity loan. You don’t need to have a mortgage to get a home equity loan — if you don’t have one, it just means your balance due is zero, and therefore there is potentially a higher ceiling on loan amount. Furthermore, the money gained from a home equity loan doesn’t need to be used for a second home, or anything relating to homes. It’s simply your money, and can be used without restriction.

Traditionally, income inequality has been measured by something called the Gini coefficient. The Gini coefficient is measured on a scale from 0 to 1, with 0 meaning no inequality and 1 meaning a small number of people control the entirety of the wealth. While the Gini coefficient is an excellent indicator of whether or not there is inequality, it does nothing to tell us where it came from except in the case of extreme values. A new measure, the Ortega parameters, seeks to correct that.

It’s commonly thought that the wealth gap is primarily between high-income earners and low-income earners, and that the middle class is effectively nonexistent. That isn’t always the case, and the Ortega parameters can determine where this analysis is accurate and where it is not. There are two separate measures that make up the Ortega parameters: inequality between low-income and middle-to-high-income earners, and inequality between very high income earners and the rest of the population. If a population has low inequality on the first scale and high inequality on the second scale, it simply means that a small number of extremely wealthy individuals live there, but the overall inequality is actually fairly low. The Gini coefficient would not notice this nuance and just rate it as highly unequal. Determining the cause of inequality can also help to devise countermeasures: in areas with high inequality between the lower income earners and middle income earners, the solution is a higher minimum wage; in areas with a few very wealthy individuals, that is better fixed with taxes on high income earners.